PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066518

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066518

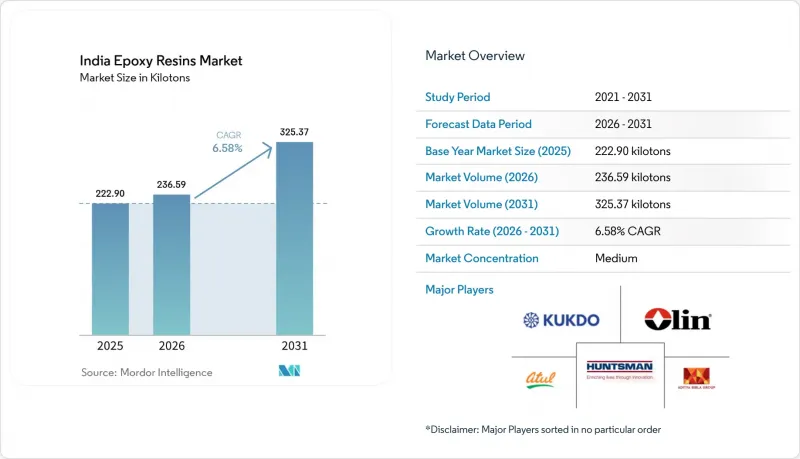

India Epoxy Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india epoxy resins market size was valued at 222.90 kilotons in 2025 and is estimated to grow from 236.59 kilotons in 2026 to reach 325.37 kilotons by 2031, at a CAGR of 6.58% during the forecast period (2026-2031).

This report is Segmented by Raw Material (DGEBA, DGEBF, Novolac, Aliphatic, Glycidylamine, and Other Raw Materials), and Application (Paints and Coatings, Adhesives and Sealants, Composites, Electrical and Electronics, and Other Applications). The Market Forecasts are Provided in Terms of Volume (Tons).

India Epoxy Resins Market Trends and Insights

Surging Infrastructure Spending in Tier-2 and Tier-3 Cities

Government missions to modernize secondary cities are driving robust uptake of heavy-duty epoxy flooring, protective coatings, and structural adhesives for new malls, hospitals, and education facilities. These locations offer greenfield demand where competitive pricing pressure is lower than in metros, enabling producers to sustain margins. Developers prefer seamless, hygienic epoxy floors that outperform ceramic and terrazzo alternatives, while contractors appreciate shorter project turnaround times. Manufacturing hubs in Gujarat and Maharashtra supply most of the resin volumes, benefitting from nearby ports and integrated petrochemical feedstocks. Suppliers that expand distribution into interior districts can capture incremental volume growth as construction activity spreads beyond coastal metros.

Automotive Lightweighting Push from FY 2025 CAFE Norms

Stricter Corporate Average Fuel Economy rules oblige automakers to lower fleet emissions, spurring adoption of carbon-fiber-epoxy composites for body panels, structural parts, and battery enclosures. The government's INR 25,938 crore (USD 3.1 billion) vehicle PLI scheme, restricted to EV, hybrid, and fuel-cell platforms, accelerates intermediate demand for advanced adhesives and thermally conductive epoxy potting compounds. Tier-1 suppliers leverage India's proven capability in scaled electronics assembly to localize composite sub-component fabrication, increasing resin off-take. Lightweighting is a structural necessity rather than a short-term volume swing, ensuring consistent consumption growth.

BIS Draft Limits on BPA Residuals in Resins

Proposed Quality Control Orders impose stringent caps on unreacted bisphenol A content, compelling manufacturers to invest in purification, alternative curing agents, or BPA-free chemistries. Large integrated producers with robust research and development funding can adjust formulations swiftly and may leverage compliance credentials in export markets. Smaller regional firms risk margin compression and potential consolidation if capital requirements exceed liquidity.

Other drivers and restraints analyzed in the detailed report include:

- Wind-Turbine Blade Additions Under India's 500 GW Renewables Target

- Government PLI Scheme for Advanced Chemistry Cell Battery Packs

- Volatile Propylene and Phenol Feedstock Prices Linked to Crude Swings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DGEBA accounted for 64.02% of India Epoxy Resin market share in 2025 and is forecast to post an 8.05% CAGR to 2031. The composition yields excellent mechanical strength, chemical resistance, and cost efficiency, supporting wide penetration in coatings, electrical insulation, and composites. DGEBF targets electronics and high-temperature sectors that require lower viscosity and higher thermal stability. Novolac systems fill niches needing exceptional chemical resistance, such as chemical-processing tank linings. Aliphatic resins deliver superior UV stability for decorative finishes, while glycidylamine grades provide high adhesion to metals and impact resistance, serving marine and aerospace coatings. Other raw materials include bio-based and specialty chemistries now emerging in response to sustainability mandates.

Producers use incremental innovations-faster cure, low-VOC blends, and BPA-reduced options-to address upcoming standards. Competitive tension may intensify if BPA residual limits push formulators toward DGEBF or bio-epoxies; however, current price-performance advantages make large-scale substitution unlikely before 2030.

List of Companies Covered in this Report:

- 3M

- Aditya Birla Group

- Atul Ltd

- BASF

- Daicel Corporation

- DuPont

- Huntsman International LLC

- Kukdo Chemical Co., Ltd.

- Macro Polymers Pvt Ltd

- Nan Ya Plastics Corporation

- Olin Corporation

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging infrastructure spending in Tier-2 and Tier-3 cities

- 4.2.2 Automotive lightweighting push from FY 2025 CAFE norms

- 4.2.3 Wind-turbine blade additions under India's 500 GW renewables target

- 4.2.4 Government PLI scheme for advanced chemistry cell (ACC) battery packs (encapsulants)

- 4.2.5 Rapid growth of organised retail flooring and decorative laminates

- 4.3 Market Restraints

- 4.3.1 BIS draft limits on BPA residuals in resins

- 4.3.2 Volatile propylene and phenol feedstock prices linked to crude swings

- 4.3.3 Rising popularity of bio-based unsaturated polyester alternatives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Raw Material

- 5.1.1 DGEBA (Bisphenol A and ECH)

- 5.1.2 DGEBF (Bisphenol F and ECH)

- 5.1.3 Novolac (Formaldehyde and Phenols)

- 5.1.4 Aliphatic (Aliphatic Alcohols)

- 5.1.5 Glycidylamine (Aromatic Amines and ECH)

- 5.1.6 Other Raw Materials

- 5.2 By Application

- 5.2.1 Paints and Coatings

- 5.2.2 Adhesives and Sealants

- 5.2.3 Composites

- 5.2.4 Electrical and Electronics

- 5.2.5 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Aditya Birla Group

- 6.4.3 Atul Ltd

- 6.4.4 BASF

- 6.4.5 Daicel Corporation

- 6.4.6 DuPont

- 6.4.7 Huntsman International LLC

- 6.4.8 Kukdo Chemical Co., Ltd.

- 6.4.9 Macro Polymers Pvt Ltd

- 6.4.10 Nan Ya Plastics Corporation

- 6.4.11 Olin Corporation

- 6.4.12 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment