PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066490

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066490

Massive Open Online Course (MOOC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

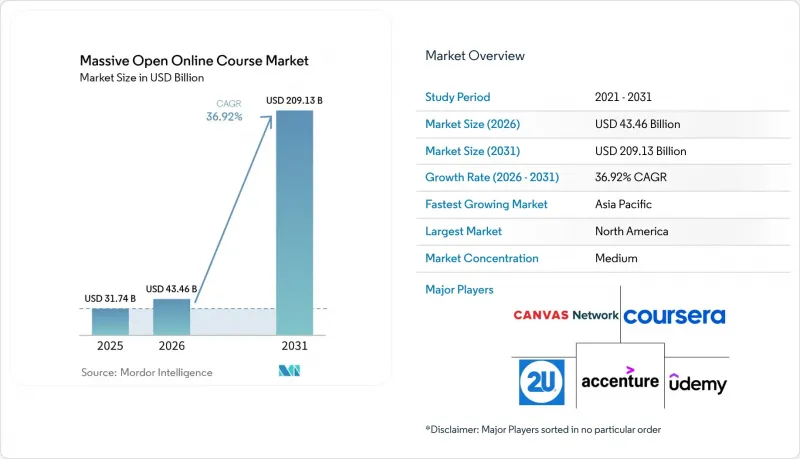

According to Mordor Intelligence, the massive open online course (MOOC) market size was valued at USD 31.74 billion in 2025 and estimated to grow from USD 43.46 billion in 2026 to reach USD 209.13 billion by 2031, at a CAGR of 36.92% during the forecast period (2026-2031).

This report is Segmented by Platform Type (cMOOC, XMOOC, Hybrid/SPOC), Subject Area (Technology and Computer Science, Business and Management, and More), End User (Higher-Education Students, K-12 Learners, and More), Revenue Model (Free Audit-Only, Freemium, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Massive Open Online Course (MOOC) Market Trends and Insights

Corporate upskilling mandates drive enterprise adoption

Enterprise learning budgets surpassed USD 350 billion in 2025 as employers tied competitive advantage to continuous skill renewal. FPT Corporation's alliance with Udemy illustrates this momentum: the firm invested VND 187.3 billion (USD 7.6 million) to train staff across Japan and Korea, embedding curated MOOCs into its performance framework Similar talent-centric investments from Skillsoft and Accenture's LearnVantage accelerate platform demand by connecting verified certificates to internal career ladders.

Government funding accelerates digital education infrastructure

Canada earmarked CAD 39.2 million (USD 29.1 million) for the CanCode program's AI track, Australia allocated AUD 436.4 million (USD 291.6 million) to Skills for Education and Employment, and the EU's Digital Europe Programme injected EUR 108 million (USD 117.7 million) into advanced digital skills. These grants subsidize content development, subsidize micro-credential recognition, and upgrade broadband capacity, positioning MOOCs as critical national competitiveness infrastructure

Completion rates remain critically low despite innovation

Average course completion hovers between 5% and 15% on major platforms, and even MIT-Harvard joint MOOCs close at a 3.13% rate. India's SWAYAM registers sub-4% completions despite government credit recognition, underscoring a persistent motivation gap. Research links early dropout to limited digital literacy, while later attrition correlates with time-management and academic skill mismatches. Platforms experiment with cohort mentors, micro-learning formats, and gamified milestones to mitigate attrition, yet material improvement remains elusive.

Other drivers and restraints analyzed in the detailed report include:

- AI-driven personalization transforms learning outcomes

- Blockchain credentials gain enterprise recognition

- Data-privacy regulations constrain personalization capabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid/SPOC solutions captured 40.11% CAGR potential through 2031 as employers seek structured cohorts that blend asynchronous video with live coaching. xMOOCs still hold 48.76% of 2025 revenue, buoyed by university partnerships and well-defined curricula that address compliance and accreditation requirements. cMOOC offerings continue to serve collaborative knowledge communities but command limited scale.

Enterprises integrate Hybrid/SPOC platforms directly into learning-management systems to embed bite-sized virtual sessions into the workday. Real Madrid University School's Coursera tie-up delivers 12 sports-industry courses that combine peer projects and faculty webinars to global cohorts. These structured experiences improve social presence and accountability, elevating feedback cycles and completion metrics compared with self-paced xMOOCs.

Technology and Computer Science retained 32.52% of the Massive Open Online Course market share in 2025 by catering to relentless demand for programming, AI, and cybersecurity competencies. Massive Open Online Course market size in language learning is rising fastest, expanding at a 37.68% CAGR as remote work multiplies multilingual communication needs. Business and Management and Science and Engineering segments post steady gains but face competitive saturation.

Duolingo's USD 748 million 2024 revenue validates consumer enthusiasm for gamified language apps that transition seamlessly into enterprise offerings. Simultaneously, 101 Blockchains collaborates with Accredible to issue digital certificates for over 30,000 professionals, demonstrating convergence between advanced tech content and credential innovation.

Geography Analysis

North America retained 31.65% of the Massive Open Online Course (MOOC) market share in 2025, anchored by robust venture-capital flows, deep corporate learning budgets, and early regulatory clarity on micro-credentials. The United States accounts for the lion's share, with Accenture's USD 1 billion Udacity acquisition underscoring confidence in platform economics. Canada's CanCode funding embeds AI curricula into K-12 pipelines, while Mexico's near-shoring boom fuels bilingual upskilling demand.

Asia-Pacific is the fastest-growing territory, expanding at a 37.25% CAGR. India's SWAYAM and China's domestic MOOC ecosystems tap colossal learner bases and government sponsorship that recognize MOOCs as scalable answers to higher-education capacity constraints. Australia's AUD 436.4 million Skills for Education and Employment initiative reinforces regional public-private collaboration, and FPT-Udemy training illustrates cross-border enterprise learning synergies spanning Japan, Korea, and Vietnam.

Europe, the Middle East, and Africa show steady uptake moderated by regulatory and infrastructure diversity. The EU's Digital Europe grants foster coordinated credential standards and fund advanced digital-skills content, while the University of Surrey's AR/VR course portfolio illustrates an academic push toward immersive learning. In the Middle East, IHG Academy's Arabic-language hospitality MOOC addresses local workforce needs. Sub-Saharan Africa leverages mobile-first delivery to mitigate campus capacity gaps, while South America advances through Brazil and Argentina's ed-tech investment climates.

- Coursera Inc.

- Udemy, Inc.

- edX LLC (2U, Inc.)

- LinkedIn Learning (Microsoft Corp.)

- FutureLearn Ltd. (Global University Systems)

- Khan Academy, Inc.

- Pluralsight LLC

- Instructure Holdings, Inc. (Canvas)

- Blackboard Inc. (Anthology)

- 360training.com, Inc.

- openSAP (SAP SE)

- Skillshare, Inc.

- Alison Ltd.

- Swayam (NPTEL, Govt. of India)

- Iversity GmbH (Springer Nature)

- Miriadax (Telefonica Learning Services)

- OpenWHO (World Health Organization)

- Udacity Inc. (Accenture plc)

- WizIQ Inc.

- OpenLearn (Open University)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for cost-effective, flexible learning

- 4.2.2 Corporate upskilling and reskilling mandates

- 4.2.3 Smartphone and broadband proliferation

- 4.2.4 Government push for micro-credentials and funding

- 4.2.5 AI-driven adaptive learning breakthroughs (under-radar)

- 4.2.6 Global employer consortiums validating MOOC badges (under-radar)

- 4.3 Markeat Restraints

- 4.3.1 Persistently low completion and engagement rates

- 4.3.2 Quality-assurance / accreditation gaps

- 4.3.3 Stricter data-privacy rules limiting learner analytics (under-radar)

- 4.3.4 Post-pandemic digital-fatigue dampening screen time (under-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform Type

- 5.1.1 cMOOC

- 5.1.2 xMOOC

- 5.1.3 Hybrid / SPOC

- 5.2 By Subject Area

- 5.2.1 Technology and Computer Science

- 5.2.2 Business and Management

- 5.2.3 Science and Engineering

- 5.2.4 Arts and Humanities

- 5.2.5 Language Learning

- 5.3 By End User

- 5.3.1 Higher-Education Students

- 5.3.2 K-12 Learners

- 5.3.3 Working Professionals / Corporate

- 5.3.4 Lifelong Learners

- 5.4 By Revenue Model

- 5.4.1 Free (Audit-only)

- 5.4.2 Freemium

- 5.4.3 Subscription (B2C)

- 5.4.4 Pay-per-course / Certificate

- 5.4.5 Enterprise Licensing (B2B)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Coursera Inc.

- 6.4.2 Udemy, Inc.

- 6.4.3 edX LLC (2U, Inc.)

- 6.4.4 LinkedIn Learning (Microsoft Corp.)

- 6.4.5 FutureLearn Ltd. (Global University Systems)

- 6.4.6 Khan Academy, Inc.

- 6.4.7 Pluralsight LLC

- 6.4.8 Instructure Holdings, Inc. (Canvas)

- 6.4.9 Blackboard Inc. (Anthology)

- 6.4.10 360training.com, Inc.

- 6.4.11 openSAP (SAP SE)

- 6.4.12 Skillshare, Inc.

- 6.4.13 Alison Ltd.

- 6.4.14 Swayam (NPTEL, Govt. of India)

- 6.4.15 Iversity GmbH (Springer Nature)

- 6.4.16 Miriadax (Telefonica Learning Services)

- 6.4.17 OpenWHO (World Health Organization)

- 6.4.18 Udacity Inc. (Accenture plc)

- 6.4.19 WizIQ Inc.

- 6.4.20 OpenLearn (Open University)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment