PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066513

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066513

Laboratory Informatics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

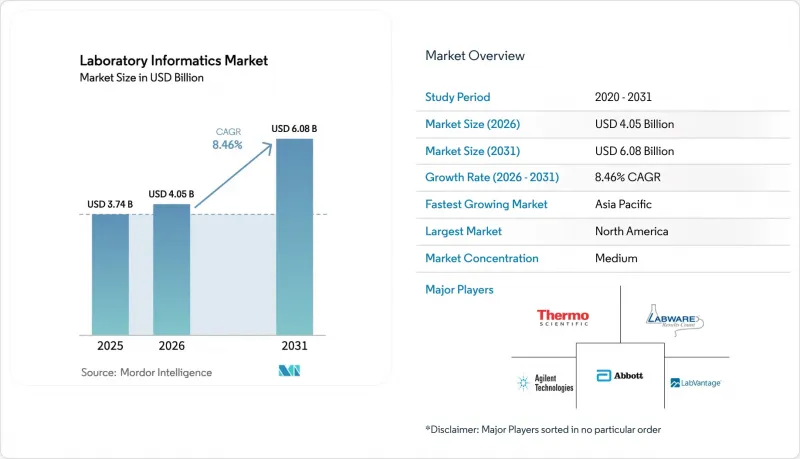

According to Mordor Intelligence, the laboratory informatics market size is projected to be USD 3.74 billion in 2025, USD 4.05 billion in 2026, and reach USD 6.08 billion by 2031, growing at a CAGR of 8.46% from 2026 to 2031.

This report is Segmented by Product (LIMS, ELN, ECM, LES, CDS, and Other Products), Component (Services and Software), Delivery Mode (On-Premise, Web-Hosted, and Cloud-Based), End User (Pharmaceutical & Biotechnology Companies, Cros, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). Market Forecasts are Provided in Terms of Value (USD).

Global Laboratory Informatics Market Trends and Insights

Growing Regulatory Emphasis on Data Integrity and Compliance

Regulators tightened electronic-record enforcement, making validated informatics indispensable for submissions. In 2024, FDA warning letters cited inadequate audit trails, prompting widespread adoption of LIMS across QC laboratories. EMA Annex 11 and the finalized ICH Q2(R2)/Q14 guidelines extend similar expectations in Europe. ISO 17025 revisions now reference electronic data management, prompting smaller testing labs to favor subscription-based, cloud-hosted solutions that embed validation artifacts and eliminate capital expense. Collectively, these mandates accelerate enterprise transitions away from paper logbooks toward platforms offering role-based access, version control, and automated deviation alerts.

Rising Adoption of Cloud-Based Laboratory Informatics Platforms

Cloud deployments commanded 53.24% share in 2025 and are expanding at a 13.21% CAGR, as life-science firms scale capacity during trial surges without procuring new servers. Waters Empower 4 synchronizes chromatography data to AWS or Azure within minutes, empowering remote QA review and round-the-clock operations. European laboratory societies now recommend the use of geographically distributed data centers and 24-hour backups to counter ransomware threats. Upload latency for terabyte-scale NGS files remains a hurdle; vendors are embedding edge computing to trim bandwidth by nearly 40%. The validation scope broadens in the cloud era, compelling routine audits of underlying infrastructure to meet FDA guidance published in 2024.

High Upfront Implementation and Validation Costs

A single LIMS roll-out in a pharmaceutical QC lab can cost USD 500,000 to USD 2 million, with validation consuming as much as 40% of the budget. Thermo Fisher estimates 3,000-5,000 consulting hours per deployment, a barrier for mid-tier organizations. While SaaS subscriptions remove server outlays, annual fees often exceed USD 100,000 for a 50-user license. Payback periods extend beyond three years, deterring labs that face uncertain revenue streams.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Precision Medicine and Genomics Research

- Integration Of Artificial Intelligence and Advanced Analytics

- Data Security and Privacy Concerns in Cloud Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Geography Analysis

North America retained a 48.72% share in 2025, largely due to rigorous FDA enforcement and the presence of dense biopharma clusters. The FDA issued 18 data-integrity warning letters in 2024 alone, catalyzing rapid system upgrades. Canada adopted ICH Q2(R2) in 2024, prompting CAD 2.8 billion (USD 2.1 billion) in laboratory digitalization projects[3]. Growth moderates as the installed base matures and replacement cycles lengthen to nearly a decade.

Asia-Pacific is forecast to record a 9.21% CAGR through 2031, propelled by India's ambitions to double its pharmaceutical market to USD 130 billion by 2030. China's NMPA mandated electronic batch records with audit trails in 2024, accelerating local demand for compliant LIMS solutions. Japan's digital health expansion, projected to grow at an 11.9% CAGR through 2032, further underpins the regional upside.

Europe maintains steady adoption, buoyed by GDPR and Annex 11. Germany invested EUR 1.9 billion (USD 2.1 billion) in 2024 to modernize pharmaceutical labs, with AI-enhanced LIMS deployed at BASF and Bayer. The June 2024 Synnovis ransomware event prompted UK authorities to mandate endpoint detection across all laboratory IT systems. Middle Eastern laboratories pursue ISO 17025 accreditation to enhance export credibility, while South American uptake remains preliminary, pending national e-record mandates.

- Abbott (STARLIMS Corporation)

- Accelerated Technology Laboratories (ATL)

- Agilent Technologies

- Autoscribe Informatics

- Axtria

- Benchling Inc.

- Clinisys, Inc.

- Dassault Systemes SE (BIOVIA)

- Dotmatics Ltd.

- Illumina

- IDBS (Danaher)

- LabCollector (AgileBio)

- LabLynx

- LabVantage Solutions

- LabWare

- Oracle

- PerkinElmer

- Siemens Healthineers

- Thermo Fisher Scientific

- Waters Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Regulatory Emphasis on Data Integrity and Compliance

- 4.2.2 Rising Adoption of Cloud-Based Laboratory Informatics Platforms

- 4.2.3 Expansion of Precision Medicine and Genomics Research

- 4.2.4 Integration of Artificial Intelligence and Advanced Analytics

- 4.2.5 Increasing Outsourcing of R&D to Contract Organizations

- 4.2.6 Pandemic-Led Shift Toward Remote and Digital Laboratory Workflows

- 4.3 Market Restraints

- 4.3.1 High Upfront Implementation and Validation Costs

- 4.3.2 Data Security and Privacy Concerns in Cloud Deployment

- 4.3.3 Legacy Instrument Integration Challenges

- 4.3.4 Shortage of Skilled Bioinformatics and IT Personnel

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Buyers/Consumers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value / USD)

- 5.1 By Product

- 5.1.1 Laboratory Information Management System (LIMS)

- 5.1.2 Electronic Lab Notebooks (ELN)

- 5.1.3 Enterprise Content Management (ECM)

- 5.1.4 Laboratory Execution System (LES)

- 5.1.5 Chromatography Data System (CDS)

- 5.1.6 Other Products

- 5.2 By Component

- 5.2.1 Services

- 5.2.2 Software

- 5.3 By Delivery Mode

- 5.3.1 On-Premise

- 5.3.2 Web-Hosted

- 5.3.3 Cloud-Based

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Research Organizations (CROs)

- 5.4.3 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products & Services, and Analysis of Recent Developments)

- 6.3.1 Abbott (STARLIMS Corporation)

- 6.3.2 Accelerated Technology Laboratories (ATL)

- 6.3.3 Agilent Technologies Inc.

- 6.3.4 Autoscribe Informatics

- 6.3.5 Axtria

- 6.3.6 Benchling Inc.

- 6.3.7 Clinisys, Inc.

- 6.3.8 Dassault Systemes SE (BIOVIA)

- 6.3.9 Dotmatics Ltd.

- 6.3.10 Illumina Inc.

- 6.3.11 IDBS (Danaher)

- 6.3.12 LabCollector (AgileBio)

- 6.3.13 LabLynx Inc.

- 6.3.14 LabVantage Solutions Inc.

- 6.3.15 LabWare

- 6.3.16 Oracle

- 6.3.17 PerkinElmer Inc.

- 6.3.18 Siemens Healthineers AG

- 6.3.19 Thermo Fisher Scientific Inc.

- 6.3.20 Waters Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment