PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066541

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066541

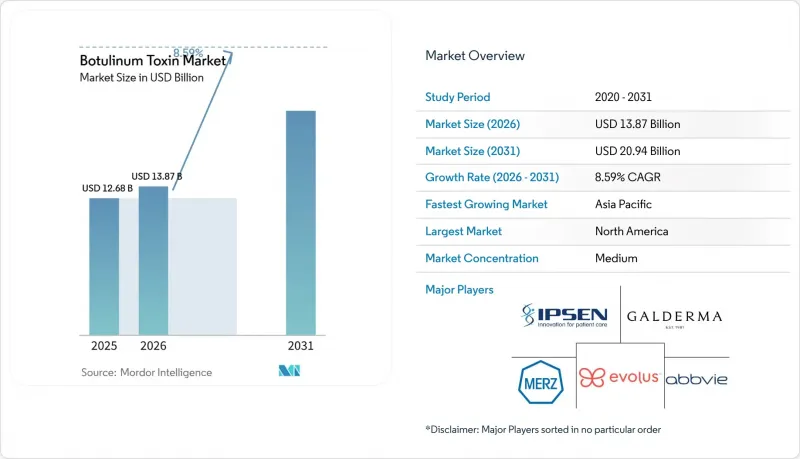

Botulinum Toxin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the botulinum toxin market size is projected to expand from USD 12.68 billion in 2025 and USD 13.87 billion in 2026 to USD 20.94 billion by 2031, registering a CAGR of 8.59% between 2026 to 2031.

This report Segments the Industry Into by Product Type (Botulinum Toxin Type A, Botulinum Toxin Type B), Application (Aesthetic, Therapeutic), End User (Specialty & Dermatology Clinics, Hospitals & Surgery Centers, Spas & Beauty Centers, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Botulinum Toxin Market Trends and Insights

Rising Demand for Minimally Invasive Aesthetic Procedures

Global procedure counts continue to climb because neuromodulators offer immediate, reversible results without surgical downtime, qualities highly valued in social-media-driven cultures. The American Society of Plastic Surgeons recorded 9.88 million U.S. neuromodulator sessions in 2024, a 4% year-over-year uptick that masks even steeper growth among first-time male users and patients under 30. Instagram and TikTok compress consideration windows, pushing patients from awareness to treatment in under 18 months. Clinics that can schedule same-day consults capture these impulse conversions and report a 3.2-visit annual cadence per patient, sustaining recurring revenue. The "tweakment" culture favors subtle, repeat interventions rather than dramatic facelifts, which in turn stabilizes volume even when macroeconomic conditions soften and reinforces botulinum toxin market growth. Yet the surge also invites non-physician injectors where regulation is light, prompting quality concerns that authorities are beginning to police.

Growing Adoption in Chronic Migraine Prophylaxis

Chronic migraine affects roughly 2% of the population; onabotulinumtoxinA now holds first-line status under 2024 American Headache Society guidelines, supported by Level A evidence from multi-year trials. UnitedHealthcare removed prior-authorization requirements in 2025, resulting in a 34% reduction in dropout rates within six months. Health-economic analyses show that emergency department visits decrease by 47% and opioid prescriptions by 52% once patients initiate toxin prophylaxis, resulting in an annual net savings of USD 4,200 per case. Neurologists are increasingly administering injections in-office, thereby broadening the treatment base. As accountable-care organizations shoulder downside risk, botulinum toxin fits neatly into value-based care models, accelerating its therapeutic adoption.

Immunoresistance & Neutralizing Antibody Risk

Neutralizing antibodies arise in 1-3% of repeat users, typically after seven cycles or cumulative doses exceeding 200 units, which can lead to treatment failure and necessitate product switching. Comparative data on protein-free versus conventional toxins remain sparse, leaving clinicians reliant on pragmatic dosing strategies and wider inter-treatment intervals. Payers watching real-world effectiveness may introduce antibody testing, adding cost and administrative steps that could dampen uptake, especially in aesthetic settings where patients pay out-of-pocket.

Other drivers and restraints analyzed in the detailed report include:

- Expansion in APAC Via Indigenous Manufacturers

- Longer-Lasting, Complexing-Protein-Free Formulations

- Cold-Chain & Handling Gaps in Low-Income Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The botulinum toxin market size for Type A products accounted for 87.81% of total revenue in 2025, reflecting their broad FDA labeling across both aesthetic and therapeutic domains. Complex-protein-free formulations, such as Xeomin, are gradually eroding legacy share because the single-session upper-face indication, cleared in 2024, reduces chair time and appeals to volume-driven clinics. Jeuveau increased its U.S. market share from 4% in 2019 to 14% in 2025 by targeting millennials with social media-centric campaigns at prices 20-30% lower than the market leader. Daxxify's six-month duration differentiator has not yet translated into proportional uptake because provider training requirements slow onboarding. Korean entrants with 30-40% lower pricing continue gaining traction in Asia and parts of Latin America, further shaping botulinum toxin market share.

Type B's contribution is small yet rising at a 10.58% CAGR through 2031 as antibody-induced non-responders to Type A accumulate. RimabotulinumtoxinB offers a 24- to 48-hour onset, making it appealing for acute cervical dystonia cases. Eisai logged 19% European revenue growth in 2024, driven by neurologist switches rather than new-to-therapy patients. Duration is shorter, but where functional improvement outweighs cosmetic longevity, clinicians are willing to trade repeat visits for efficacy. The result is a stable, if niche, revenue driver that diversifies the botulinum toxin industry portfolio.

Geography Analysis

North America accounted for 42.36% of global revenue in 2025 and remains the leading market for new product launches and regulatory precedents. U.S. volume reached 9.88 million procedures in 2024, concentrated in coastal metros for aesthetic purposes and dispersed across neurology and urology practices for therapeutic use. Health Canada's 2024 approval of Nabota injects pricing competition that may expand access among cost-sensitive consumers. Mexico's medical-tourism flow offers 50-60% cost savings but faces counterfeit risk, curbing its scale. The FDA's openness to novel serotypes, exemplified by TrenibotE's 2025 BLA, signals ongoing innovation, although distant-spread safety communications raise concerns about malpractice insurance.

The Asia-Pacific region is forecast to grow at a 12.13% CAGR, the fastest worldwide, driven by domestic manufacturing scale and an expanding middle class. South Korea's per-capita usage rivals that of the U.S., driven by cultural acceptance and government export incentives. China's market divides along quality perceptions: tier-1 cities prefer Western labels, whereas tier-2 and tier-3 cities opt for domestic products priced at USD 80-100 per vial. Japan's aging population pushes therapeutic demand; Xeomin only secured PMDA clearance in 2024, but uptake is accelerating. India's aesthetic segment grows at a rate of 20-25% annually in urban centers, yet cold-chain gaps constrain its broader penetration. Southeast Asian hubs, such as Bangkok, treat approximately 120,000 international aesthetic patients annually at 40% discounts, thereby extending the regional reach of the botulinum toxin market.

Europe holds a mid-tier share, with growth tempered by the European Medicines Agency's 2025 mandate for enhanced distant-spread warnings, which lengthen sales cycles in France and Italy. Germany and the UK lead therapeutic uptake through national health coverage for chronic migraine and spasticity; the UK's nurse-led OAB clinics have reduced wait times from nine months to six weeks. Eastern European countries are catching up as incomes rise and Western-trained physicians return to their homeland. In the Middle East, the UAE and Saudi Arabia drive growth, leveraging their high per-capita wealth and medical tourism infrastructure. South Africa exhibits steady private-sector growth, but wider sub-Saharan penetration is limited by infrastructure and public health priorities. South America pivots on Brazil, where ANVISA reviews Korean and Chinese toxins, potentially democratizing access once approvals land.

- Abbvie

- Aesthetic Biomedical Inc.

- Coretox (Medytox subsidiary)

- Daewoong Pharmaceutical Co., Ltd.

- Eisai

- Evolus Inc.

- Galderma

- Huons Global

- Hugel Inc.

- Ipsen Group

- Lanzhou Institute of Biological Products Co., Ltd.

- Medytox

- Merz Pharma

- Revance Therapeutics

- Shanghai Haohai Biological Technology Co., Ltd.

- Sihuan Pharmaceutical Holdings Ltd.

- Stemline Therapeutics

- Syndax Pharmaceuticals

- Suneva Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Minimally-Invasive Aesthetic Procedures

- 4.2.2 Growing Adoption in Chronic Migraine Prophylaxis

- 4.2.3 Expansion in APAC Via Indigenous Manufacturers

- 4.2.4 Longer-Lasting, Complexing-Protein-Free Formulations

- 4.2.5 Rising Male and "Pre-Juvenation" Patient Segments

- 4.2.6 Reimbursement Gains for Neurogenic Bladder & OAB

- 4.3 Market Restraints

- 4.3.1 Immunoresistance & Neutralizing Antibody Risk

- 4.3.2 Cold-Chain & Handling Gaps in Low-Income Markets

- 4.3.3 Counterfeit / Grey-Market Toxin Supply

- 4.3.4 High Out-of-Pocket Costs for Cosmetic Indications

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Botulinum Toxin Type A

- 5.1.1.1 OnabotulinumtoxinA (Botox)

- 5.1.1.2 AbobotulinumtoxinA (Dysport)

- 5.1.1.3 IncobotulinumtoxinA (Xeomin)

- 5.1.1.4 PrabotulinumtoxinA (Jeuveau)

- 5.1.1.5 DaxibotulinumtoxinA (Daxxify)

- 5.1.1.6 Complexing-protein-free (Coretox & others)

- 5.1.2 Botulinum Toxin Type B

- 5.1.1 Botulinum Toxin Type A

- 5.2 By Application

- 5.2.1 Aesthetic

- 5.2.1.1 Glabellar Lines

- 5.2.1.2 Crow's Feet

- 5.2.1.3 Forehead Lines

- 5.2.1.4 Masseter Reduction & Jaw Contouring

- 5.2.1.5 Body Contouring & Hyperhidrosis

- 5.2.2 Therapeutic

- 5.2.2.1 Chronic Migraine

- 5.2.2.2 Spasticity

- 5.2.2.3 Cervical Dystonia

- 5.2.2.4 Neurogenic Detrusor Overactivity / OAB

- 5.2.2.5 Sialorrhea

- 5.2.2.6 Others (Strabismus, Tremor, TMD)

- 5.2.1 Aesthetic

- 5.3 By End User

- 5.3.1 Specialty & Dermatology Clinics

- 5.3.2 Hospitals & Surgery Centers

- 5.3.3 Spas & Beauty Centers

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc. (Allergan Aesthetics)

- 6.3.2 Aesthetic Biomedical Inc.

- 6.3.3 Coretox (Medytox subsidiary)

- 6.3.4 Daewoong Pharmaceutical Co., Ltd.

- 6.3.5 Eisai Co., Ltd.

- 6.3.6 Evolus Inc.

- 6.3.7 Galderma S.A.

- 6.3.8 Huons Global

- 6.3.9 Hugel Inc.

- 6.3.10 Ipsen Group

- 6.3.11 Lanzhou Institute of Biological Products Co., Ltd.

- 6.3.12 Medytox Inc.

- 6.3.13 Merz Pharma GmbH & Co. KGaA

- 6.3.14 Revance Therapeutics Inc.

- 6.3.15 Shanghai Haohai Biological Technology Co., Ltd.

- 6.3.16 Sihuan Pharmaceutical Holdings Ltd.

- 6.3.17 Stemline Therapeutics

- 6.3.18 Syndax Pharmaceuticals

- 6.3.19 Suneva Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment