PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066524

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066524

Seed Processing Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

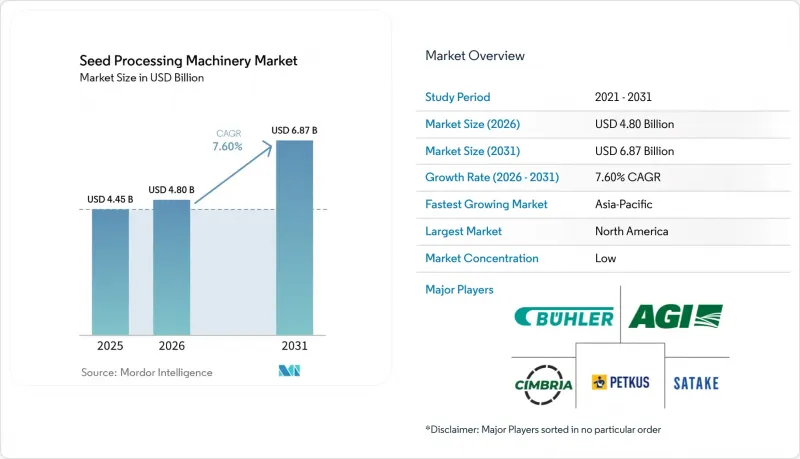

According to Mordor Intelligence, the seed processing machinery market size was valued at USD 4.45 billion in 2025 and is projected to grow from USD 4.80 billion in 2026 to USD 6.87 billion by 2031, registering a 7.6% CAGR from 2026 to 2031.

This report is Segmented by Machinery Type (Pre-Cleaners, Cleaners, Dryers, Graders, Polishers, Optical Sorters, Seed Packagers, and More), by Operation Mode (Automatic and Semi-Automatic), by End-User (Commercial Seed Processing Plants, Seed Producers, On-Farm Facilities, and More), and by Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Seed Processing Machinery Market Trends and Insights

Automation of Optical Sorting Enhances Efficiency and Reduces Labor Costs

Automation is enhancing performance standards in the seed processing machinery market by minimizing manual intervention in sorting and defect removal processes. Artificial intelligence-enabled optical systems can identify variations in color, texture, and shape at the single-seed level, enabling processors to improve purity without compromising line speed. The launch of Buhler's SORTEX AI700 in 2025 exemplifies the transition toward deep-learning sorting systems aimed at improving inspection quality in seed and grain applications. As the market shifts from multiple mechanical stages to fewer intelligent sorting units, each line achieves higher productivity but also faces increased vulnerability to unplanned stoppages. This development underscores the growing importance of predictive maintenance, remote diagnostics, and robust service contracts in commercial procurement within the seed processing machinery market.

Increasing Demand for Treated and Value-Added Seeds

The seed processing machinery market is experiencing growth driven by advancements beyond basic fungicide treatments, including bioactive inoculants, micronutrient coatings, and specialized polymer films. These high-value seed products necessitate precise coating consistency, improved drying control, and enhanced lot segregation, as inconsistencies in application quality can compromise the performance of an entire certified batch. In October 2024, India's National Mission on Edible Oils and Oilseeds allocated INR 10,103 crore (USD 1.19 billion) and established 65 new seed hubs, generating direct downstream demand for equipment used in treating, coating, and packaging seeds. Additionally, the market is witnessing increased demand for ancillary equipment, such as cleaners, packagers, and labeling systems, to maintain lot integrity throughout the processing chain. The rise of biological treatments has further driven equipment demand, as processors require low-shear and temperature-controlled coating and drying systems to ensure the viability of microorganisms.

High Up-Front Cost of Smart Machinery

High initial costs remain a significant barrier to the adoption of advanced seed processing machinery. Buyers often compare the costs of advanced optical sorting systems with conventional mechanical equipment, finding optical sorters to be 40% to 60% more expensive. Additionally, expenses related to automation controls, connectivity infrastructure, and supervisory control and data acquisition systems further increase the overall project investment. These financial challenges are particularly pronounced in regions with limited access to agricultural financing and long equipment replacement cycles. Consequently, the high capital investment required continues to hinder the adoption of advanced seed processing machinery by cooperatives, farm-level processors, and small to medium-scale commercial operators.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies Boost Post-Harvest Mechanization Efforts

- Growth in Commercial Seed Multiplication Centers

- Supply Chain Volatility for Precision Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The seed processing machinery market share for the cleaners segment accounted for the largest 42.7% in 2025. Cleaners continue to dominate as primary seed cleaning is essential before subsequent operations, such as grading, treatment, drying, coating, and packaging, can commence. Air-screen cleaners are widely preferred due to their scalability, low maintenance requirements, and compatibility with various crop types and downstream equipment systems. Additionally, dryers and treatment systems are gaining significance in regions addressing post-harvest moisture management challenges and the increasing adoption of biological seed treatments. The cleaners segment benefits from sustained demand across commercial seed plants, grain handlers, and integrated seed-processing facilities managing large multi-crop processing workflows globally.

The seed processing machinery market for the optical sorters segment will advance to grow at the fastest CAGR of 7.6% from 2026 to 2031. This growth is driven by rising demand for export-grade seed purity, digital quality control, and automated defect detection technologies. Optical sorters are increasingly utilized as artificial intelligence-enabled imaging systems enhance processing precision and minimize contamination risks in high-value seed operations. Manufacturers are also incorporating compliance monitoring, traceability, and data-management features into sorting platforms to meet certification requirements. Despite the rapid growth of advanced sorting systems, cleaners remain the dominant equipment category, as primary seed-cleaning processes continue to serve as the operational foundation for commercial seed-processing workflows globally.

Geography Analysis

The sedd processing machinery market share for North America accounted for the largest 34.1% in 2025. The region benefits from a well-established commercial seed industry, widespread adoption of precision seed-treatment technologies, and extensive row-crop production systems. The large-scale cultivation of corn and soybeans drives strong demand for advanced seed-cleaning, grading, and optical-sorting systems. Commercial seed companies in the United States and Canada are increasingly investing in integrated processing infrastructure to enhance traceability, meet purity standards, and ensure export compliance. Factors such as strong replacement demand, digital process integration, and established seed-certification systems continue to reinforce North America's leading position in commercial seed-processing equipment and infrastructure development globally.

The sedd processing machinery market size for Asia-Pacific is projected to grow at the fastest 8.1% CAGR from 2026 to 2031. This growth is driven by the expansion of certified seeds, government-supported agricultural modernization initiatives, and increasing investments in commercial processing infrastructure across China, India, and Southeast Asia. Public funding for seed hubs, processing units, and grain-handling infrastructure is accelerating the adoption of modern cleaning, drying, and sorting systems throughout the region. Additionally, the rise of commercial agriculture and growing demand for high-quality certified seeds are fostering the modernization of processing operations. More developed agricultural economies, such as Japan, Australia, and South Korea, are focusing on optical sorting, digital compliance systems, and automated processing technologies within their commercial seed-production networks.

South America remains a significant growth region due to the extensive cereal and oilseed seed multiplication activities in Brazil and Argentina, which are closely tied to export-oriented agriculture. According to the Food and Agriculture Organization of the United Nations, Ethiopia's Postharvest Management Strategy 2024-2030 has allocated ETB 14.3 billion (USD 266 million) for post-harvest mechanization and processing technology deployment. This initiative supports the broader modernization of seed and grain infrastructure. In the Middle East and Africa, there is a growing focus on food security, controlled-environment agriculture, and improvements in post-harvest efficiency. These developments are gradually driving demand for modern seed-cleaning, sorting, and handling technologies in developing agricultural economies.

- Buhler AG

- Cimbria A/S (Grain & Protein Technologies)

- PETKUS Technologie GmbH

- Satake Corporation

- Ag Growth International Inc.

- Westrup ApS (Fowler Westrup India Pvt. Ltd.)

- Alvan Blanch Development Company Limited

- Osaw Agro Industries Pvt. Ltd.

- Skiold A/S

- Oliver Manufacturing CO, Inc.

- Shijiazhuang Synmec International Trading, Ltd. (Hebei Ruixue Grain Selecting Machinery Co., Ltd.)

- Carter Day International, Inc.

- Lewis M. Carter Manufacturing, LLC

- Bratney Companies (K.B.C. Group, Inc.)

- Spectrum Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automation of optical sorting enhances efficiency and reduces labor costs

- 4.2.2 Increasing demand for treated and value-added seeds

- 4.2.3 Government subsidies boost post-harvest mechanization efforts

- 4.2.4 Growth in commercial seed multiplication centers

- 4.2.5 Microplastic-free coating transition drives treater and dryer retrofits

- 4.2.6 Digital traceability and certification workflows drive inline sampling and labeling upgrades

- 4.3 Market Restraints

- 4.3.1 High up-front cost of smart machinery

- 4.3.2 Supply chain volatility for precision components

- 4.3.3 Operator and service-skill bottlenecks limit uptime

- 4.3.4 Data ownership and cyber security concerns around connected equipment

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Machinery Type

- 5.1.1 Pre-cleaners

- 5.1.2 Cleaners

- 5.1.3 Dryers

- 5.1.4 Graders

- 5.1.5 Coaters and Treaters

- 5.1.6 Separators and Destoners

- 5.1.7 Polishers

- 5.1.8 Optical Sorters

- 5.1.9 Seed Packagers

- 5.1.10 Other Specialized Equipment

- 5.2 By Operation Mode

- 5.2.1 Automatic

- 5.2.2 Semi-Automatic

- 5.3 By End-User

- 5.3.1 Commercial Seed Processing Plants

- 5.3.2 Seed Producers

- 5.3.3 Research Institutions

- 5.3.4 On-Farm Facilities

- 5.3.5 Grain Handling Facilities

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 Italy

- 5.4.2.4 Spain

- 5.4.2.5 United Kingdom

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Buhler AG

- 6.4.2 Cimbria A/S (Grain & Protein Technologies)

- 6.4.3 PETKUS Technologie GmbH

- 6.4.4 Satake Corporation

- 6.4.5 Ag Growth International Inc.

- 6.4.6 Westrup ApS (Fowler Westrup India Pvt. Ltd.)

- 6.4.7 Alvan Blanch Development Company Limited

- 6.4.8 Osaw Agro Industries Pvt. Ltd.

- 6.4.9 Skiold A/S

- 6.4.10 Oliver Manufacturing CO, Inc.

- 6.4.11 Shijiazhuang Synmec International Trading, Ltd. (Hebei Ruixue Grain Selecting Machinery Co., Ltd.)

- 6.4.12 Carter Day International, Inc.

- 6.4.13 Lewis M. Carter Manufacturing, LLC

- 6.4.14 Bratney Companies (K.B.C. Group, Inc.)

- 6.4.15 Spectrum Industries

7 Market Opportunities and Future Outlook