PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066567

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066567

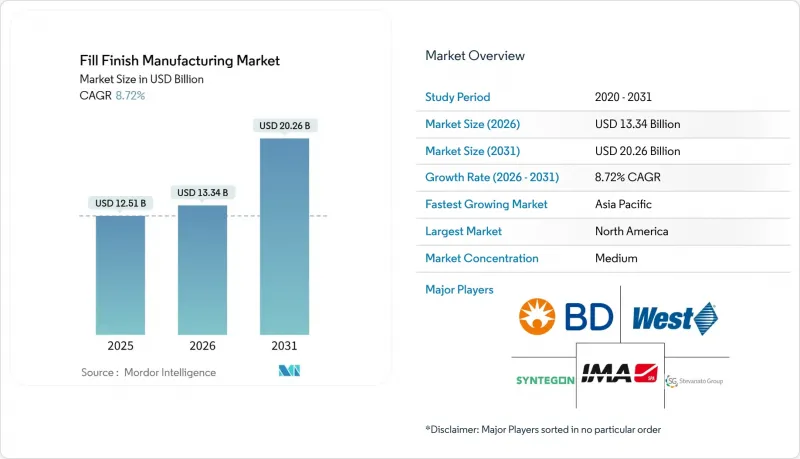

Fill Finish Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the fill finish manufacturing market size is expected to grow from USD 12.51 billion in 2025 to USD 13.34 billion in 2026 and is forecast to reach USD 20.26 billion by 2031 at 8.72% CAGR over 2026-2031.

This report is Segmented by Product Type (Consumables [Prefilled Syringes, Cartridges, Vials, Others], Instruments/Systems [Stand-Alone, Integrated, Automated, Semi-Automated/Manual]), End User (CMOs, Pharma & Biotech, Others), Container Material (Glass, Polymer), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Fill Finish Manufacturing Market Trends and Insights

Technological Advances in RTU Syringes & Cartridges

RTU formats eliminate washing and depyrogenation, trimming two to three days from production lead time and safeguarding biologics with narrow stability windows. SCHOTT's syriQ BioPure, launched in 2024, ships pre-sterilized glass barrels that cut visible-particulate rejects by 40% compared with bulk-washed components. West Pharmaceutical's expansion of Daikyo Crystal Zenith polymer cartridges in 2025 is solving silicone-oil migration challenges for single-dose GLP-1 pens. Equipment suppliers support the shift: Syntegon's ALAsys integrates RTU nest handling and reduces changeovers to under 90 minutes, enabling multi-product flexibility without serial sterilization cycles. As the Fill-Finish Manufacturing market tightens regulatory focus, the FDA and EMA now consider RTU containers a best-practice mitigation for Annex 1 contamination-control expectations, accelerating adoption by both CDMOs and captive plants.

Rising Outsourcing to CDMOs / CMOs

Capital intensity discourages innovators from building sterile suites; a single high-speed line can exceed USD 100 million in all-in costs. Samsung Biologics added four fill-finish lines during its USD 740 million Incheon expansion in 2025 to capture demand from biosimilar and mRNA vaccine sponsors. WuXi Biologics secured global contracts for adalimumab and rituximab biosimilars after upgrading its Suzhou site to 12 aseptic lines. Lonza's USD 400 million Portsmouth project introduced twin syringe lines rated at 400 units per minute, a scale that mid-sized biotech firms cannot replicate. These investments help the Fill-Finish Manufacturing market absorb surging volumes from clinical pipelines while spreading regulatory risk across specialized providers.

Stringent Global GMP & Validation Costs

Modern revisions mandate continuous environmental monitoring, three successful media fills, and annual requalification-regimens that cost USD 2 million to USD 5 million per line each year. FDA updates in 2024 added real-time particle trending, pushing firms to retrofit isolators with automated sampling nodes. China's NMPA aligned domestic GMP with ICH Q7, compelling small CDMOs to buy differential-pressure alarms and self-cleaning isolators they can scarcely afford. Validation delays lengthen time-to-market; any contaminated unit during media fills resets the 18-month qualification calendar, dampening Fill-Finish Manufacturing market momentum in resource-constrained regions.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Biologics & Injectable Pipeline

- Sustainability Push for Recyclable Polymer Components

- High CAPEX for Aseptic Fill-Finish Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumables anchored 62.81% of 2025 revenue because every batch consumes fresh vials, stoppers, cartridges, and prefilled syringes. Yet the Fill-Finish Manufacturing market size for instruments and systems is expanding faster, clocking a 9.50% CAGR that reflects industry fixation on throughput and compliance. Automated monoblocs integrate filling, stoppering, capping, and 100% vision inspection in one housing, curbing operator intervention and data-integrity risks. Syntegon's ALAsys and IMA's Adapta lines clock 400-plus units per minute while maintaining +-1% fill accuracy; CDMOs invest here to assure slot reservations from big pharma sponsors. Semi-automated equipment lingers in low-income geographies where labor costs undercut robotics, but incoming ICH-aligned GMP rules in India and China will nudge buyers toward full automation.

Consumables nonetheless remain indispensable and recession-resistant within the Fill-Finish Manufacturing market. Prefilled syringes are gaining share as GLP-1 injectables migrate from vials, while cartridge usage is ballooning on the back of pen devices for chronic diseases. Suppliers secure multi-year contracts bundling barrels, elastomer plungers, and needle shields, effectively locking customers into proprietary ecosystems. New RTU nests simplify line changeovers; SCHOTT's NxT packaging reduces component prep time by 50%, an intangible yet important benefit as line-utilization targets creep past 80%. Sustainability considerations now influence bill-of-materials: polymer suppliers offering closed-loop recycling enjoy preferred-supplier status with procurement teams under ESG scorecard pressure.

Geography Analysis

North America retained 37.44% of global billings in 2025 thanks to its dense cluster of innovators, marquee CDMOs, and a robust FDA inspection framework. The region hosts an estimated 180 commercial aseptic lines, many embedded in vertically integrated big-pharma campuses that demand 95% runtime reliability. Mexico is building syringe capacity in Juarez to serve U.S. near-shoring strategies, trimming customs delays and tariff risk. Canada's growth is modest but focused on biosimilars; two new lines at Apotex and Pharmascience will collectively deliver 120 million prefilled devices per year by 2027.

Europe combines world-class container suppliers with complex regulatory dynamics. Post-Brexit divergence forces dual MHRA and EMA validations, nudging multinational CDMOs to favor continental hubs in Germany and Italy. The EU waste directive increases operating expenses for polymer-heavy operations, yet Gerresheimer, SCHOTT, and Stevanato Group leverage in-house R&D to pioneer recyclable platforms that square GMP sterility with environmental targets. Eastern European nations position themselves as lower-cost fill-finish nodes, yet many still lack the inspection history demanded by U.S. buyers, stalling cross-Atlantic contracts.

Asia-Pacific is the clear growth engine, advancing at an 9.82% CAGR and gradually disrupting established trade routes in the Fill-Finish Manufacturing market. China's NMPA cleared 23 biosimilars over 2024-2025, catalyzing USD 200 million-plus expansions at WuXi Biologics and Fosun Pharma. India's Serum Institute readied six lines capable of 1.5 billion doses annually, anchoring GAVI procurement for polio and HPV. South Korea funnels public incentives into Samsung Biologics and SK Bioscience, both of which embed local robotics expertise for lights-out syringe packaging. Japan's demographic focus on aging spurs in-country capacity for long-acting injectables, though its stringent PMDA validation extends lead times relative to Korea and Singapore.

- Aptar

- Bausch+Strobel

- Beckton Dickinson

- Corning

- Daikyo Seiko Ltd.

- FUJIFILM

- Gerresheimer

- Groninger & Co. GmbH

- IMA S.p.A.

- Marchesini Group S.p.A.

- Nipro

- Novo Nordisk A/S (Catalent, Inc.)

- OPTIMA Packaging Group GmbH

- Owen Mumford Pharmaceutical Services (UK)

- SCHOTT

- SGD Pharma

- Stevanato Group

- Syntegon Technology

- Thermo Fisher Scientific (Patheon)

- West Pharmaceutical Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological advances in RTU syringes & cartridges

- 4.2.2 Rising outsourcing to CDMOs / CMOs

- 4.2.3 Expanding biologics & injectable pipeline

- 4.2.4 Sustainability push for recyclable polymer components

- 4.2.5 Modular micro-batch isolator systems for cell & gene therapies

- 4.2.6 AI-driven predictive maintenance of fill-finish lines

- 4.3 Market Restraints

- 4.3.1 Stringent global GMP & validation costs

- 4.3.2 High CAPEX for aseptic fill-finish lines

- 4.3.3 EU plastics-waste regulation on single-use disposables

- 4.3.4 Talent shortage for advanced-therapy micro-batch lines

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Consumables

- 5.1.1.1 Prefilled Syringes

- 5.1.1.2 Cartridges

- 5.1.1.3 Vials

- 5.1.1.4 Others

- 5.1.2 Instruments / Systems

- 5.1.2.1 Stand-Alone Systems

- 5.1.2.2 Integrated Lines

- 5.1.2.3 Automated Machines

- 5.1.2.4 Semi-Automated / Manual Machines

- 5.1.1 Consumables

- 5.2 By End User

- 5.2.1 Contract Manufacturing Organizations

- 5.2.2 Pharmaceutical & Biotechnology Firms

- 5.2.3 Others

- 5.3 By Container Material

- 5.3.1 Glass

- 5.3.2 Polymer (COP/COC & other plastics)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Aptar

- 6.3.2 Bausch+Strobel

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Corning Incorporated

- 6.3.5 Daikyo Seiko Ltd.

- 6.3.6 FUJIFILM Diosynth Biotechnologies

- 6.3.7 Gerresheimer AG

- 6.3.8 Groninger & Co. GmbH

- 6.3.9 IMA S.p.A.

- 6.3.10 Marchesini Group S.p.A.

- 6.3.11 Nipro Corporation

- 6.3.12 Novo Nordisk A/S (Catalent, Inc.)

- 6.3.13 OPTIMA Packaging Group GmbH

- 6.3.14 Owen Mumford Pharmaceutical Services (UK)

- 6.3.15 SCHOTT AG

- 6.3.16 SGD Pharma

- 6.3.17 Stevanato Group

- 6.3.18 Syntegon Technology GmbH

- 6.3.19 Thermo Fisher Scientific (Patheon)

- 6.3.20 West Pharmaceutical Services

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment