PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066462

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066462

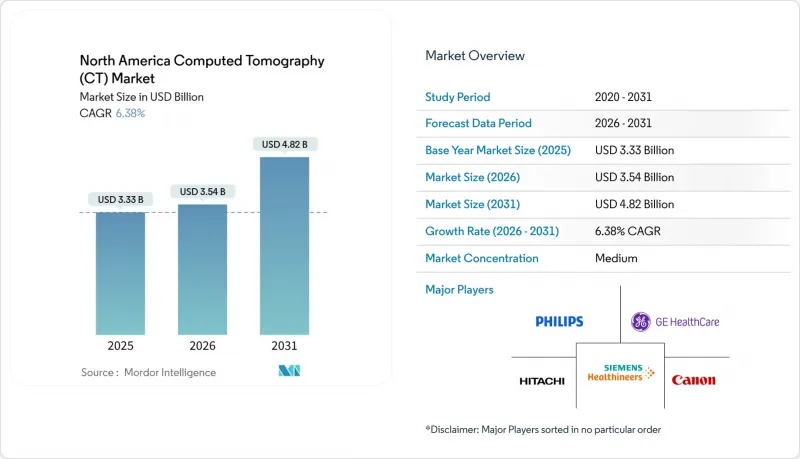

North America Computed Tomography (CT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america computed tomography market size is projected to be USD 3.33 billion in 2025, USD 3.54 billion in 2026, and reach USD 4.82 billion by 2031, growing at a CAGR of 6.38% from 2026 to 2031.

This report is Segmented by Technology (Low-Slice, and More), Product Type (Stationary CT Scanners, and More), Application (Oncology, Cardiology, and More), End-User (Hospitals, Diagnostic Imaging Centers, and More), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Computed Tomography (CT) Market Trends and Insights

Rising Prevalence of Chronic Diseases

With rising cancer rates and increasing cardiac risk factors, the demand for imaging services remains a critical component of healthcare budgets. Projections indicate a 3.2% increase in new cancer cases in the United States, reaching 2.1 million cases by 2026.Additionally, nearly half of United States adults are managing at least one chronic condition, driving the need for regular CT surveillance. Expanded eligibility for lung cancer screenings in 2021 is expected to add 6.4 million new candidates by 2025, although current uptake remains below 20%, presenting significant growth potential. Updated 2024 guidelines have positioned coronary CT angiography as the preferred method for evaluating stable chest pain, shifting referrals away from traditional catheterization. By 2030, adults aged 65 and older will account for 21% of the United States population. This age group, which utilizes CT scans at a rate 3.5 times higher than younger individuals, is expected to drive sustained growth in imaging volumes.

Advances in Low-Dose Multi-Slice CT Technology

Photon-counting detectors and deep-learning reconstruction cut dose while heightening contrast resolution, expanding CT's utility in pediatric and screening workflows. Siemens' NAEOTOM Alpha received Health Canada clearance in 2024, opening the door for competing photon-counting systems. Canon's DLIR platform trimmed reconstruction steps by 40%, evidencing measurable workflow savings. FDA data show that 80% of AI devices cleared in 2024 targeted imaging, underscoring a regulatory environment that rewards dose-efficient innovation.

High Capital & Service Costs

Premium photon-counting CT platforms can cost up to USD 5 million, a hurdle for low-volume centers. Annual service contracts range from 8% to 12% of the the purchase price, compounding budgetary strain. Leasing alleviates upfront outlays but often results in higher total lifecycle spend, reinforcing economic disparities between urban academic hospitals and rural providers.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Geriatric Imaging Volumes

- Favorable Reimbursement & Replacement Cycles

- Radiation-Dose Safety Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-slice systems (>=128-slice) are projected to grow at a rate of 6.94% from 2026 to 2031, surpassing the overall North American computed tomography (CT) market. This growth is driven by cardiology and oncology teams seeking spectral data and sub-millimeter resolution, capabilities that medium-slice scanners cannot provide. In 2025, medium-slice platforms captured 44.16% of the North American CT market share, as community hospitals and outpatient imaging centers prioritized cost and routine abdomen-pelvis throughput. Low-slice models have found their niche in orthopedic extremity and veterinary applications, where their compact size and pricing under USD 500,000 compensate for their limited coverage.

Photon-counting adoption marks a pivotal shift. In 2025, Siemens dispatched 120 NAEOTOM Alpha units throughout North America. Notably, early adopters bypassed 256-slice upgrades, highlighting benefits like 60% savings on iodine contrast and the removal of beam-hardening artifacts. Vendors lacking photon-counting capabilities face potential exclusion from lucrative high-margin cardiac contracts, especially where ALARA dose metrics are paramount.

In 2025, stationary scanners constituted 85.79% of the North American CT market, capitalizing on a throughput of 20-30 patients per day and established reimbursement pathways. Meanwhile, portable and mobile units are on a growth trajectory, with a projected CAGR of 7.09% through 2031. This surge is driven by the formalization of bedside CT protocols in emergency rooms, ICUs, and rural clinics. For instance, Samsung NeuroLogica's CereTom, weighing in at 385 pounds, is favored by neuro-critical-care units for its ability to perform non-contrast head CTs without relocating ventilated patients.

Contract radiology firms operate mobile fleets catering to rural hospitals without on-site CT capabilities. Additionally, FEMA has stockpiled portable systems for disaster response scenarios. The continued reimbursement parity under Medicaid waivers bolsters capital investments in states with widely dispersed populations.

List of Companies Covered in this Report:

- Arineta Cardio Imaging

- Canon

- Carestream Health

- Epica Medical Innovations

- FUJIFILM

- GE Healthcare

- Hitachi

- Imris Inc.

- Koning

- Neusoft Medical Systems

- Koninklijke Philips

- Planmed

- PointNix Co. Ltd.

- Samsung Electronics (Co. NeuroLogica)

- Shenzhen Anke High-Tech

- Shimadzu

- Siemens Healthineers

- Stryker (Imaging Division)

- United Imaging Healthcare

- Xoran Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Diseases

- 4.2.2 Advances in Low-Dose Multi-Slice CT Technology

- 4.2.3 Expanding Geriatric Imaging Volumes

- 4.2.4 Favourable Reimbursement & Replacement Cycles

- 4.2.5 Growth of Outpatient/Mobile CT Centres

- 4.2.6 AI-Enabled Workflow Optimisation

- 4.3 Market Restraints

- 4.3.1 High Capital & Service Costs

- 4.3.2 Radiation-Dose Safety Concerns

- 4.3.3 Detector?Grade Chip Supply Constraints

- 4.3.4 Shortage of Certified CT Technologists

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Technology

- 5.1.1 Low-slice (<16-slice)

- 5.1.2 Medium-slice (32-64-slice)

- 5.1.3 High-slice (>128-slice)

- 5.2 By Product Type

- 5.2.1 Stationary CT Scanners

- 5.2.2 Portable / Mobile CT Scanners

- 5.3 By Application

- 5.3.1 Oncology

- 5.3.2 Neurology

- 5.3.3 Cardiovascular

- 5.3.4 Musculoskeletal

- 5.3.5 Pulmonary / Thoracic

- 5.3.6 Trauma & Emergency

- 5.3.7 Gastrointestinal

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Specialty & Veterinary Clinics

- 5.4.5 Research & Academic Institutes

- 5.5 Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Arineta Cardio Imaging

- 6.3.2 Canon Medical Systems Corporation

- 6.3.3 Carestream Health

- 6.3.4 Epica Medical Innovations

- 6.3.5 Fujifilm Holdings Corporation

- 6.3.6 GE HealthCare

- 6.3.7 Hitachi Healthcare Systems

- 6.3.8 Imris Inc.

- 6.3.9 Koning Corporation

- 6.3.10 Neusoft Medical Systems

- 6.3.11 Philips Healthcare

- 6.3.12 Planmed OY

- 6.3.13 PointNix Co. Ltd.

- 6.3.14 Samsung Electronics (Co. NeuroLogica)

- 6.3.15 Shenzhen Anke High-Tech

- 6.3.16 Shimadzu Corporation

- 6.3.17 Siemens Healthineers

- 6.3.18 Stryker (Imaging Division)

- 6.3.19 United Imaging Healthcare

- 6.3.20 Xoran Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment