PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066491

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066491

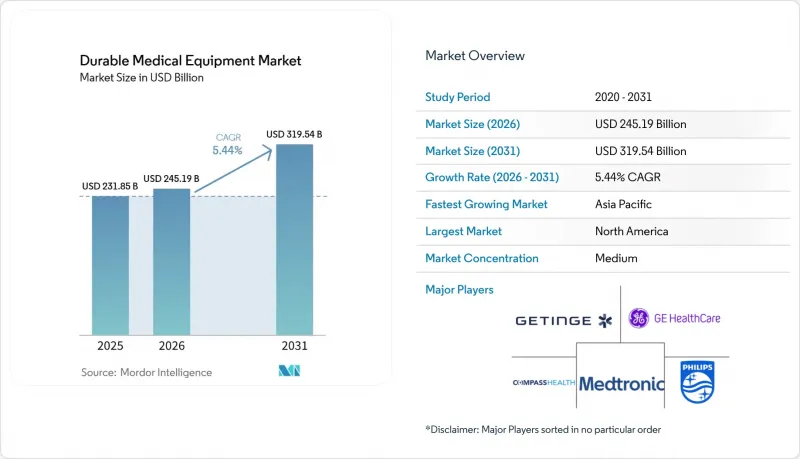

Durable Medical Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the durable medical equipment market size was valued at USD 231.85 billion in 2025 and is estimated to grow from USD 245.19 billion in 2026 to reach USD 319.54 billion by 2031, at a CAGR of 5.44% during the forecast period (2026-2031).

This report is Segmented by Device Type (Personal Mobility Devices [Wheelchairs, and More], Bathroom Safety Devices & Medical Furniture, and Monitoring & Therapeutic Devices), End-User (Hospitals & Clinics, and More), Distribution Channel (Hospital & Clinic Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Durable Medical Equipment Market Trends and Insights

Rapidly Ageing Population Sustaining Mobility and Respiratory Demand

Japan's share of citizens aged 75 years and older surpassed 15% in 2025, pushing purchases of wheelchairs, walkers, and oxygen concentrators covered by the long-term care insurance program that reimburses up to 90% of device costs . Eurostat forecasts Europe's population aged 65 and above to reach 30% by 2050, prompting national payers to subsidize home-based respiratory therapy and mobility aides. CMS projects Medicare enrollment to rise to 80 million by 2030, enlarging the addressable base for powered wheelchairs and CPAP systems. Germany allocated EUR 450 billion in 2024 health spending, with a rising share earmarked for assistive technology under social insurance rules. Safety standards such as ISO 7176 and IEC 60601 help ensure devices supplied to seniors meet durability and electrical requirements, reducing liability for providers.

IoT-Enabled Device Ecosystems Improving Adherence and Data Monetization

Connected glucose monitors, pulse oximeters, and portable ventilators increasingly pair with smartphones, transmitting real-time readings to cloud dashboards. Abbott's FreeStyle Libre 2 Plus transmits glucose data directly to Apple Health, allowing physicians to adjust dosing without clinic visits. ResMed's AirSense 11 CPAP streams usage metrics to clinicians, cutting 30-day readmissions for obstructive sleep apnea by 18% in a 2024 multi-site study. The FDA's TEMPO model grants automatic Medicare coverage for breakthrough connected devices within two days of approval, slashing time-to-reimbursement and encouraging rapid commercial launches. However, heterogeneous data standards slow cross-platform analytics, motivating adoption of HL7 FHIR for interoperability across vendor ecosystems.

High Upfront and Lifecycle Service Costs

Advanced power wheelchairs with IoT sensors list between USD 15,000 and USD 40,000, while smart hospital beds range from USD 8,000 to USD 25,000, challenging budgets where third-party reimbursement is thin. Preventive maintenance and software updates frequently add 20% to ownership expenses over five years, extending replacement cycles and increasing downtime risk. Biomedical technician shortages keep hourly service rates high across mature markets, with the U.S. Bureau of Labor Statistics expecting only 5% employment growth through 2032. Subscription bundles from equipment-as-a-service vendors absorb the upfront hit by spreading costs over monthly invoices. In Europe, MDR post-market surveillance updates every two years add EUR 50,000-200,000 per product line, expenses generally passed to buyers.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Home-Based Chronic Care Supported by Reimbursement Expansion

- AI-Driven Predictive Maintenance Lowering TCO for Providers

- Uptake of GLP-1 Obesity Drugs Reducing Mobility-Aid Volumes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monitoring and therapeutic devices held a 38.55% share of the durable medical equipment market in 2025 and are on track to expand at an 8.25% CAGR to 2031, outperforming mobility aids and bathroom-safety products. OTC glucose monitors like Abbott FreeStyle Libre 2 Plus and Dexcom Stelo remove finger-stick calibration and sync to mobile health apps, spurring double-digit unit growth across North America . Philips Respironics' multi-year recall shifted sleep-apnea demand to ResMed, whose cellular-enabled AirSense 11 helped reduce hospital readmissions by 18% in pilot programs, strengthening its foothold.

Growth momentum continues as payers reimburse remote vital-sign monitors used in home-health programs, helping the durable medical equipment market size for monitoring devices widen. Yet insulin-pump volumes face pressure from obesity-drug uptake, pushing pump makers to concentrate on pediatric and Type 1 diabetes niches. Oxygen concentrators and CPAP systems benefit from mHealth connectivity that supports remote adherence tracking. In contrast, personal mobility devices confront slower growth; to offset volume headwinds, power-chair vendors now embed fall-detection sensors and posture-adjustment algorithms that collect usable clinical data, reinforcing their role in value-based care pathways.

Geography Analysis

North America remains the largest regional contributor at 41.13% share in 2025, buoyed by rising Medicare enrollment and CMS policy that lifts home-health reimbursement. The FDA's expedited coverage for breakthrough devices shrinks commercialization timelines, accelerating adoption of IoT monitors and AI-enhanced oxygen concentrators. Amazon Pharmacy's logistics backbone supports rapid equipment delivery, helping online sales climb, while Canada's Assistive Devices Program funds up to 75% of eligible product costs, expanding access. Mexico's social insurance pilots portable oxygen services in rural areas, cutting hospital admissions.

Asia-Pacific is the fastest-growing arena at an 8.51% CAGR to 2031, propelled by Japan's "2025 problem" demographic shift and China's preference for aging in place. India's Ayushman Bharat Digital Mission created unique health IDs for half a billion citizens, smoothing telemedicine prescriptions for home-use monitors. South Korea reimburses up to 80% of portable oxygen rentals, while Australia's National Disability Insurance Scheme funds assistive technology for more than 600,000 participants.

Europe carries substantial weight behind aging demographics and ESG procurement goals. Germany channels social insurance toward assistive devices, the NHS commits to net-zero procurement, and France's Silver Economy initiative subsidizes home-medical kits, pushing lifecycle-low-carbon equipment into mainstream demand. EU-wide medical device regulation mandates post-market surveillance that raises compliance barriers but uplifts safety, reinforcing buyer confidence in long-lasting equipment that anchors the durable medical equipment market.

- Abbott Laboratories

- Arjo AB

- Baxter International Inc. (Hillrom & Welch Allyn)

- Beckton Dickinson

- Cardinal Health

- Coloplast

- Compass Health

- ConvaTec Group plc

- Drive DeVilbiss Healthcare

- GE HealthCare Technologies Inc.

- Getinge

- Invacare

- Koninklijke Philips

- Masimo

- Medtronic

- Nihon Kohden

- OMRON

- Permobil (Patricia Industries)

- Pride Mobility Products

- Resmed

- Mindray

- Siemens Healthineers

- Stryker

- Sunrise Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapidly ageing population sustaining mobility & respiratory demand

- 4.2.2 IoT-enabled device ecosystems improving adherence & data monetisation

- 4.2.3 Shift to home-based chronic-care supported by reimbursement expansion

- 4.2.4 AI-driven predictive maintenance lowering TCO for providers

- 4.2.5 E-commerce & DTP fulfilment compressing channel costs

- 4.2.6 ESG-linked hospital cap-ex boosting energy-efficient equipment refresh

- 4.3 Market Restraints

- 4.3.1 High upfront & lifecycle service costs

- 4.3.2 Uptake of GLP-1 obesity drugs reducing mobility-aid volumes

- 4.3.3 Skilled biomedical-tech labour shortages lengthening service cycles

- 4.3.4 Fragmented post-sale data standards hampering interoperability

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Personal Mobility Devices

- 5.1.1.1 Wheelchairs

- 5.1.1.2 Crutches & Canes

- 5.1.1.3 Walkers & Rollators

- 5.1.1.4 Other Personal Mobility Devices

- 5.1.2 Bathroom Safety Devices & Medical Furniture

- 5.1.2.1 Medical Beds & Mattresses

- 5.1.2.2 Commodes & Toilets

- 5.1.2.3 Other Bathroom Safety & Medical Furniture

- 5.1.3 Monitoring & Therapeutic Devices

- 5.1.3.1 Blood Glucose Monitors

- 5.1.3.2 Oxygen Equipment

- 5.1.3.3 Vital-sign Monitors

- 5.1.3.4 Other Monitoring & Therapeutic Devices

- 5.1.1 Personal Mobility Devices

- 5.2 By End-User

- 5.2.1 Hospitals & Clinics

- 5.2.2 Home-Healthcare Settings

- 5.2.3 Ambulatory Surgical Centres

- 5.2.4 Other End-Users

- 5.3 By Distribution Channel

- 5.3.1 Hospital & Clinic Pharmacies / DME Suppliers

- 5.3.2 Retail Pharmacies & DME Stores

- 5.3.3 Online & Direct-to-Patient Channels

- 5.3.4 Business-to-business (B2B)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Arjo AB

- 6.3.3 Baxter International Inc. (Hillrom & Welch Allyn)

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Cardinal Health, Inc.

- 6.3.6 Coloplast A/S

- 6.3.7 Compass Health Brands

- 6.3.8 ConvaTec Group plc

- 6.3.9 Drive DeVilbiss Healthcare

- 6.3.10 GE HealthCare Technologies Inc.

- 6.3.11 Getinge AB

- 6.3.12 Invacare Corporation

- 6.3.13 Koninklijke Philips N.V.

- 6.3.14 Masimo Corporation

- 6.3.15 Medtronic plc

- 6.3.16 Nihon Kohden Corporation

- 6.3.17 OMRON Corporation

- 6.3.18 Permobil (Patricia Industries)

- 6.3.19 Pride Mobility Products Corp.

- 6.3.20 ResMed Inc.

- 6.3.21 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.22 Siemens Healthineers AG

- 6.3.23 Stryker Corporation

- 6.3.24 Sunrise Medical LLC

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment