PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066542

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066542

Insurance Fraud Detection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

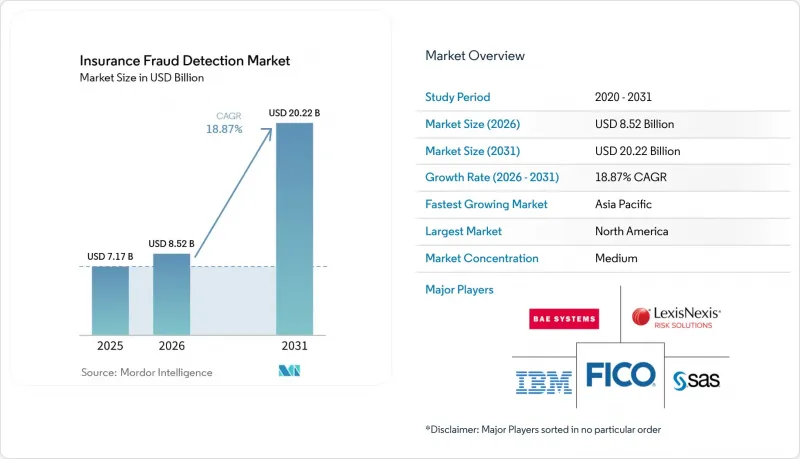

According to Mordor Intelligence, the insurance fraud detection market size is projected to be USD 7.17 billion in 2025, USD 8.52 billion in 2026, and reach USD 20.22 billion by 2031, growing at a CAGR of 18.87% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (On-Premise, Cloud-Based, Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Identity Theft Detection, Payment and Billing Fraud, and More), End User (Life Insurance, Health Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Insurance Fraud Detection Market Trends and Insights

Expanding Volume of Digital Claims Data

Insurers processed more than 1.2 billion mobile-first claims in 2025, overwhelming batch-oriented fraud engines that rely on static business rules. Photo, video, and geolocation files require computer vision and natural language models that can triage unstructured inputs in seconds. Early adopters reported 30% fewer false positives after deploying multimodal analytics, which freed investigators to focus on high-severity alerts. The volume of incoming evidence also increases consent-management complexity, as customers may withdraw permission to use personal images at any time under privacy statutes. Vendors that offer elastic cloud storage combined with secure edge preprocessing are attracting carriers that need to keep pace with nonstop claim uploads, strengthening growth in the insurance fraud detection market.

Growing Adoption of Predictive Analytics and AI

Machine-learning deployment reached 62% of global insurers in 2025, up from 41% a year earlier, as carriers sought real-time fraud scores at the point of quote, accelerating innovation across the insurance fraud detection market. Platforms now fuse telematics, credit, and social-media data to identify suspicious behavior before policies bind. Deloitte projects that widespread adoption of artificial intelligence could save the sector USD 80 billion to USD 160 billion by 2032. Regulators are pushing for transparent models, prompting a wave of investments in explainability dashboards and bias audits that document every input feature. Vendors that balance high detection lift with granular traceability are winning multi-year enterprise contracts in North America and Western Europe.

Data Privacy and Consent Constraints

The European Union General Data Protection Regulation and California Consumer Privacy Act require explicit opt-ins before personal data can feed fraud models, shrinking usable datasets whenever policyholders refuse consent. India's Digital Personal Data Protection Act allows claimants to demand human review of automated decisions, adding to the already-stressed workload of investigation teams. Multinational insurers must now design region-specific workflows that comply with the strictest standards, inflating project timelines and legal costs. Smaller carriers without in-house counsel incur higher per-policy compliance expenses, which slow the adoption of cloud-based analytics. Vendors offering granular consent management and automated deletion routines gain a competitive edge.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Regulatory Pressure to Reduce Fraud Losses

- Proliferation of Real-Time Data Sources

- Integration Complexity with Legacy Core Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 63.44% of component revenue in 2025, yet services are expanding at a 19.07% CAGR, which will lift their share of the insurance fraud detection market through 2031. The surge reflects mounting needs for bias audits, model retraining, and regulator-ready documentation that many carriers prefer to outsource rather than build internally. Services vendors now bundle implementation consulting with recurring managed-detection subscriptions, converting one-time license buyers into long-lived revenue streams. As insurance fraud detection market share for services rises, software providers respond by embedding audit trails and fairness dashboards directly into core platforms to defend against account stickiness.

The shift favors consultancies that maintain expertise across multiple governance regimes, including the National Association of Insurance Commissioners bulletin in the United States and the European Union Artificial Intelligence Act. They deliver risk-based pricing that aligns monthly fees with recovered fraud savings, an approach that resonates with finance teams under margin pressure. Oracle, SAP, and IBM have launched service-heavy subscription tiers that couple platform access with continuous monitoring, shortening procurement cycles for midsize carriers that lack in-house data scientists. Over the forecast horizon, demand for evidence-ready compliance artifacts will keep service growth ahead of software growth, even as low-code tools reduce initial deployment effort.

Cloud implementations captured 58.46% revenue in 2025, but hybrid deployments clock the fastest 19.34% CAGR, positioning them to gain insurance fraud detection market share before 2031. Hybrid lets carriers process sensitive claims data on-premise while sending tokenized features to cloud models, an architecture that satisfies data-sovereignty rules in jurisdictions such as Germany and Japan. Confidential-computing enclaves on Microsoft Azure and similar platforms encrypt data in use, making hybrid environments palatable to risk-averse compliance teams. Edge gateways further cut latency by compressing images and extracting fraud-relevant features close to the data source, ensuring real-time scoring even when wide-area bandwidth is thin.

Complexity persists because model versions in the cloud must remain synchronized with on-premises rule engines to avoid scoring drift. Vendors offer unified orchestration layers that automate rollout and rollback across tiers, enabling insurers to adopt agile release cycles without breaching audit controls. Sovereign-cloud investments from regional hyperscalers lower jurisdictional barriers and bring additional compute choices to conservative markets. As a result, the insurance fraud detection market size tied to hybrid projects will continue to accelerate, especially among national carriers that run mixed mainframe and microservice estates.

Geography Analysis

North America retained 39.62% of the insurance fraud detection market share in 2025, underscoring its status as the largest regional buyer of advanced analytics platforms. Regulatory catalysts, such as the National Association of Insurance Commissioners bulletin and Colorado's Artificial Intelligence Act, require carriers to conduct annual fairness audits, pushing technology budgets toward the development of explainability dashboards. United States carriers balance proprietary builds with software-as-a-service subscriptions, while Canada's patchwork of provincial rules complicates cross-border platform rollouts and lengthens implementation cycles. Mexico's low insurance penetration limits spend, yet cross-border auto-fraud pressures drive adoption of telematics-enabled verification tools that validate accident locations.

Asia-Pacific posts the fastest regional CAGR of 19.89%, positioning it to drive the insurance fraud detection market to a larger size than any other geography through 2031. India's mandate requiring every insurer to deploy an integrated fraud-monitoring framework by April 2026 is unlocking hundreds of millions of dollars in new investments. China's digital insurers formed a big-data alliance in 2025 that shares anonymized patterns, trimming duplicate investigations and accelerating blocklist updates. Japan is migrating from manual audits to anomaly scoring after a 2025 investigation uncovered systemic life-insurance misrepresentation, prompting carriers to integrate third-party validation feeds. South Korea's 15-day fraud-reporting deadline and Hong Kong's regulatory cohort programs round out a regionwide push toward real-time analytics.

Europe, the Middle East and Africa, and South America contribute smaller but steadily rising slices of global demand. The European Union Artificial Intelligence Act classifies fraud detection as a high-risk category, compelling conformity assessments that favor vendors with built-in audit trails. United Kingdom guidance on discriminatory outcomes widens spending on bias mitigation, while Germany's data-sovereignty rules keep many deployments on private cloud. The United Arab Emirates encourages pilot projects but lacks uniform privacy codes, leading insurers to adopt modular platforms they can localize quickly. Brazil's guidance linking product approvals to fraud-prevention capabilities nudges carriers toward modern tools, though overall spend remains capped by low insurance density and macroeconomic volatility.

- SAS Institute Inc.

- IBM Corporation

- Fair Isaac Corporation

- BAE Systems plc

- LexisNexis Risk Solutions

- Shift Technology

- Friss Fraudebestrijding B.V.

- Experian plc

- ACI Worldwide Inc.

- Verisk Analytics Inc.

- Optalitix Ltd.

- KPMG International Ltd.

- Accenture plc

- Oracle Corporation

- SAP SE

- Pegasystems Inc.

- DataRobot Inc.

- Microsoft Corporation

- Hewlett Packard Enterprise Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Volume of Digital Claims Data

- 4.2.2 Growing Adoption of Predictive Analytics and AI

- 4.2.3 Increasing Regulatory Pressure to Reduce Fraud Losses

- 4.2.4 Rising Sophistication of Organized Fraud Rings

- 4.2.5 Proliferation of Real-Time Data Sources (Telematics, IoT)

- 4.2.6 Emergence of On-Demand Insurance Models

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Consent Constraints

- 4.3.2 Integration Complexity with Legacy Core Systems

- 4.3.3 High Cost of Skilled Data Science Talent

- 4.3.4 Bias and Fairness Concerns in AI Models

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud-Based

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Claims Fraud Detection

- 5.4.2 Underwriting Fraud

- 5.4.3 Identity Theft Detection

- 5.4.4 Payment and Billing Fraud

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Property and Casualty Insurance

- 5.5.2 Life Insurance

- 5.5.3 Health Insurance

- 5.5.4 Other End Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAS Institute Inc.

- 6.4.2 IBM Corporation

- 6.4.3 Fair Isaac Corporation

- 6.4.4 BAE Systems plc

- 6.4.5 LexisNexis Risk Solutions

- 6.4.6 Shift Technology

- 6.4.7 Friss Fraudebestrijding B.V.

- 6.4.8 Experian plc

- 6.4.9 ACI Worldwide Inc.

- 6.4.10 Verisk Analytics Inc.

- 6.4.11 Optalitix Ltd.

- 6.4.12 KPMG International Ltd.

- 6.4.13 Accenture plc

- 6.4.14 Oracle Corporation

- 6.4.15 SAP SE

- 6.4.16 Pegasystems Inc.

- 6.4.17 DataRobot Inc.

- 6.4.18 Microsoft Corporation

- 6.4.19 Hewlett Packard Enterprise Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment