PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066485

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066485

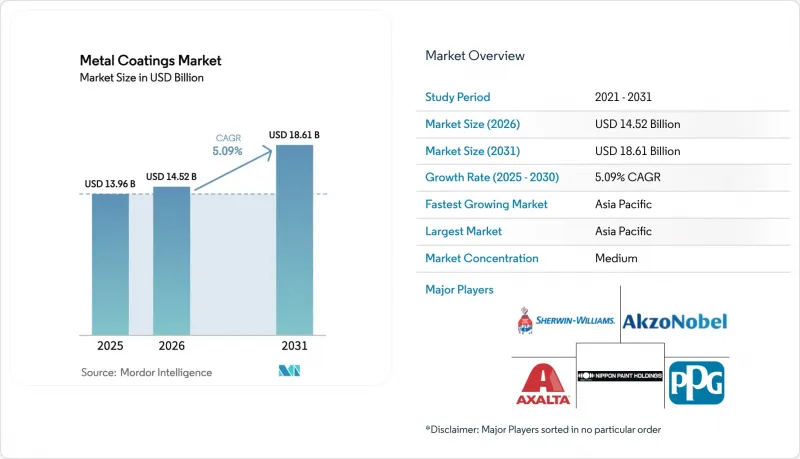

Metal Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the metal coatings market size is expected to increase from USD 13.96 billion in 2025 to USD 14.52 billion in 2026 and reach USD 18.61 billion by 2031, growing at a CAGR of 5.09% over 2026-2031.

This report is Segmented by Resin Type (Epoxy, Polyester, Polyurethane, Other Resin Types), Technology (Water-Borne, Solvent-Borne, Powder, and More), Application (Architectural, Automotive, Marine, Protective, General Industrial, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Metal Coatings Market Trends and Insights

Stringent VOC Caps Accelerating Water-Borne Chemistries

Regulators across three continents have set stringent ceilings on volatile organic compounds (VOCs), effectively resetting formulation baselines. In 2024, the United States capped VOCs in architectural coatings. Meanwhile, the European Union is pushing for a reduction by 2030. Germany, ahead of the curve, has already set a limit for metal substrates. In 2025, China mandated VOC audits for appliance and metal-furniture lines in Guangdong and Jiangsu. Singapore, not to be left behind, established a threshold in January 2025. Water-borne options have surged, now accounting for a significant portion of North America's architectural metal output, a notable rise from earlier years. However, achieving C5 corrosion protection remains a challenge without hybrid polyurethane-acrylic chemistries. Suppliers are now combining flash-rust inhibitors with innovative latent catalysts, effectively reducing cure windows under ambient conditions. Formulators offering ISO 12944-compliant water-borne systems for marine or oil-and-gas sectors stand to reap premium margins in the metal coatings arena.

Re-Roofing and Bridge-Rehab Up-Cycle in OECD Markets

Aging transport assets are fueling a consistent demand for coatings. In the United States, many bridges have surpassed their 50-year service life, leading to a significant need for protective coatings by 2030. Europe, recognizing the urgency, has allocated funds for bridge and tunnel refurbishments under its TEN-T program. Meanwhile, Japan's Longevity Plan is addressing thousands of bridges, employing zinc-rich epoxy primers to extend repainting intervals. As commercial roof lifecycles shorten, driven by the pursuit of cool-roof credits under LEED v5, there is a heightened demand for fluoropolymer and silicone-modified polyester top-coats. However, shortages in zinc dust and titanium dioxide are causing project delays, simultaneously creating a market for low-zinc epoxy alternatives that provide galvanic protection and mitigate supply risks.

Epoxy Resin Supply Volatility Linked to BPA Regulations

In January 2025, the EU's ban on food-contact epoxy coatings forced the market to pivot toward bisphenol F and pricier bio-based substitutes. France's ANSES expedited phase-outs, while the U.S. FDA encouraged beverage canners to move away from traditional epoxies via voluntary guidance. In 2025, spot resin prices spiked, squeezing converter margins and postponing project tenders, as specifiers sought to requalify alternatives. BPA-free systems, with their lower crosslink density, require thicker films, leading to increased consumption per square meter. This pressure is felt across the metal coatings market, disproportionately impacting small and midsize can-coating firms in Europe.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Light-Weighting Pushing Aluminum Coil Coatings

- EV Safety and Hydrogen Pipelines Lifting Specialty Protective Solutions

- Compliance Cost of Solvent-Borne Lines in ASEAN and LATAM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, epoxy resins captured 39.54% of the market revenue, largely due to their superior adhesion and chemical resistance, particularly in ISO 12944 C4 and C5 services. Meanwhile, other resin types - including acrylics, fluoropolymers, and silicone hybrids - are set to outpace the broader metal coatings market, with a projected CAGR of 6.89% during the forecast period of 2026-2031. While epoxies traditionally dominated heavy-duty protection, allowing for thicker films with fewer coats, buyers have increasingly gravitated toward polyester and polyurethane blends. This shift, influenced by BPA restrictions and rising costs, was especially evident in applications prioritizing weatherability over immersion service.

Bio-based cardanol epoxies and bisphenol F variants provided some relief, but users faced a trade-off: a decrease in crosslink density necessitated a thicker build to match the performance of conventional barriers. Conversely, while fluoropolymers came at a premium, they were favored for coastal and high-rise facade projects, where long-term gloss retention was paramount. Additionally, silicone-modified polyesters gained traction in coil lines, particularly in scenarios where temperatures had to be controlled to avoid aluminum temper loss. These developments further broadened the metal coatings market for specialty resins. Suppliers adeptly navigating environmental regulations while ensuring efficient film builds are set to shape resin-mix dynamics through 2031.

Geography Analysis

Asia-Pacific, accounting for 46.95% of global sales in 2025, is projected to grow at a CAGR of 6.41% through the forecast period of 2026-2031. This growth is bolstered by China's strong manufacturing base, India's ambitious infrastructure projects, and ASEAN's strict VOC regulations. China's push for a significant share in the EV market by 2030 is driving the uptake of coil-coated aluminum. Simultaneously, audits in Guangdong and Jiangsu are accelerating the shift to water-borne solutions. In India, budgets for steel structures are increasingly being allocated to protective paints, ensuring consistent tenders that benefit both domestic and international suppliers. Vietnam's newly imposed cap is prompting line retrofits, guiding regional production towards compliant coatings.

North America, which holds a substantial share of 2025's turnover, is reaping benefits from the Bipartisan Infrastructure Law, especially given that many of its bridges are over 50 years old. Europe not only contributes significantly to the revenue but also leads in regulatory innovations, from banning BPA to defining hydrogen-pipeline standards under its Hydrogen Backbone vision. These established regions emphasize high-value protective specifications, reinforcing the demand for solvent-borne epoxies, even as powder and water-based platforms gain momentum.

While South America and the Middle-East currently hold a smaller combined market share, they are poised for rapid percentage growth. Brazil's strict ozone regulations and Saudi Arabia's NEOM contracts are broadening protective niches. Yet, challenges arise with Argentina's fragmented provincial VOC regulations and inconsistent enforcement in certain ASEAN countries, complicating supply-chain planning. Nonetheless, these challenges also unveil acquisition and greenfield opportunities for global formulators seeking a stronger presence in the metal coatings market.

- AkzoNobel N.V.

- Axalta Coating Systems LLC

- BASF

- Beckers Group

- Chugoku Marine Paints, Ltd.

- Hempel A/S

- Jotun

- Kansai Paint Co.,Ltd.

- Nippon Paint Holdings Co. Ltd

- PPG Industries Inc.

- Shalimar Paints Ltd

- Socomore

- Teknos Group

- The Sherwin-Williams Company

- TIGER Coatings GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent VOC caps accelerating water-borne chemistries

- 4.2.2 Re-roofing and bridge-rehab up-cycle in OECD markets

- 4.2.3 Automotive light-weighting pushing aluminium coil coatings

- 4.2.4 EV battery-pack safety driving intumescent metal coatings

- 4.2.5 Hydrogen pipelines demanding high-temperature anti-corrosion linings

- 4.3 Market Restraints

- 4.3.1 Epoxy resin supply volatility linked to BPA regulations

- 4.3.2 Compliance cost of solvent-borne lines in ASEAN and LATAM

- 4.3.3 Under-cured powder defects in large offshore components

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyester

- 5.1.3 Polyurethane

- 5.1.4 Other Resin Types (Acrylic, Fluoropolymer, etc.)

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Powder

- 5.2.4 Ultraviolet (UV)-Cured

- 5.2.5 Light Emitting Diode (LED) Curing

- 5.3 By Application

- 5.3.1 Architectural

- 5.3.2 Automotive

- 5.3.3 Marine

- 5.3.4 Protective

- 5.3.5 General Industrial

- 5.3.6 Other Applications (Renewable Energy, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 Thailand

- 5.4.1.6 Malaysia

- 5.4.1.7 Philippines

- 5.4.1.8 Vietnam

- 5.4.1.9 Singapore

- 5.4.1.10 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Turkey

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Egypt

- 5.4.5.5 Qatar

- 5.4.5.6 Nigeria

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AkzoNobel N.V.

- 6.4.2 Axalta Coating Systems LLC

- 6.4.3 BASF

- 6.4.4 Beckers Group

- 6.4.5 Chugoku Marine Paints, Ltd.

- 6.4.6 Hempel A/S

- 6.4.7 Jotun

- 6.4.8 Kansai Paint Co.,Ltd.

- 6.4.9 Nippon Paint Holdings Co. Ltd

- 6.4.10 PPG Industries Inc.

- 6.4.11 Shalimar Paints Ltd

- 6.4.12 Socomore

- 6.4.13 Teknos Group

- 6.4.14 The Sherwin-Williams Company

- 6.4.15 TIGER Coatings GmbH & Co. KG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Biodegradable Metal Coatings