PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066515

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066515

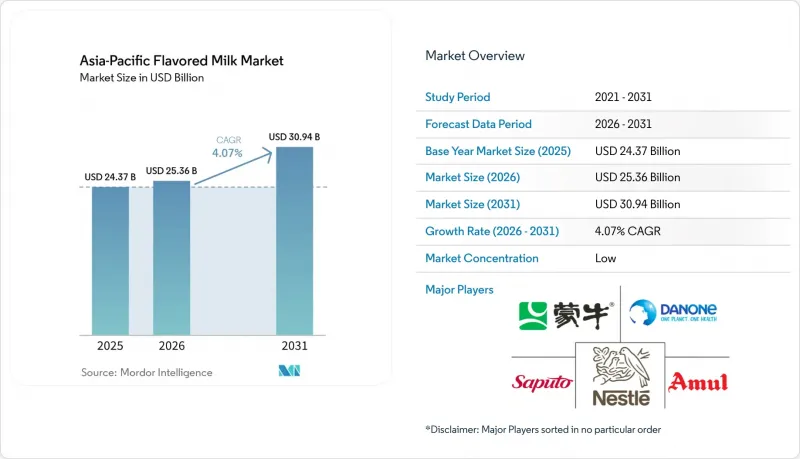

Asia-Pacific Flavored Milk - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific flavored milk market size is projected to expand from USD 24.37 billion in 2025 and USD 25.36 billion in 2026 to USD 30.94 billion by 2031, registering a 4.07% CAGR between 2026 and 2031.

This report is Segmented by Product Type (Dairy-Based and Plant-Based), Flavor Profile (Chocolate, Strawberry, Vanilla, and Others), Packaging Type (PET/Glass Bottles, Cans, Tetra Pak, and Others), Distribution Channels (On-Trade, and Off-Trade), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Flavored Milk Market Trends and Insights

Rising Demand for Health-Centric Dairy Products

Consumers across Asia-Pacific increasingly view flavored milk as a functional beverage rather than an indulgent treat, driving demand for low-sugar, high-protein, and probiotic-enriched variants. Tetra Pak's 2025 consumer research found that 62% of respondents prioritize physical health when selecting dairy products, and 59% express interest in ready-to-drink liquid formats that deliver convenience without compromising nutrition. This shift is most pronounced in Japan and South Korea, where aging populations seek calcium and vitamin D fortification to mitigate osteoporosis risk, and in Australia, where lactose-free and A2 protein milk cater to digestive sensitivities. Manufacturers respond by reformulating existing SKUs: Vinamilk upgraded its chocolate milk in December 2025 to contain 2.5 times more chocolate while reducing fat by 21%, and introduced Vinamilk Flex with 70% more calcium than its no-sugar nutritional milk baseline, fortified with vitamin D3 for absorption. The trend extends to plant-based offerings, where soy and oat variants are fortified with B12, calcium, and omega-3 to match dairy's nutritional profile, blurring the line between indulgence and wellness.

Rising Disposable Incomes in Emerging Countries

Rising per capita incomes in China, India, Indonesia, and Vietnam are driving a shift among millions of households from unbranded dairy products to packaged, branded flavored milk. According to China's National Bureau of Statistics, per capita disposable income reached USD 6,025 in 2025, reflecting a 5.0% increase in real terms. Urban incomes averaged USD 7,848, while rural incomes stood at USD 3,397. This income growth corresponds with a 9.3% year-on-year rise in retail sales of grains, oils, and food products, alongside a 26.1% share for online retail, emphasizing a shift toward modern, traceable supply chains. In India, Amul reported a FY25 turnover of INR 90,000 crore (USD 1,078 billion) and aims to achieve INR 100,000 crore (USD 1,198 billion) within two years. This goal is supported by an INR 10,000 crore (USD 120 billion) expansion plan, which includes a new processing plant in Assam with a daily capacity of 100,000 liters, costing USD 12 million. In Indonesia, the "Free Nutritious Meals" program, launched in January 2025 and targeting 83 million children, is generating institutional demand for fortified flavored milk. However, economic slowdowns during the first half of 2025 have impacted middle-class purchasing power, highlighting the sector's sensitivity to macroeconomic conditions, as reported by the Government of Indonesia.

Concerns about High Sugar Content in Flavored Milk

Public health campaigns and regulatory mandates targeting added sugar are pressuring manufacturers to reformulate or risk losing shelf space and consumer trust. India's Food Safety and Standards Authority issued draft amendments in February 2025 requiring bold, larger fonts for added sugar, saturated fat, and sodium declarations, along with the percentage of the recommended daily allowance, directly impacting flavored milk SKUs that often exceed 10 grams of sugar per 100 ml. Australia's FSANZ and Japan's Ministry of Health, Labour and Welfare have signaled similar front-of-pack labeling initiatives, creating compliance costs and potential SKU rationalization. Manufacturers respond by launching reduced-sugar variants, Vinamilk's upgraded chocolate milk cuts fat by 21% while increasing chocolate intensity, and Vinamilk Flex contains no added sugar, but these reformulations risk alienating consumers accustomed to sweeter profiles. The tension between health positioning and taste preference is most acute in children's segments, where parents demand nutrition but children drive purchase decisions based on flavor.

Other drivers and restraints analyzed in the detailed report include:

- Product Innovation, Including Plant-Based Variants and Local Flavors

- Rising Consumption of Fortified and Functional Milk Products

- Prevalence of Lactose Intolerance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, dairy-based flavored milk accounted for 88.32% of the market revenue, driven by strong consumer preferences, a robust cold-chain infrastructure, and competitive pricing. However, plant-based alternatives are set to grow at a 5.54% CAGR through 2031, as manufacturers address the needs of lactose-intolerant consumers and respond to increasing sustainability demands. Within the dairy segment, cow milk remains the primary choice, supporting the majority of chocolate, strawberry, and vanilla products. In contrast, goat milk occupies a niche market, focusing on premium, digestibility-oriented products targeted at infants and elderly consumers. Buffalo and camel milk cater to hyper-local markets in India and the Middle East but lack the scale to influence broader regional trends. The plant-based sector is diversifying into soy, almond, oat, and hybrid blends, each appealing to specific consumer groups. Soy attracts cost-conscious households seeking protein, almond appeals to health-focused urban consumers willing to pay a premium, and oat resonates with environmentally conscious millennials and Gen Z. Nestle's Bear Brand Milk N' Soy, launched in the Philippines in May 2025, exemplifies this hybrid innovation. By combining dairy and soy with enzyme technology to eliminate the beany flavor and gritty texture, Nestle expands its market reach without cannibalizing its core dairy sales.

Oatside's Nobo Soy, introduced in March 2026 in Singapore and Malaysia, taps into the 48% of Malaysian consumers who have increased their plant-based consumption. Meanwhile, Farm Fresh's gula melaka and Ichiba Melon UHT variants demonstrate how local flavors can drive consumer trials, even in emerging plant-based categories. Regulatory frameworks are increasingly distinguishing between dairy and plant-based products. For example, India's FSSAI requires flavored milk to meet specific fat and solids-not-fat standards and mandates clear heat treatment declarations. Conversely, plant-based beverages are prohibited from using the term "milk" unless it is prefixed with the plant source. While these regulations reduce consumer confusion, they also limit plant-based brands' ability to leverage dairy's established health reputation. As a result, plant-based brands are focusing on building independent identities centered on sustainability, allergen-free claims, and functional fortification.

Chocolate flavor held 44.59% of 2025 revenue, benefiting from universal appeal, established supply chains for cocoa powder and chocolate compounds, and IP-driven product launches such as Mengniu's Tom & Jerry co-branded milk and Oak's Rolo collaboration with Nestle in Australia, yet strawberry will grow at 6.67% CAGR through 2031 as manufacturers target younger demographics with fruit-forward, lower-sugar formulations. Vanilla occupies a stable third position, serving as a base for customization in foodservice channels where baristas add syrups and toppings, while "others", including local flavors like kesar badam, gula melaka, matcha, taro, and tropical fruits, are the fastest-innovating segment, with launches in 2025-2026 demonstrating appetite for novelty. Parle Agro's Smoodh Kesar Badam, introduced in February 2026, combines saffron and almond in 80 ml and 150 ml packs priced at INR 10 and INR 20, leveraging cultural resonance and affordability to penetrate both urban and rural markets.

Flavor preferences vary sharply by geography: chocolate dominates in China, India, and Southeast Asia, where Western confectionery associations drive trial; strawberry performs strongly in Japan and South Korea, where fruit-flavored dairy has deep cultural roots; and local flavors such as taro and matcha resonate in East Asia, with Binggrae's Taro Flavoured Milk achieving cult status in South Korea and export markets like New Zealand. Manufacturers face a strategic trade-off: chocolate and strawberry deliver volume and margin predictability, but local flavors generate buzz, social-media engagement, and premiumization opportunities. The rise of bubble tea, projected to grow from USD 2.83 billion to USD 4.78 billion by 2032, creates crossover demand for flavored milk as a base ingredient, with cafes and QSRs incorporating taro, matcha, and fruit-flavored milk into boba lattes and smoothies, blurring the line between retail and foodservice segments

List of Companies Covered in this Report:

- China Mengniu Dairy Co. Ltd.

- Inner Mongolia Yili Industrial Group Co. Ltd.

- Gujarat Co-operative Milk Marketing Federation Ltd. (Amul)

- Nestle S.A.

- Danone S.A.

- FrieslandCampina N.V.

- Saputo Inc.

- Arla Foods Amba

- Meiji Holdings Co. Ltd.

- Morinaga Milk Industry Co. Ltd.

- Lotte Foods Co. Ltd.

- Bright Food (Group) Co. Ltd.

- Dairy Farmers of America Inc.

- Dean Foods Company

- Grupo Lala S.A.B. de C.V.

- Fonterra Co-operative Group Ltd.

- a2 Milk Company Ltd.

- Parle Agro Pvt. Ltd.

- Mother Dairy Fruit & Vegetable Pvt. Ltd.

- Hiland Dairy Foods Company

- Umang Dairies Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Health-Centric Dairy Products

- 4.2.2 Rising disposable incomes in emerging Countries

- 4.2.3 Product Innovation, Including Plant-Based Variants and Local Flavors

- 4.2.4 Rising Consumption of Fortified and Functional Milk Products

- 4.2.5 Increasing Modern Retail Expansion in the Region

- 4.2.6 Rising Inclination Towards Protein-Rich and Nutrient Dense Beverages

- 4.3 Market Restraints

- 4.3.1 Concerns about High Sugar Content in Flavored Milk

- 4.3.2 Prevalance of Lactose Intolerance

- 4.3.3 Supply Chain Inefficieneces in the region

- 4.3.4 Stringent Food Safety and Labeling Regulations

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Product Type

- 5.1.1 Dairy Based

- 5.1.1.1 Cow

- 5.1.1.2 Goat

- 5.1.1.3 Others

- 5.1.2 Plant Based

- 5.1.2.1 Soy

- 5.1.2.2 Almond

- 5.1.2.3 Oats

- 5.1.2.4 Others

- 5.1.1 Dairy Based

- 5.2 Flavor Profile

- 5.2.1 Chocolate

- 5.2.2 Strawberry

- 5.2.3 Vanilla

- 5.2.4 Others

- 5.3 Packaging Type

- 5.3.1 PET/Glass Bottles

- 5.3.2 Cans

- 5.3.3 Tetra Pak

- 5.3.4 Others

- 5.4 Distribution Channels

- 5.4.1 On-Trade

- 5.4.2 Off-Trade

- 5.4.2.1 Supermarkets/Hypermarkets

- 5.4.2.2 Specialist Retailers

- 5.4.2.3 Convenience Stores

- 5.4.2.4 Online Retail

- 5.4.2.5 Other Distribution Channels

- 5.5 Geography

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 Australia

- 5.5.5 South Korea

- 5.5.6 Vietnam

- 5.5.7 Indonesia

- 5.5.8 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 China Mengniu Dairy Co. Ltd.

- 6.4.2 Inner Mongolia Yili Industrial Group Co. Ltd.

- 6.4.3 Gujarat Co-operative Milk Marketing Federation Ltd. (Amul)

- 6.4.4 Nestle S.A.

- 6.4.5 Danone S.A.

- 6.4.6 FrieslandCampina N.V.

- 6.4.7 Saputo Inc.

- 6.4.8 Arla Foods Amba

- 6.4.9 Meiji Holdings Co. Ltd.

- 6.4.10 Morinaga Milk Industry Co. Ltd.

- 6.4.11 Lotte Foods Co. Ltd.

- 6.4.12 Bright Food (Group) Co. Ltd.

- 6.4.13 Dairy Farmers of America Inc.

- 6.4.14 Dean Foods Company

- 6.4.15 Grupo Lala S.A.B. de C.V.

- 6.4.16 Fonterra Co-operative Group Ltd.

- 6.4.17 a2 Milk Company Ltd.

- 6.4.18 Parle Agro Pvt. Ltd.

- 6.4.19 Mother Dairy Fruit & Vegetable Pvt. Ltd.

- 6.4.20 Hiland Dairy Foods Company

- 6.4.21 Umang Dairies Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK