PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066562

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066562

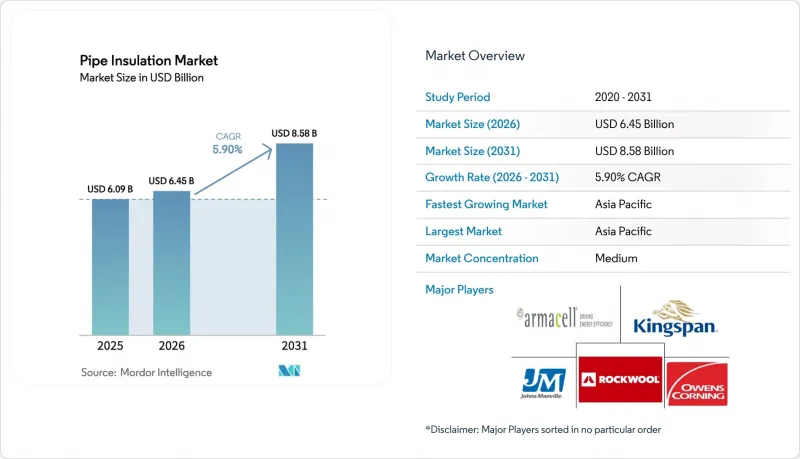

Pipe Insulation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, pipe insulation market size in 2026 is estimated at USD 6.45 billion, growing from 2025 value of USD 6.09 billion with 2031 projections showing USD 8.58 billion, growing at 5.90% CAGR over 2026-2031.

This report is Segmented by Type (Fiberglass, Rockwool, Silicates, Polyurethane, Rubber Foams, Other Types), End-User Industry (Buildings and Construction, Oil and Gas, Transportation, General Industrial, Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Pipe Insulation Market Trends and Insights

Stringent Energy-Efficiency Building Codes

Building codes are turning pipe insulation from a discretionary line item into a legal requirement. The 2024 International Energy Conservation Code (IECC) mandates thicknesses of up to 5 inches for hot-water pipelines, a rule expected to cut residential site-energy use by 7.80% in the United States. California's Title 24 and similar European directives specify minimum R-values, effectively sidelining low-performance wraps. With 14 U.S. states already on the 2024 IECC path, Northeast Energy Efficiency Partnerships forecasts 6.80% source-energy savings for early adopters. Commercial facilities mirror these requirements, pushing owners to favor lifecycle energy savings over upfront costs-another lever that expands the pipe insulation market.

Expansion of LNG and Cryogenic Pipeline Projects

Liquefied-natural-gas export terminals alo ng the U.S. Gulf Coast require more than 19,800 miles of new or replacement piping, much of it designed for -160 °C operating temperatures. Ambient-pressure aerogel pipe-in-pipe designs cut installation costs while keeping contraction stresses within allowable limits. As Asia-Pacific commissions floating LNG hubs, demand for long-run subsea insulation miles pushes premium material pricing. Manufacturers with cryogenic-grade polyurethane or cellular glass lines enjoy margin upside and early-mover contracts on multi-year megaprojects.

High Installed Cost and Labour Intensity

Field application of spray polyurethane foam and multi-layer jacketing requires certified crews and specialized rigs, pushing installation charges above USD 15/linear foot in large metro markets creating cost pressures within the pipe insulation industry. Although energy bills can drop 30% post-retrofit, Better Buildings Neighborhood data show that every USD 1 invested yields only USD 0.08 in first-year savings, stretching homeowner payback horizons. Prefabricated pipe spools partially solve the skills gap, yet transport limits hamper uptake for diameters above 12 inches. Labor scarcity is most acute in Northern Europe, where aging tradespeople retire faster than apprentices enter vocational programs. Producers respond with snap-fit mineral-fiber shells and self-adhesive aerogel wraps that cut site labor by up to 40%, but widespread adoption lags.

Other drivers and restraints analyzed in the detailed report include:

- Surging District Heating and Cooling Investments

- Smart Insulation with Embedded Sensors

- Volatile Petrochemical Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiberglass maintained the leading 39.10% pipe insulation market share in 2025, underpinned by low cost and a λ-value near 0.04 W/(m*K). Rockwool leverages inherent fire resistance and circularity claims; the brand's 2023 sales translated to anticipated lifetime energy savings of 818 TWh. Silicate wraps own niche refinery and power-plant lines above 600 °C, while rigid polyurethane foams post sub-0.02 W/(m*K) conductivities in bio-based formulations. Rubber foams remain HVAC staples because they flex with thermal cycling.

Other Types-primarily aerogel blankets and cellular glass-grow fastest at 7.13% CAGR through 2031 as mega-projects demand ultra-low heat loss. Next-gen Si3N4-reinforced aerogels come in at densities as low as 0.033 g/cm3 withstanding 893 °C differentials. Cellular glass appeals to LNG and cryogenic pipelines for zero water absorption and 100-year design life. Higher capex is offset by maintenance savings, leading process owners to specify performance-based tenders that favor premium materials.

Geography Analysis

Asia-Pacific dominates the pipe insulation market, pairing volume scale with policy support. Chinese provincial authorities now tie building permits to verified thermal-energy models, and the national Three-Year Action Plan for energy conservation identifies pipework insulation as a Tier-1 measure. India's renewable-integration drive requires process industries to cut steam line losses, sending demand toward laminated mineral-fiber shells. The Asian Development Bank's blended-financing tools de-risk greenfield heat-network projects, assuring steady material off-take.

North America benefits from LNG pipeline rollouts and code updates. The U.S. DOE's confirmation of 7.80% residential energy savings from the 2024 IECC emboldens states to adopt without lengthy cost-effectiveness debates. Federal tax credits covering 30% of insulation spend further shorten paybacks. Canadian provinces tap low-interest retrofit loans, while industrial players in Alberta hedge feedstock volatility by switching to higher-efficiency jacketing to buffer fuel bills.

Europe's ambition is to treble district cooling pipes by 2042 in cities like Paris, intertwining with the EU Renovation Wave that targets 35 million building upgrades by 2030 in the pipe insulation industry. Scandinavian markets trial carbon-negative insulation made with biogenic binders, providing early revenue for specialty manufacturers. Utilities bundle insulation contracts with heat-pump procurement, shifting supplier negotiations toward total-cost-of-ownership metrics.

- Armacell

- Aspen Aerogels, Inc.

- BASF

- Beijing Coowor Network Technology Co., Ltd.

- Cellofoam North America Inc.

- Covestro AG

- Frost King Weatherization Products / Thermwell Products Co., Inc.

- Huamei Energy-saving Technology Group Co., Ltd.

- Huntsman International LLC

- Isoclima S.p.A.

- Johns Manville

- Kingspan Group

- Knauf Insulation, Inc.

- L'Isolante K-Flex S.p.A.

- NMC sa

- ODE YalItIm A.S.

- Owens Corning

- Polyguard

- Rockwool International

- Saint-Gobain

- Thermaflex

- Zotefoams plc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Energy-Efficiency Building Codes

- 4.2.2 Expansion of LNG and Cryogenic Pipeline Projects

- 4.2.3 Surging District Heating and Cooling Investments

- 4.2.4 Smart Insulation with Embedded Sensors

- 4.2.5 Carbon-Pricing Led Industrial Retrofits

- 4.3 Market Restraints

- 4.3.1 High Installed Cost and Labour Intensity

- 4.3.2 Volatile Petrochemical Feedstock Prices

- 4.3.3 Shift to Thin-Wall Plastic Piping Alternatives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Fiberglass

- 5.1.2 Rockwool

- 5.1.3 Silicates

- 5.1.4 Polyurethane

- 5.1.5 Rubber Foams

- 5.1.6 Other Types (Aerogel Blankets,Cellular Glass, etc.)

- 5.2 By End-User Industry

- 5.2.1 Buildings and Construction

- 5.2.2 Oil and Gas

- 5.2.3 Transportation

- 5.2.4 General Industrial

- 5.2.5 Other End-user Industries (Power Generation and Utilities, Chemical and Petrochemical Processing, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Armacell

- 6.4.2 Aspen Aerogels, Inc.

- 6.4.3 BASF

- 6.4.4 Beijing Coowor Network Technology Co., Ltd.

- 6.4.5 Cellofoam North America Inc.

- 6.4.6 Covestro AG

- 6.4.7 Frost King Weatherization Products / Thermwell Products Co., Inc.

- 6.4.8 Huamei Energy-saving Technology Group Co., Ltd.

- 6.4.9 Huntsman International LLC

- 6.4.10 Isoclima S.p.A.

- 6.4.11 Johns Manville

- 6.4.12 Kingspan Group

- 6.4.13 Knauf Insulation, Inc.

- 6.4.14 L'Isolante K-Flex S.p.A.

- 6.4.15 NMC sa

- 6.4.16 ODE YalItIm A.S.

- 6.4.17 Owens Corning

- 6.4.18 Polyguard

- 6.4.19 Rockwool International

- 6.4.20 Saint-Gobain

- 6.4.21 Thermaflex

- 6.4.22 Zotefoams plc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment