PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066531

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066531

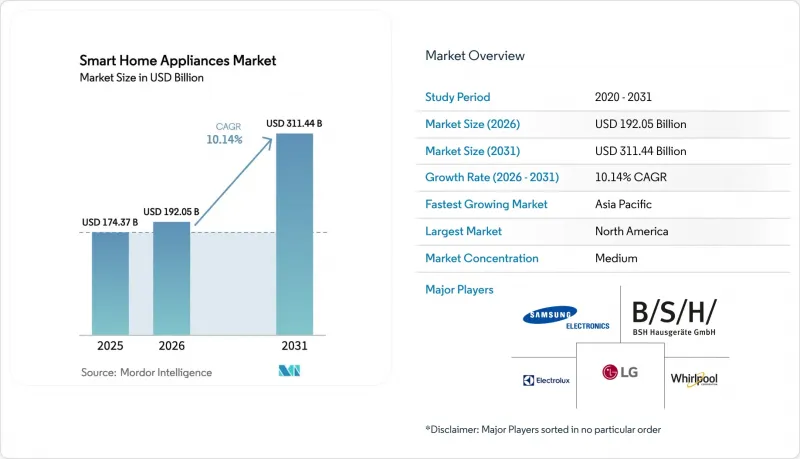

Smart Home Appliances - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the smart home appliances market size is projected to be USD 174.37 billion in 2025, USD 192.05 billion in 2026, and reach USD 311.44 billion by 2031, growing at a CAGR of 10.14% from 2026 to 2031.

This report is Segmented by Product Type (Smart Refrigerators, Smart Ovens, Smart Dishwashers, and More), Connectivity Technology (Wi-Fi, Bluetooth, Zigbee, Z-Wave, Thread, Other Technologies), Distribution Channel (Online, Offline), End-User Industry (Residential, Commercial), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Smart Home Appliances Market Trends and Insights

Rapid Adoption of IoT and Voice-Assistant Ecosystems

Samsung's SmartThings platform logged 2.5 billion device interactions during 2024, while Amazon Alexa now supports 140,000 smart devices across 400 brands . This critical mass removes the learning-curve barrier that long deterred older homeowners. Appliance makers are embedding Thread 1.4 radios so products can self-organize into secure mesh networks that maintain service even if the household Wi-Fi router fails . Integration also yields compound use-cases like dryers coordinate with rooftop solar output, or refrigerators vary compressor speed in line with occupancy patterns collected by home security sensors. The result is an ecosystem in which connected appliances deliver measurable electricity savings without constant user input, broadening the smart home appliances market to previously hesitant demographics.

Energy-Efficiency Regulations and Incentive Programs

Mandatory efficiency labels are morphing into connectivity mandates. The EU's 2025 energy-labeling update requires that A-rated refrigerators and washers include smart-grid interfaces. California's Title 24 building code similarly obliges new homes to install demand-response-ready appliances. Complementary rebates amplify pull-through demand. For instance, ComEd pays USD 50-200 per unit for qualified devices enrolled in its Peak-Time Savings program. These carrots and sticks mean manufacturers that cannot demonstrate secure two-way communication risk losing shelf space at big-box retailers. Such policies move the smart home appliances market beyond voluntary adoption toward regulatory compliance, elongating replacement cycles as buyers trade up to maintain resale value.

Data-Privacy and Cybersecurity Concerns

The 2024 Wyze camera breach, which exposed 13,000 video feeds, placed privacy squarely on mainstream news cycles and curbed intent-to-buy scores for connected devices. New rules under the EU Cyber Resilience Act compel vendors to provide security patches for a product's entire service life, raising lifetime support costs. Similar proposals in the United States would require factory-installed unique passwords and public vulnerability disclosures. Consumers interpreting headlines equate any internet-connected appliance with risk, raising the bar for transparent data-use policies. Brands must now allocate budget for encryption hardware and third-party penetration testing, which marginally inflates retail pricing and slows adoption in the smart home appliances market.

Other drivers and restraints analyzed in the detailed report include:

- Growth of E-Commerce Home-Appliance Sales

- Utilities' Time-of-Use Tariffs Driving Smart Load-Shifting Appliances

- Supply-Chain Volatility for Semiconductor Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart washing machines and dryers commanded 24.12% of the smart home appliances market share in 2025, a leadership driven by short replacement cycles and rebate-boosted ROI calculations. High-spin motors and sensor-based detergent dosing save water and electricity, validating purchase decisions for cost-conscious families. Conversational voice controls and mobile push alerts further reduce user effort, lifting customer-satisfaction scores. Smart refrigerators leverage their always-powered status to anchor digital dashboards, becoming central hubs for grocery management and home-energy analytics. Ovens are iterating toward camera-enabled bake detection and auto-shutoff logic that cuts food waste and electricity bills.

Smart cookware and cooktops, while starting from a smaller base, are projected to grow at a 12.74% CAGR through 2031, the fastest among product categories. AI-linked recipe libraries and precision induction zones cater to time-starved professionals seeking guaranteed results. Autonomous vacuum cleaners and air conditioners capitalize on labor-saving appeal and comfort optimization, respectively, thereby recruiting first-time smart appliance buyers. Dishwashers and kitchen scales add incremental connectivity that extends ecosystem stickiness without inflating prices excessively. Overall, appliances that incorporate hands-free autonomy or measurable cost savings continue to outpace features that merely replicate manual controls, reinforcing hierarchy within the smart home appliances market.

Wi-Fi accounted for 57.93% of 2025 revenue owing to near-universal router penetration and user familiarity. Yet Thread devices are forecast to expand at a 12.94% CAGR as Matter certification gains prominence. Thread-enabled appliances form self-healing IPv6 meshes that sustain low-latency performance even when single nodes drop offline, satisfying the stringent reliability needs of ovens or HVAC systems. This evolution diminishes proprietary hubs, lowering total system cost for homeowners. Bluetooth retains a foothold for personal-health products like smart scales, where occasional phone sync suffices. Zigbee and Z-Wave continue serving security-plus-lighting bundles sold through professional installers.

Vendors now view open, certificate-based provisioning as a safeguard against future cybersecurity mandates. Accordingly, engineering roadmaps prioritize Thread radios, sometimes in dual-band packages that support Wi-Fi 6 for over-the-air firmware updates while defaulting to Thread for day-to-day telemetry. Such architectural shifts position Thread as the baseline for the next hardware replacement wave, further standardizing the smart home appliances market around interoperable protocols.

Geography Analysis

North America led with 32.41% revenue share in 2025, anchored by mature rebate infrastructures and high disposable income. ComEd's Peak-Time Savings and PG&E's Critical-Peak Pricing reward connected load shifting, ensuring tangible financial returns. Federal efficiency standards now incorporate connected-ready provisions, effectively making smart features table stakes for new models. Canada's federal carbon price credits further nudge consumers toward AI-managed machines, while Mexico's rising middle class is fueling demand in urban centers despite patchy rural broadband coverage.

Asia Pacific is projected to compound at an 11.12% CAGR through 2031, making it the fastest-growing region. China shipped 4.48 billion appliances in 2024, up 20.8% year-on-year, and domestic giants Midea and Haier are using scale advantages to undercut Western peers abroad. South Korea and Japan, already boasting fiber penetration rates above 97%, are early adopters of premium AI fridge-to-car charging synchronization. India's smart-city initiatives include subsidies for grid-interactive devices, smoothing price sensitivities. Southeast Asia's booming e-commerce platforms are bypassing retail infrastructure gaps, accelerating device availability even in secondary cities.

Europe maintains a steady trajectory as stringent regulations shift from efficiency to cybersecurity. The updated energy label requires smart-grid interfaces by 2025, while the Cyber Resilience Act mandates lifetime patch delivery. Germany and the UK leverage ample rooftop solar to encourage appliances that modulate consumption based on intra-day prices. Nordic countries, with abundant hydro and wind resources, encourage load-shifting washers and dryers that flatten demand curves during winter peaks. In the Middle East and Africa, adoption remains concentrated in wealthier Gulf Cooperation Council states, but new fiber corridors and urban megaprojects are creating beachheads for future expansion, gradually enlarging the global smart home appliances market.

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Whirlpool Corporation

- AB Electrolux

- BSH Hausgerate GmbH

- Haier Smart Home Co., Ltd.

- Panasonic Corporation

- Midea Group Co., Ltd.

- Xiaomi Corporation

- GE Appliances (Haier Company)

- Arcelik A.S.

- Breville Group Limited

- Dyson Ltd.

- Gorenje Group

- Miele & Cie. KG

- Daewoo Electronics Corp.

- Hisense Home Appliances Group

- Sharp Corporation

- Vestel Elektronik AS

- Smeg S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising disposable income and consumer awareness

- 4.2.2 Rapid adoption of IoT and voice-assistant ecosystems

- 4.2.3 Energy-efficiency regulations and incentive programs

- 4.2.4 Growth of e-commerce home-appliance sales

- 4.2.5 OEM bundling of AI-based predictive-maintenance services

- 4.2.6 Utilities' time-of-use tariffs driving smart load-shifting appliances

- 4.3 Market Restraints

- 4.3.1 High upfront cost and long replacement cycles

- 4.3.2 Data-privacy and cybersecurity concerns

- 4.3.3 Fragmented connectivity standards limiting interoperability

- 4.3.4 Supply-chain volatility for semiconductor components

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Smart Refrigerators

- 5.1.2 Smart Ovens

- 5.1.3 Smart Dishwashers

- 5.1.4 Smart Washing Machines and Dryers

- 5.1.5 Smart Cookware and Cooktops

- 5.1.6 Smart Vacuum Cleaners

- 5.1.7 Smart Air Conditioners

- 5.1.8 Smart Scales and Thermometers

- 5.1.9 Other Product Types

- 5.2 By Connectivity Technology

- 5.2.1 Wi-Fi

- 5.2.2 Bluetooth

- 5.2.3 Zigbee

- 5.2.4 Z-Wave

- 5.2.5 Thread

- 5.2.6 Other Technologies

- 5.3 By Distribution Channel

- 5.3.1 Online

- 5.3.2 Offline

- 5.4 By End-User Industry

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Southeast Asia

- 5.5.4.7 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 LG Electronics Inc.

- 6.4.3 Whirlpool Corporation

- 6.4.4 AB Electrolux

- 6.4.5 BSH Hausgerate GmbH

- 6.4.6 Haier Smart Home Co., Ltd.

- 6.4.7 Panasonic Corporation

- 6.4.8 Midea Group Co., Ltd.

- 6.4.9 Xiaomi Corporation

- 6.4.10 GE Appliances (Haier Company)

- 6.4.11 Arcelik A.S.

- 6.4.12 Breville Group Limited

- 6.4.13 Dyson Ltd.

- 6.4.14 Gorenje Group

- 6.4.15 Miele & Cie. KG

- 6.4.16 Daewoo Electronics Corp.

- 6.4.17 Hisense Home Appliances Group

- 6.4.18 Sharp Corporation

- 6.4.19 Vestel Elektronik AS

- 6.4.20 Smeg S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment