PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066570

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066570

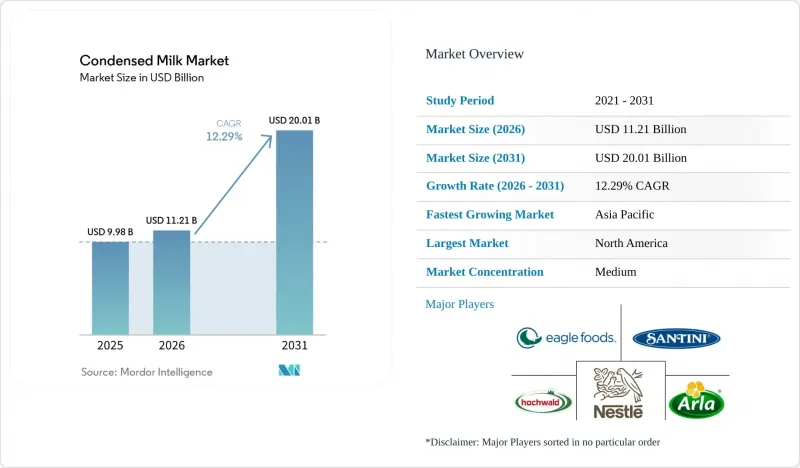

Condensed Milk - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the condensed milk market size is projected to be USD 9.98 billion in 2025, USD 11.21 billion in 2026, and reach USD 20.01 billion by 2031, growing at a CAGR of 12.29% from 2026 to 2031.

This report is Segmented by Product Type (Dairy and Non-Dairy/Plant-Based); Category (Sweetened Condensed Milk and Unsweetened Evaporated Milk), Packaging Type (Cans, Tubes, Bottles and Pouches, Cartons, and Others); Distribution Channel (Retail, Foodservice, and Industrial); and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Condensed Milk Market Trends and Insights

Surge in Bakery and Confectionery Manufacturing Capacity

Industrial bakeries and confectionery producers are expanding production to meet the growing demand for shelf-stable ingredients, driving consistent demand for condensed milk. This ingredient is widely used as a sweetener, moisture-retention agent, and flavor enhancer. In 2024, Ferrero enhanced its North American operations by acquiring WK Kellogg for USD 2.8 billion, while Mondelez invested in emerging markets to localize supply chains and reduce import tariffs. Barry Callebaut expanded cocoa-processing facilities in West Africa and Southeast Asia, reflecting a trend of vertical integration to control costs and maintain quality. Condensed milk is essential in products like filled chocolates, caramel centers, and baked goods, serving as a sugar substitute and textural modifier. Manufacturers are focusing on balancing sweetness with longer shelf life, especially in the Asia-Pacific region, where urbanization and rising incomes are boosting demand for packaged confectionery and premium bakery products. According to the most recent data available from the International Dairy Deli Bakery Association, for 2024, sales in total bakery were up 5.7% from the prior year to USD 43.5 billion. This growth generated increased demand for condensed milk as an essential ingredient in various baked goods, including cakes, pastries, and confectioneries. Its versatility in enriching dough and creating fillings and toppings solidifies its importance in bakery applications.

Growing Use of Sweetened Condensed Milk in RTD Coffee Beverages

Ready-to-drink (RTD) coffee brands are now adding sweetened condensed milk, achieving a creamy texture and natural sweetness without the need for refrigeration. This is especially advantageous in markets where cold-chain infrastructure is limited. The RTD coffee segment is witnessing rapid growth in the Asia-Pacific region. Here, countries like Vietnam, Thailand, and Indonesia, with their traditional coffee culture, prominently feature condensed milk as a staple ingredient. In a notable move, Nestle's Carnation brand has introduced vegan condensed milk formulations, crafted from oat and rice flour. This strategy aims to attract lactose-intolerant consumers and align with the growing plant-based trend. It underscores a significant shift: even established dairy brands are diversifying their ingredient platforms. Beverage formulators are increasingly valuing condensed milk not just for its creamy texture, but also for its ability to mask the bitterness of robusta coffee blends. Moreover, its high sugar content extends shelf life, minimizing the need for preservatives. This evolving dynamic is prompting RTD coffee producers to adjust their ingredient procurement strategies. They're now pursuing long-term supply agreements with condensed milk manufacturers, ensuring locked-in pricing and consistent quality.

Volatility in Global Whole-Milk Powder Prices

Raw material price fluctuations create margin pressure for condensed milk manufacturers. Weather-related disruptions in major dairy-producing regions, combined with geopolitical tensions affecting trade flows, amplify price volatility and complicate long-term contract negotiations between suppliers and food manufacturers. Smaller producers face particular challenges in managing price risk, as they lack the scale to implement sophisticated hedging strategies or negotiate volume-based pricing agreements with dairy suppliers. The 7% decline in Argentine milk production forecasted for 2024 due to economic instability illustrates how regional supply shocks can cascade through global pricing mechanisms, according to the United States Department of Agriculture . Forward contracting becomes essential for maintaining competitive positioning, though it requires working capital commitments that strain smaller operators' financial resources.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Vegan/Plant-Based Condensed Coconut and Oat Formulations

- Long Shelf Life Boosts Demand

- Logistics Cold-Chain Gaps: Distribution Challenges Persist

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tubes are expected to grow at a 12.48% CAGR through 2031, driven by their convenience, reduced waste, and single-serve formats that suit on-the-go consumers and small households. Unlike traditional cans, which require full consumption or refrigeration after opening, tubes allow precise dispensing, reduce oxidation, and extend usability. This makes them ideal for retail consumers and foodservice operators seeking flexibility. Tetra Pak's retortable carton technology, combining aseptic processing with fiber-based barriers, offers a sustainable alternative to metal cans. With 70% paperboard content, these cartons align with sustainability goals and consumer demand for reduced plastic use.

In 2025, cans accounted for 56.8% of the packaging market, supported by established supply chains, consumer familiarity, and cost efficiency in bulk production. Metal cans provide excellent barriers against light, oxygen, and moisture, ensuring long-term product stability without refrigeration. They dominate in emerging markets, where durability and bulk purchasing are priorities. However, sustainability concerns challenge cans due to the high carbon footprint of aluminum and steel production and low recycling rates in many regions. Bottles, pouches, and cartons cater to niche needs for resealability and transparency but face limitations from higher costs and complex processing.

In 2025, sweetened condensed milk held a 70.5% category share, driven by its role in desserts, beverages, and confections. Its high sugar content enhances flavor, preserves shelf life, and delivers the creamy texture and caramelized sweetness consumers expect. This product remains a staple in traditional recipes like Vietnamese coffee, Thai tea, and Brazilian brigadeiro, especially in Asia-Pacific and Latin America. In North America, brands like Nestle's Carnation and Eagle Foods' Borden maintain strong market positions by leveraging brand recognition and extensive distribution to compete with private-label products.

Unsweetened evaporated milk is growing at a 13.59% CAGR through 2031, supported by demand from foodservice operators and industrial users seeking lower-sugar options for sauces, soups, and coffee blends. It appeals to health-conscious consumers and institutional buyers, particularly in Western Europe and North America, where sugar-reduction trends are reshaping products. With higher protein and calcium content, it is also used in infant nutrition and pediatric formulations to meet regulatory standards. Arla's £90 million investment in its Lockerbie UHT center highlights the category's growth potential. Post-pandemic foodservice recovery has further boosted demand for shelf-stable dairy products, increasing the adoption of unsweetened evaporated milk in commercial kitchens.

Geography Analysis

In 2025, North America holds a 41.22% market share, supported by its strong food processing infrastructure and focus on premium products. At the same time, the Asia-Pacific region is the fastest-growing, with a 12.01% CAGR projected through 2031, driven by urbanization and rising disposable incomes. In North America, the condensed milk market is adapting to changing consumer preferences and production trends. The United States remains the largest consumer, with the USDA estimating milk production to reach 228.2 billion pounds in 2024, a 0.7% increase due to higher per-cow output despite smaller herd sizes . Additionally, consumer interest is shifting toward premium and specialty products, particularly in the ready-to-drink (RTD) coffee market. Condensed milk is a key ingredient in cold brew coffee and nutrient-enriched beverages, which are increasingly popular among younger consumers.

In the Asia-Pacific region, urbanization and the growing cafe culture are driving market growth. In Vietnam, Vinamilk and FrieslandCampina dominate domestic production, reflecting both a concentration of market share and strong brand presence. In Indonesia, the steady growth of sweetened condensed milk sales highlights its continued popularity, especially in traditional beverages, as noted by the World Bank. However, limited cold-chain infrastructure restricts market access in rural areas of Indonesia and India. Efforts to address this issue are underway, with infrastructure investments supported by multilateral funding aiming to expand market opportunities in these regions.

In Europe, the focus is on sustainability and quality certifications. According to the European Dairy Association, milk production is expected to reach 145 million tonnes in 2024. Processors are increasingly channeling this output into value-added products instead of traditional commodity butter. Northern European consumers, who are highly conscious of carbon footprints, are showing a growing preference for plant-based condensed milk. This trend is encouraging established dairy companies to acquire or collaborate with niche vegan brands. In Eastern Europe, price sensitivity continues to drive demand for sweetened canned products, which are primarily imported from Poland and the Netherlands.

- Nestle S.A.

- FrieslandCampina N.V.

- Fonterra Co-operative Group Ltd.

- Eagle Foods

- Arla Foods amba

- Vinamilk

- PT Indofood CBP (Indolakto)

- Hochwald Foods GmbH

- Dana Dairy Group Ltd.

- Gujarat Co-operative Milk Marketing Fed. (Amul)

- Morinaga Milk Industry Co., Ltd.

- Santini Foods, Inc.

- United Dairy Ltd.

- Nature's Charm Co. Ltd.

- Alaska Milk Corp.

- Fraser & Neave Holdings Bhd.

- Parmalat S.p.A (Lactalis)

- Almarai Company

- Borden Dairy Company

- Milky Mist Dairy Food Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Bakery and Confectionery Manufacturing Capacity

- 4.2.2 Growing Use of Sweetened Condensed Milk in RTD Coffee Beverages

- 4.2.3 Rise of Vegan/Plant-Based Condensed Coconut and Oat Formulations

- 4.2.4 Long Shelf Life Boosts Demand

- 4.2.5 Convenience and Versatility of Usage

- 4.2.6 Rising Demand for Shelf-Stable Desserts in Tourist Hubs

- 4.3 Market Restraints

- 4.3.1 Volatility in Global Whole-Milk Powder Prices

- 4.3.2 Logistics Cold-Chain Gaps

- 4.3.3 Stringent Import Quotas on Dairy Fat

- 4.3.4 Availability of Alternatives

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Product Type

- 5.1.1 Dairy

- 5.1.2 Non-Dairy/Plant-Based

- 5.2 By Category

- 5.2.1 Sweetened Condensed Milk

- 5.2.2 Unsweetened Evaporated Milk

- 5.3 By Packaging Type

- 5.3.1 Cans

- 5.3.2 Tubes

- 5.3.3 Bottles and Pouches

- 5.3.4 Cartons (Tetra Pak and Others)

- 5.3.5 Others

- 5.4 By Distribution Channel

- 5.4.1 Retail

- 5.4.1.1 Supermarkets/Hypermarkets

- 5.4.1.2 Convenience Stores

- 5.4.1.3 Specialty Stores

- 5.4.1.4 Online Retail

- 5.4.2 Foodservice

- 5.4.3 Industrial

- 5.4.3.1 Bakery and Confectionery

- 5.4.3.2 Beverages and Dairy-Based Drinks

- 5.4.3.3 Infant and Pediatric Nutrition

- 5.4.3.4 Others

- 5.4.1 Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nestle S.A.

- 6.4.2 FrieslandCampina N.V.

- 6.4.3 Fonterra Co-operative Group Ltd.

- 6.4.4 Eagle Foods

- 6.4.5 Arla Foods amba

- 6.4.6 Vinamilk

- 6.4.7 PT Indofood CBP (Indolakto)

- 6.4.8 Hochwald Foods GmbH

- 6.4.9 Dana Dairy Group Ltd.

- 6.4.10 Gujarat Co-operative Milk Marketing Fed. (Amul)

- 6.4.11 Morinaga Milk Industry Co., Ltd.

- 6.4.12 Santini Foods, Inc.

- 6.4.13 United Dairy Ltd.

- 6.4.14 Nature's Charm Co. Ltd.

- 6.4.15 Alaska Milk Corp.

- 6.4.16 Fraser & Neave Holdings Bhd.

- 6.4.17 Parmalat S.p.A (Lactalis)

- 6.4.18 Almarai Company

- 6.4.19 Borden Dairy Company

- 6.4.20 Milky Mist Dairy Food Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK