PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066508

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066508

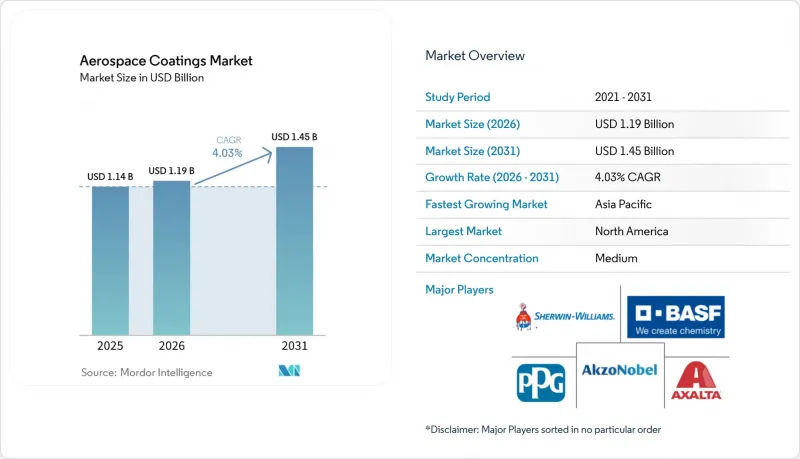

Aerospace Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aerospace coatings market size is projected to be USD 1.14 billion in 2025, USD 1.19 billion in 2026, and reach USD 1.45 billion by 2031, growing at a CAGR of 4.03% from 2026 to 2031.

This report is Segmented by Resin Type (Epoxy, Polyurethane, Acrylic, and Other Resin Types), Technology (Solvent-Borne, Water-Borne, and Other Technologies), End User (Original Equipment Manufacturer and Maintenance Repair and Operations), Aviation Type (Commercial, Military, and General), and Geography (Asia-Pacific, North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Aerospace Coatings Market Trends and Insights

Rising Production Rates of Commercial Aircraft

In 2025, families like the 737 MAX and A320neo, both single-aisle aircraft, averaged high monthly airframe completion rates. With Airbus projecting a significant number of deliveries for the year, the uptick in build rates translates to heightened volumes of primer and topcoat. This is due to wide-body aircraft requiring more surface coverage compared to their narrow-body counterparts. However, ongoing supply-chain challenges, particularly in titanium forgings and composite prepregs, have led to deferrals in some paint-booth slots, resulting in delayed recognition into later quarters. As a workaround, existing spray lines are operating on dual shifts. This is a temporary measure until the new automated booths, which come with lead times of 18 to 24 months, become operational. Furthermore, the surge in throughput amplifies the demand for quality assurance, especially in areas like in-line color matching and film thickness monitoring.

Increasing Use of Composites in Aircraft Manufacturing

Carbon-fiber structures now make up a significant portion of the weight in Boeing's 787 and Airbus's A350, a notable increase from older aluminum fuselages. Epoxy primers, now standard, utilize chromate-free inhibitors. These primers effectively bond with hydroxyl-rich fiber surfaces while steering clear of galvanic corrosion. Formulators incorporate triazole and rare-earth additives to meet required benchmarks. While conductive top coats, which ensure surface resistivity stays low, add to material costs, they're essential for lightning-strike dissipation. Room-temperature-cure epoxy, which bonds without the need for autoclave heat, further enhances composite repairs in service. However, it's worth noting that only a select few suppliers possess current FAA approvals.

Concerns of Volatile Organic Compound Emissions

U.S. regulations limit primer volatile-organic-compound content and top coats. The European Union plans to implement these same limits by 2028. Adhering to these standards increases raw material costs as formulators shift to slower-evaporating solvents. Consequently, paint-shop cycle times extend, leading to reduced throughput. While water-borne alternatives can more readily meet these regulations, they require humidity-controlled booths, which produce higher wastewater loads, posing a challenge for smaller maintenance operations. This financial hurdle is driving a trend of consolidation, favoring larger MRO houses with more robust cash flows.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Air Travel

- Accelerating Maintenance, Repair and Overhaul Demand for Aging Fleets

- Lengthy Certification Cycles for New Chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy held 58.36% of the aerospace coatings market share in 2025, and the segment is expected to grow at a 4.22% CAGR to 2031, underscoring a robust demand, particularly in composite-rich fuselages. Polyurethanes, securing the second position, are the top choice for airlines seeking ultraviolet-stable top coats. However, it's worth noting that as suppliers incorporate light-stabilizer packages, the prices of these raw materials are on the rise.

Acrylics, prized for their dielectric properties, cater to specialty radome niches. Yet, their limited chemical resistance curtails wider adoption. Meanwhile, the silicone and fluoropolymer families are experiencing sluggish growth. This is largely due to emerging PFAS restrictions, which pose challenges for OEM qualification. Furthermore, the lengthy certification timelines, often spanning several years, act as a deterrent for disruptive newcomers. As a result, the existing resin hierarchies remain firmly entrenched, at least until the next regulatory cycle.

Solvent technologies accounted for 54.41% of revenue in 2025, supported by established performance records on military fleets and legacy narrow-body lines. Water-borne systems are advancing at a 4.18% CAGR through 2031 because they meet evolving emission limits without booth-air incineration.

Adoption hurdles linger. Water-borne films cure more slowly in high humidity and produce extra wastewater. Powder coating stays confined to landing-gear and cabin parts because the 180 °C bake impeded composites. MIL-PRF specifications that date back decades ensure a baseline of demand that shields solvent chemistries from rapid displacement.

Geography Analysis

North America supplied 40.05% of revenue in 2025, reflecting Boeing assembly in Washington State and an extensive legacy MRO sector. Domestic labor rates, however, motivate carriers to ferry jets to Asia for heavy paint work, tempering volume growth in the region. Europe holds the second-largest position thanks to Airbus' final-assembly lines in Toulouse and Hamburg and to aggressive emission rules that push technical innovation.

Asia-Pacific is the fastest-expanding region at 3.22% CAGR, driven by Chinese and Indian manufacturing initiatives and by its role as a global transit hub. COMAC aims for local content but continues to import essential epoxy primers until domestic suppliers obtain FAA or EASA approvals. However, the Middle East's high concentration of wide-body operators bolsters the demand for coatings, particularly ultraviolet-resistant top coats essential for desert climates.

Tariff regimes and currency swings influence procurement decisions in emerging markets. Brazilian real depreciation, for instance, raises imported resin costs and prolongs reliance on proven solvent-borne systems despite regulatory pressure elsewhere.

- Advanced Deposition & Coating Technologies, Inc.

- Akzo Nobel N.V.

- Axalta Coating Systems, LLC

- BASF SE

- BryCoat Inc.

- Henkel AG & Co. KGaA

- Hentzen Coatings, Inc.

- Ionbond

- Jotun

- Mankiewicz Gebr. & Co.

- PPG Industries, Inc.

- Socomore

- The Sherwin-Williams Company

- Zircotec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising production rates of commercial aircraft

- 4.2.2 Increasing use of composites in aircraft manufacturing

- 4.2.3 Increasing Demand for Air Travel

- 4.2.4 Accelerating Mainenance, Reapir and Overhaul demand for aging fleets

- 4.2.5 Increase in Manufacturing of Aircrafts in Emerging Economies

- 4.3 Market Restraints

- 4.3.1 Concerns of VOC emissions

- 4.3.2 Lengthy certification cycles for new chemistries

- 4.3.3 Early substitution risk from next-gen fluoropolymer films

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Other Resin Types (Silicone, Fluoropolymer, etc.)

- 5.2 By Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.2.3 Other Technologies (Powder,etc.)

- 5.3 By End User

- 5.3.1 Original Equipment Manufacturer (OEM)

- 5.3.2 Maintenance, Repair and Operations (MRO)

- 5.4 By Aviation Type

- 5.4.1 Commercial Aviation

- 5.4.2 Military Aviation

- 5.4.3 General Aviation

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information,Products and Services, and Recent Developments)

- 6.4.1 Advanced Deposition & Coating Technologies, Inc.

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Axalta Coating Systems, LLC

- 6.4.4 BASF SE

- 6.4.5 BryCoat Inc.

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Hentzen Coatings, Inc.

- 6.4.8 Ionbond

- 6.4.9 Jotun

- 6.4.10 Mankiewicz Gebr. & Co.

- 6.4.11 PPG Industries, Inc.

- 6.4.12 Socomore

- 6.4.13 The Sherwin-Williams Company

- 6.4.14 Zircotec

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment