PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066493

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066493

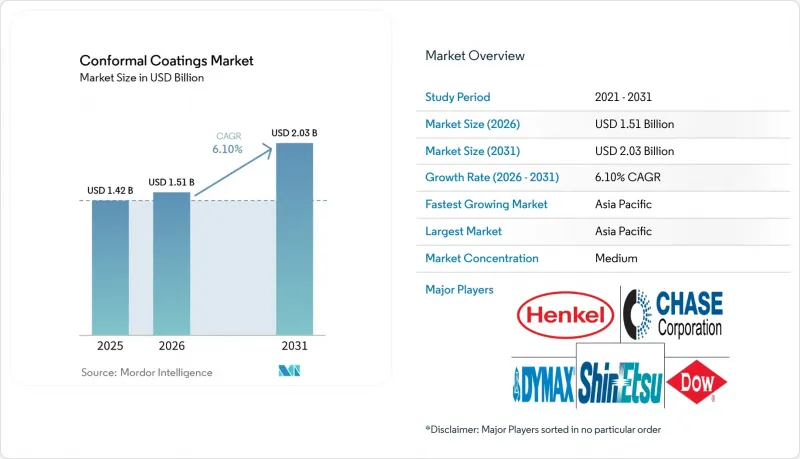

Conformal Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the conformal coatings market size is expected to grow from USD 1.42 billion in 2025 to USD 1.51 billion in 2026 and is forecast to reach USD 2.03 billion by 2031 at 6.10% CAGR over 2026-2031.

This report is Segmented by Material Type (Acrylic, Epoxy, Silicone and More), Technology (Solvent-Based, Water-Based, UV-Cured, and Hybrid/Other Advanced Systems), Operation Method (Spray Coating, Dip Coating, and More), End-User Industry (Consumer Electronics, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Conformal Coatings Market Trends and Insights

5G Smartphones and IoT Wearables Require Mini-Circuit Protection

Sub-10 mm2 RF front-ends and stacked passives leave little clearance, compelling coatings with dielectric constants below 3 and +-5 µm thickness control to prevent impedance drift. Wearables demand biocompatible films that survive 100,000 flex cycles yet retain IPC-CC-830C Class 3 reliability. Contract assemblers in Vietnam and India saved 40% of material by switching to selective robotic dispensing, eliminating manual masking on camera modules and flexible OLED driver boards. DuPont's Interconnect Solutions reported low-double-digit organic growth in Q3 2024 on the back of these ramps. Manufacturers also pair UV-cured topcoats with transparent acrylic under-layers to speed cure and preserve AOI visibility.

LEO Satellites and Avionics Electronics Need High-Performance Coatings

More than 10 000 LEO satellites slated for launch between 2024 and 2030 each carry 50-200 boards that must withstand atomic oxygen, -150 °C to +125 °C cycling, and 100 krad radiation environments. Parylene and fluoropolymer nano-coatings deliver dielectric strength above 5 kV/mm and outgassing below 1% total mass loss, surpassing Type AR acrylics. Henkel logged double-digit electronics growth in China during 2024, partially tied to avionics programs. Aerospace OEMs now qualify silicone systems for fly-by-wire control at 15 000 m where low pressure invites corona discharge. Automated vacuum deposition lines with +-0.1 mm accuracy improve first-pass yield to 98% on phased-array modules.

Rework/Inspection Complexity of UV-Cured Opaque Films

Opaque UV coatings cure within seconds, yet block AOI cameras from verifying solder joints required under IPC-A-610 Class 3. Mechanical abrasion or plasma is often the only route to remove misapplied films, risking pad lift on fine-pitch QFNs. Hybrid lines now apply transparent UV material on AOI-critical zones and pigmented coating elsewhere, adding 15% overhead in fixtures and recipes. Nordson's Select Coat SL-1040 logs nozzle flow and UV dose to cut rework under 1%. EMS players still cite 2-4 hour training curves for technicians switching from solvent to UV systems.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Shift to RoHS-Compliant Low-VOC Water/UV Systems

- Expansion of Telecom Infrastructure and 5G Rollout

- Silicone-Monomer Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylics led the conformal coatings market with 44.24% share in 2025 and are forecast to grow at 6.88% CAGR as assemblers value low cost, broad compatibility, and easy rework. Silicone chemistries, meanwhile, deliver -60 °C to +200 °C stability and low modulus that preserves solder joint integrity under thermal cycling, justifying premium pricing. Epoxies remain entrenched in under-hood automotive boxes for their chemical resistance, although brittleness limits take-rate. Urethanes and polyurethanes win in foldable devices demanding flex life above 100,000 cycles. Emerging fluoropolymer nano-coatings are logging demand for sub-10 µm films with contact angles more than 110° that repel sweat in wearables.

Silicone's KRW-6000, launched by Shin-Etsu in 2024, marries water dispersibility with 30-minute cure at 150 °C, answering OEM calls for RoHS compliance without throughput penalties. Total cost-of-ownership now dictates material decisions, blending raw resin price with capital, cure-energy loads, and end-of-life disposal under extended producer rules in Europe and Japan. IPC-CC-830C Type AR and Type SR products account for 75% of market qualifications, yet the 2024 IPC-HDBK-830A update formally added fluoropolymer guidance, foreshadowing next-gen adoption. Advanced hybrids, such as dual-cure epoxy-acrylate blends, target BMS power modules requiring 4 kV/mm dielectric strength and >=1 W/mK thermal conductivity.

Solvent-based still occupy 55.78% of the conformal coatings market size in 2025, owing to broad wetting and established approvals across automotive PPAPs. UV-cured, however, are accelerating at 7.13% CAGR through 2031, driven by zero-VOC status, one-second cures, and energy savings that cut oven power by 80%. Water-based systems gain favor where regulation trumps throughput, rising to nearly one-fifth of volume despite 60-minute dry times at 80 °C. Hybrid chemistries serve potting and encapsulation roles in high-voltage inverters.

EMS giants in Vietnam installed over 200 UV-LED tunnels in 2024 to coat smartphone antennas and wireless charging coils, trimming floor space 30%. Automotive trials on LiDAR modules show UV silicones slicing tack-free time from 45 minutes to 60 seconds while sustaining MIL-STD-810H performance. Nordson's Q2 2024 saw Industrial Precision Solutions rise 2% on coatings equipment even as semiconductor demand sagged 22% in its Advanced Technology arm. Persistent barriers include opaque-film AOI limits, but integration of in-situ fluorometry now validates 50 µm thickness in real time, mitigating defects before cure.

Geography Analysis

Asia-Pacific generated 42.35% of conformal coatings market revenue in 2025 and is accelerating at 7.67% CAGR through 2031. China rebounded in 2024 as smartphone and data center projects resumed, with Henkel citing double-digit electronics growth. ASEAN nations secured USD 31 billion electronics FDI in 2024, cementing their role as back-end semiconductor hubs. India's PLI incentives and 5G base-station buildout are spurring RoHS-compliant coating lines tied to Bureau of Indian Standards approvals. South Korea and Japan remain innovation centers for flex displays and automotive electronics, prompting suppliers to open tech centers in Seoul and Tokyo.

North America's demand is supported by aerospace, defense, and EV manufacturing. The CHIPS and Science Act and Inflation Reduction Act will funnel more than USD 100 billion toward domestic fabs through 2030, boosting demand for IPC-qualified coatings . 3M's Electronics division launched 169 new products in 2024, showing a push for protective materials in semiconductor packaging. Mexico's Baja California corridor is becoming an EV electronics hot spot, while Canada's Montreal cluster services avionics coating needs.

In Europe, Germany, France, and the United Kingdom enforce strict RoHS and REACH standards, propelling water-based and UV chemistries. Dow's Performance Materials & Coatings reported USD 8.497 billion sales in 2023, with silicones serving European auto and industrial clients. Nordic EV battery gigafactories and offshore wind converters need salt-fog-resistant coatings. South America and the Middle East and Africa remain nascent but are growing as Brazil's auto sector and Saudi smart-city projects specify protective films for harsh climates.

- 3M

- Actnano Inc.

- Altana AG

- Bostik (Arkema)

- Chase Corp.

- Chemtronics (KEMET)

- CHT UK Ltd

- Dow

- Dymax

- Electrolube

- Europlasma NV

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.

- MG Chemicals

- Nordson Corporation

- Panacol-Elosol GmbH

- PVA

- Shin-Etsu Chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G Smartphones and IoT Wearables Require Mini-Circuit Protection

- 4.2.2 LEO Satellites and Avionics Electronics Need High-Performance Coatings

- 4.2.3 Regulatory Shift to Rohs-Compliant Low-VOC Water/UV Systems

- 4.2.4 Expansion of Telecom Infrastructure and 5G Rollout

- 4.2.5 Increasing Aerospace and Defence Electronics Applications

- 4.3 Market Restraints

- 4.3.1 Rework/Inspection Complexity of UV-Cured Opaque Films

- 4.3.2 Silicone-Monomer Price Volatility

- 4.3.3 Scarcity of High-Purity Parylene Dimer

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Urethane/Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Material Types (Fluoropolymer, Nano-coatings)

- 5.2 By Technology

- 5.2.1 Solvent-Based

- 5.2.2 Water-Based

- 5.2.3 UV-Cured

- 5.2.4 Hybrid/Other Advanced Systems

- 5.3 By Operation Method

- 5.3.1 Spray Coating (Atomised/Film)

- 5.3.2 Dip Coating

- 5.3.3 Brush Coating

- 5.3.4 Other Operation Methods (Selective/Robotic Dispense and Chemical Vapour Deposition (CVD))

- 5.4 By End-user Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive (ICE, EV, ADAS)

- 5.4.3 Aerospace and Defense

- 5.4.4 Medical and Life-Sciences Electronics

- 5.4.5 Other End-user Industries (Industrial, Power and Energy)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 NORDIC Countries

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Actnano Inc.

- 6.4.3 Altana AG

- 6.4.4 Bostik (Arkema)

- 6.4.5 Chase Corp.

- 6.4.6 Chemtronics (KEMET)

- 6.4.7 CHT UK Ltd

- 6.4.8 Dow

- 6.4.9 Dymax

- 6.4.10 Electrolube

- 6.4.11 Europlasma NV

- 6.4.12 H.B. Fuller Company

- 6.4.13 Henkel AG & Co. KGaA

- 6.4.14 Illinois Tool Works Inc.

- 6.4.15 MG Chemicals

- 6.4.16 Nordson Corporation

- 6.4.17 Panacol-Elosol GmbH

- 6.4.18 PVA

- 6.4.19 Shin-Etsu Chemical Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment