PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066469

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066469

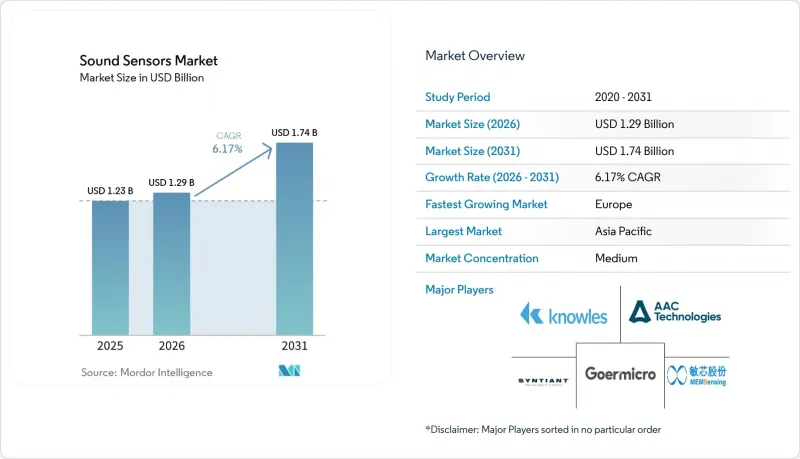

Sound Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the sound sensors market size was valued at USD 1.23 billion in 2025 and estimated to grow from USD 1.29 billion in 2026 to reach USD 1.74 billion by 2031, at a CAGR of 6.17% during the forecast period (2026-2031).

This report is Segmented by Sensor Type (Microelectromechanical (MEMS) System Microphones, and More), Frequency (Infrasound, Audible, and More), Application (Voice Recognition and Speech Processing, and More), End-User Industry (Consumer Electronics, Smartphones and Tablets, True Wireless Stereo Earbuds and Headsets, Smart Speakers and More), and Geography. The Market Sizes and Forecasts are in Terms of Value (USD).

Global Sound Sensors Market Trends and Insights

Expansion Of Voice-First Consumer Devices

The sound sensors market is seeing its strongest near-term pull from always-on voice interfaces across smartphones, TWS earbuds, smart speakers, and AI-enabled wearables. Device upgrades are no longer centered only on wake-word detection, because local inference workloads now require lower self-noise and broader frequency response from the acoustic front end. Syntiant expanded the NDP115 portfolio in December 2025 with eWLB and ultra-thin packages, demonstrating how inference silicon and front-end acoustics are now being tightly co-designed for compact devices. That design trend is narrowing the qualification funnel in the sound sensor market, as OEMs increasingly want fewer vendors and more integrated audio-AI stacks. It also raises the advantage of suppliers with MEMS process control and signal-processing IP over companies that still depend mainly on packaging and assembly scale.

Industrial Predictive Maintenance Adoption

The sound sensors market is gaining durable support from industrial operators that are moving acoustic monitoring from periodic inspection to continuous sensing on rotating and reciprocating equipment. A June 2025 study showed that MEMS acoustic emission sensors achieved fault classification accuracy above 90% on planetary gearboxes at the network edge, supporting faster deployment in harsh settings where cloud dependence is a drawback. As those systems move into enterprise architectures, more of the value is shifting toward combinations of sensors, ASICs, and analytics rather than transducers alone. This is putting pressure on standalone component vendors in the sound sensor market that lack co-integrated processing. Knowles' repositioning after the sale of its consumer MEMS microphone business also points to where suppliers see steadier margins and longer equipment cycles in industrial acoustics.

Accuracy Loss In Noisy Environments

The sound sensors market still faces a clear technical limit in reverberant spaces, high-noise industrial floors, and dense outdoor environments where raw acoustic performance degrades quickly. Research published in May 2025 showed that deep-learning anti-noise triboelectric acoustic sensors can maintain performance at signal-to-noise ratios as low as -10 dB, but the gain depends on added on-sensor neural processing that increases silicon area and system cost. That changes the procurement logic because buyers increasingly evaluate the total cost of the acoustic node rather than just the microphone. In practical deployments, this means that some voice and monitoring use cases in the sound-sensor market still struggle to meet required accuracy thresholds in real operating conditions. The restraint is most visible in the near term because commercial anti-noise architectures remain less mature than the underlying demand pipeline.

Other drivers and restraints analyzed in the detailed report include:

- Growth In Automotive In-Cabin Sensing

- Rise Of Remote And Wearable Acoustic Diagnostics

- Competition From Radar, LiDAR, And Optical Sensing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MEMS microphones accounted for 41.35% of the sound sensor market share in 2025, keeping them firmly ahead of all other sensor categories. Their lead reflects repeated design wins in smartphones, TWS earbuds, and smart speakers, where small package size, low power use, and stable acoustic performance are standard requirements. Electret condenser microphones still hold a place in cost-sensitive intercom and basic industrial voice applications, but they continue to lose ground as OEM specifications rise. Dynamic moving-coil microphones remain established in live audio and broadcast settings, while liquid-coupled and air-coupled ultrasonic devices stay focused on narrower inspection and measurement use cases. Within the sound sensors market, the highest growth is coming from acoustic emission sensors, which are projected to record a 7.77% CAGR through 2031.

That growth is tied to a structural change in how facilities manage equipment health, as operators build continuous IIoT data streams rather than relying on periodic manual checks. The sound sensors industry is therefore giving greater weight to acoustic emission platforms that support networked diagnostics, long operating lifespans, and integration with plant analytics systems. A June 2025 study on planetary gear fault diagnosis reinforced this direction by showing that MEMS acoustic emission sensing can support edge classification with high accuracy in industrial settings. XARION and similar optical approaches are also competing in high-temperature and pressurized environments where conventional contact sensing can be less effective, leaving room for differentiated technologies. At the scale end of the spectrum, AAC Technologies said its MEMS microphone revenue grew by more than 50% in 2025, while FY2025 total revenue reached RMB 31.82 billion (USD 4.43 billion), underscoring the large volume base in the leading tier of the sound sensors market.

The audible band accounted for 69.24% of revenue in 2025, making it the dominant frequency range in the sound sensors market by a wide margin. That position is rooted in the volume concentration of smartphones, earbuds, smart speakers, and wearables that operate within the 20 Hz-20 kHz range. Infrasound remains important in seismic, structural health, and military surveillance applications, but its demand base is much smaller and less volumetric. The ultrasound band is the fastest-growing frequency segment, with the ultrasound sound sensors market projected to expand at a 6.58% CAGR through 2031. Its demand is more diverse than the audible band, spanning medical imaging, sonar, EV battery testing, robotics, and industrial-level measurement.

Growth in ultrasound is being driven by multiple procurement cycles rather than a single end market. NOAA documentation for the Sunrise Wind project showed that passive acoustic monitoring is becoming part of offshore development and compliance programs, supporting longer-term demand for subsea and underwater acoustic systems. Research published in Scientific Data in May 2025 also introduced a distributed acoustic sensing dataset for sounds in the audible spectrum along optical fiber, illustrating how infrastructure sensing is expanding the usable surface area of acoustic technologies. The sound sensors market, therefore, keeps its revenue center in the audible band, while the highest-frequency layer opportunity lies in ultrasound because pricing is less commoditized and applications are broader. Infrasound continues to hold a smaller but stable role, with public-sector and defense procurement providing a demand floor.

Geography Analysis

North America accounted for 29.91% of the sound sensors market share in 2025, making it the largest regional contributor. The United States drives demand through hyperscaler voice platforms, automotive programs, industrial monitoring, and defense acoustics. Canada contributes to marine and subsea acoustics, supported by Ocean Sonics' participation in a USD 4.1 million Canada Ocean Supercluster project in March 2026. Mexico is emerging as a nearshore assembly hub for automotive-linked acoustic supply chains. Regulated procurement pathways, including FCC Part 15 and OSHA noise-related requirements, further support the North American market.

Asia-Pacific is the fastest-growing region, with the sound sensors market projected to grow at a 7.17% CAGR through 2031. China leads in NEV production, MEMS capacity, and enforcement of urban noise management. A Shanghai municipal noise control plan highlights strengthened environmental noise governance. Goertek Microelectronics, in its July 2025 Hong Kong listing prospectus, reported a 43% global market share for acoustic sensors by FY2024, reflecting regional manufacturing concentration. Japan and South Korea influence global standards through precision components and premium hearable products, while India and Southeast Asia expand as deployment and assembly hubs.

Europe remains significant, with Germany, the United Kingdom, and France driving demand across industrial automation, medical diagnostics, and the premium automotive sector. The EU Environmental Noise Directive supports municipal and transport corridor noise monitoring programs, thereby ensuring a stable public procurement base. Offshore wind and passive acoustic surveillance further bolster demand for subsea monitoring, particularly in North Sea activities. South America,, the Middle East,, and Africa remain smaller markets, but mining, oil and gas, smart-city digitization, and environmental compliance are driving selective growth in these regions.

- Knowles Corporation

- AAC Technologies Holdings Inc.

- Goertek Microelectronics Co., Ltd.

- Syntiant Corp.

- Sonion A/S

- Suzhou MEMSensing Microelectronics Technology Co., Ltd.

- Shandong Gettop Acoustic Co., Ltd.

- BSE Co., Ltd.

- ZillTek Technology Corp.

- SensiBel AS

- Bosch Sensortec GmbH

- Wuxi Silicon Source Technology Co., Ltd.

- Microsonic GmbH

- Massa Products Corporation

- XARION Laser Acoustics GmbH

- Ocean Sonics Ltd.

- Sonardyne International Ltd.

- Precision Acoustics Ltd.

- Audiowell Electronics (Guangdong) Co., Ltd.

- Fuzhou Feiying Ultrasonic Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Voice-First Consumer Devices

- 4.2.2 Industrial Predictive Maintenance Adoption

- 4.2.3 Growth in Automotive In-Cabin Sensing

- 4.2.4 Rise of Remote and Wearable Acoustic Diagnostics

- 4.2.5 Smart-City Noise Monitoring Mandates

- 4.2.6 Offshore Wind and Subsea Monitoring Demand

- 4.3 Market Restraints

- 4.3.1 Accuracy Loss in Noisy Environments

- 4.3.2 Competition From Radar, LiDAR, and Optical Sensing

- 4.3.3 Microelectromechanical System Application-Specific Integrated Circuit Intellectual-Property Fragmentation

- 4.3.4 Specialty Piezo Material Supply Volatility

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sensor Type

- 5.1.1 Microelectromechanical (MEMS) System Microphones

- 5.1.2 Electret Condenser Microphones

- 5.1.3 Dynamic-Moving-Coil Microphones

- 5.1.4 Ultrasonic Sensors

- 5.1.5 Air-Coupled Ultrasonic Sensors

- 5.1.6 Acoustic Emission Sensors

- 5.1.7 Liquid-Coupled Ultrasonic Sensors

- 5.1.8 Other Sensor Types

- 5.2 By Frequency

- 5.2.1 Infrasound

- 5.2.2 Audible

- 5.2.3 Ultrasound

- 5.3 By Application

- 5.3.1 Voice Recognition and Speech Processing

- 5.3.2 Noise Cancellation and Audio Enhancement

- 5.3.3 Environmental and Noise Monitoring

- 5.3.4 Security and Surveillance

- 5.3.5 Medical Diagnostics and Healthcare

- 5.3.6 Underwater Sensing and Sonar

- 5.3.7 Telecommunications Infrastructure

- 5.3.8 Other Applications

- 5.4 By End-User Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Smartphones and Tablets

- 5.4.3 True Wireless Stereo Earbuds and Headsets

- 5.4.4 Smart Speakers and Home Hubs

- 5.4.5 Wearables and Hearables

- 5.4.6 Industrial

- 5.4.7 Automotive and Transportation

- 5.4.8 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Knowles Corporation

- 6.4.2 AAC Technologies Holdings Inc.

- 6.4.3 Goertek Microelectronics Co., Ltd.

- 6.4.4 Syntiant Corp.

- 6.4.5 Sonion A/S

- 6.4.6 Suzhou MEMSensing Microelectronics Technology Co., Ltd.

- 6.4.7 Shandong Gettop Acoustic Co., Ltd.

- 6.4.8 BSE Co., Ltd.

- 6.4.9 ZillTek Technology Corp.

- 6.4.10 SensiBel AS

- 6.4.11 Bosch Sensortec GmbH

- 6.4.12 Wuxi Silicon Source Technology Co., Ltd.

- 6.4.13 Microsonic GmbH

- 6.4.14 Massa Products Corporation

- 6.4.15 XARION Laser Acoustics GmbH

- 6.4.16 Ocean Sonics Ltd.

- 6.4.17 Sonardyne International Ltd.

- 6.4.18 Precision Acoustics Ltd.

- 6.4.19 Audiowell Electronics (Guangdong) Co., Ltd.

- 6.4.20 Fuzhou Feiying Ultrasonic Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment