PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066575

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066575

Home Fragrances - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

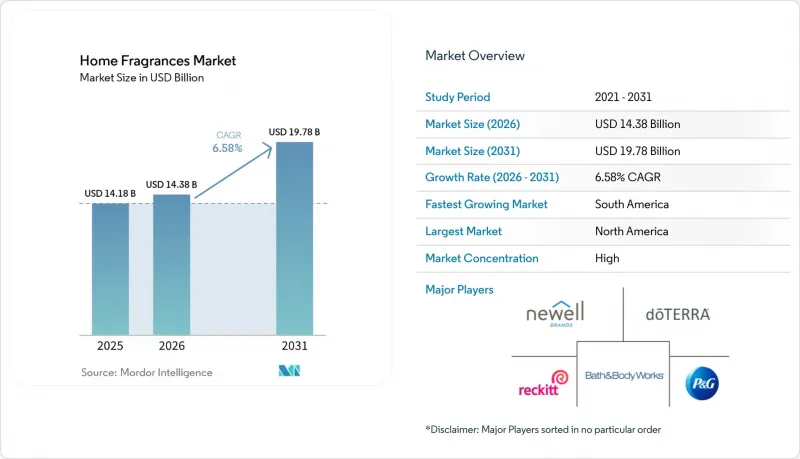

According to Mordor Intelligence, the home fragrances market was valued at USD 14.18 billion in 2025 and estimated to grow from USD 14.38 billion in 2026 to reach USD 19.78 billion by 2031, at a CAGR of 6.58% during the forecast period (2026-2031).

This report is Segmented by Product Type (Sprays, Diffusers, Scented Candles, Other Types), Category (Premium and Mass), Distribution Channel (Supermarkets and Hypermarkets, Specialty Stores, Online Retail, Other Distribution Channel), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Home Fragrances Market Trends and Insights

Rising preference for multifunctional home-fragrance solutions

Rising preference for multifunctional home-fragrance solutions is significantly driving growth in the home fragrances market, as consumers increasingly seek products that deliver both sensory appeal and practical benefits. Modern households favor fragrance formats that combine aroma with added functionalities such as air purification, odor neutralization, humidity control, or wellness support through aromatherapy. This shift aligns with growing demand for cleaner, healthier indoor environments and products that enhance overall home ambience. Brands are responding by integrating advanced diffusing technologies, natural essential oils, and antibacterial or mood-enhancing properties into their offerings. Multifunctional solutions also appeal to space-conscious consumers who prefer fewer, more effective products. Additionally, rising awareness of indoor air quality and holistic living strengthens adoption of these hybrid innovations.

Surge in premium and artisanal candle sales supported by a strong gifting culture

The premium candle market is undergoing a notable shift driven by the rapid rise of direct-to-consumer (DTC) brands. By eliminating traditional retail intermediaries, these brands are boosting margins while offering highly personalized and emotionally engaging gifting experiences. Once considered occasional luxuries, premium candles have become meaningful, year-round lifestyle statements. This evolution is closely linked to growing conscious consumerism, with buyers seeking eco-friendly, ethically crafted products. In response, premium brands such as Keap Candles and 1986 Home are adopting natural waxes like soy and coconut, creating visually appealing reusable containers, and investing in sustainable, biodegradable packaging. These changing dynamics are pushing mass-market companies to launch premium extensions, while niche artisanal makers broaden their presence through collaborations with gourmet and concept retailers, delivering curated sensory experiences that enhance brand perception and strengthen customer loyalty.

Rising presence of counterfeit and imitation home-aroma products

The rising prevalence of counterfeit and imitation home fragrance products is increasingly restraining the growth of the market, posing risks to both consumers and legitimate brands. These low-cost replicas often mimic the packaging and scent profiles of premium products but compromise on quality, safety, and ingredient integrity. Many counterfeit items contain harmful chemicals, unregulated additives, or substandard fragrance oils, raising concerns over indoor air quality and potential health effects. Their widespread availability across online marketplaces and informal retail channels fuels consumer confusion, dilutes brand trust, and reduces repeat purchases. Authentic brands face revenue losses and difficulties in protecting intellectual property as imitation products continue to circulate. Moreover, price-sensitive consumers may unknowingly choose cheaper counterfeit alternatives, further undermining demand for genuine offerings.

Other drivers and restraints analyzed in the detailed report include:

- Increasing consumer focus on home aesthetics and wellness-driven lifestyles

- Growing impact of social media channels on home-aroma purchasing behaviour

- Increasing consumer worries regarding chemical-based ingredients

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sprays accounted for 31.57% of total revenue in 2025, making them the most dominant segment in the home fragrances market. Their widespread adoption stems from their ability to deliver an immediate burst of fragrance, meeting consumer expectations for quick and convenient odor control. They are particularly effective in high-traffic zones such as bathrooms, kitchens, and entryways, where instant refreshment is valued. The portability and ease of use of spray formats also contribute to frequent household replenishment. Additionally, the wide availability of scent varieties and price points allows sprays to appeal to both mass-market and premium consumers. As a result, this category continues to hold a strong competitive edge and remains the preferred choice for everyday fragrance needs.

Scented candles are projected to grow at a CAGR of 7.21% through 2031, making them the fastest-expanding segment in the home fragrances industry. This growth rate surpasses the overall market, highlighting the strong consumer shift toward premium and experiential home aromas. Their momentum is fueled by rising premiumization trends, where consumers increasingly seek artisanal, design-forward, and long-lasting candle options. Social-media influence, particularly on aesthetic-driven platforms, has amplified candle visibility and shaped purchasing behavior. Additionally, candles remain a popular and recurring gifting choice across festive seasons, personal celebrations, and lifestyle occasions.

Geography Analysis

North America remains the dominant region in the global home fragrances market, holding approximately 49.58% of the market share in 2025. This leadership is supported by strong consumer expenditure on home improvement and a mature, well-organized retail network. Seasonal fragrance rotation is deeply embedded in consumer culture, further reinforcing the region's consistent demand. Although container-based scented candles continue to be widespread, there is a notable transition toward premium, artisanal, and design-driven products as consumers increasingly value uniqueness and quality. Battery-powered fragrance diffusers are also gaining popularity due to their convenience, portability, and flame-free operation, offering a modern alternative to traditional formats. Collectively, these factors help sustain North America's commanding position in the global market.

South America is projected to be the fastest-growing region, with a CAGR of 7.97% from 2026 to 2031, reflecting significant expansion opportunities for manufacturers. In Brazil, sprays currently dominate revenue contribution; however, scented candles are emerging as the fastest-growing category, showcasing evolving consumer preferences. The region's momentum is fueled by rising disposable incomes, continued urbanization, and heightened interest in ambiance-enhancing and aesthetically appealing home fragrance products. Growing consumer exposure to global home decor trends is also influencing the adoption of diverse fragrance formats. This shift indicates a broadening market beyond functional products toward more premium and experiential offerings.

Europe demonstrates consistently high demand for eco-friendly, natural, and wellness-oriented home fragrance products, especially in the United Kingdom and Germany. This trend is supported by a health-conscious consumer base that increasingly scrutinizes ingredients and sustainability credentials. The Asia-Pacific region, including China, India, Japan, and Australia, is witnessing steady expansion driven by increasing disposable incomes, rapid urbanization, and long-standing cultural preferences for aromatic and ambiance-enhancing products. The Middle East and Africa are experiencing strong adoption of premium and traditional fragrance forms, such as incense, bakhoor, and ornate candles.

- SC Johnson & Sons Inc.

- Reckitt Benckiser Group plc

- The Procter & Gamble Company

- Newell Brands Inc.

- Bath & Body Works Inc.

- Godrej Consumer Products Limited

- Henkel AG and Co. KGaA

- doTERRA International LLC

- Puzhen Life Co. Ltd.

- L'Occitane Groupe SA

- Nest New York (NEST Fragrances)

- Scentsy Inc.

- Prolitec Inc.

- Voluspa LLC

- Diptyque

- Ryohin Keikaku Co., Ltd.

- The Estee Lauder Companies Inc.

- ScentAir Technologies LLC

- Faultless Brands

- Seda France Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising preference for multifunctional home-fragrance solutions

- 4.2.2 Surge in premium and artisanal candle sales supported by a strong gifting culture

- 4.2.3 Increasing consumer focus on home aesthetics and wellness-driven lifestyles

- 4.2.4 Growing impact of social media channels on home-aroma purchasing behaviour

- 4.2.5 Seasonal and limited-edition releases driving fresh buying occasions

- 4.2.6 Expansion of e-commerce enhancing product availability and boosting direct-to-consumer sales

- 4.3 Market Restraints

- 4.3.1 Rising presence of counterfeit and imitation home-aroma products

- 4.3.2 Increasing consumer worries regarding chemical-based ingredients

- 4.3.3 Tightening volatile organic compounds compliance standards restricting product formulation options

- 4.3.4 Supply chain volatility impacting the availability of key raw materials

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Sprays

- 5.1.2 Diffusers

- 5.1.3 Scented Candles

- 5.1.4 Other Types

- 5.2 By Category

- 5.2.1 Premium

- 5.2.2 Mass

- 5.3 By Distribution Channel

- 5.3.1 Supermarkets and Hypermarkets

- 5.3.2 Specialty Stores

- 5.3.3 Online Retail

- 5.3.4 Other Distribution Channel

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 United Kingdom

- 5.4.2.4 Spain

- 5.4.2.5 Netherlands

- 5.4.2.6 Italy

- 5.4.2.7 Sweden

- 5.4.2.8 Poland

- 5.4.2.9 Belgium

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Indonesia

- 5.4.3.7 Singapore

- 5.4.3.8 Thailand

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Colombia

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 United Arab Emirates

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, and Recent Developments)

- 6.4.1 SC Johnson & Sons Inc.

- 6.4.2 Reckitt Benckiser Group plc

- 6.4.3 The Procter & Gamble Company

- 6.4.4 Newell Brands Inc.

- 6.4.5 Bath & Body Works Inc.

- 6.4.6 Godrej Consumer Products Limited

- 6.4.7 Henkel AG and Co. KGaA

- 6.4.8 doTERRA International LLC

- 6.4.9 Puzhen Life Co. Ltd.

- 6.4.10 L'Occitane Groupe SA

- 6.4.11 Nest New York (NEST Fragrances)

- 6.4.12 Scentsy Inc.

- 6.4.13 Prolitec Inc.

- 6.4.14 Voluspa LLC

- 6.4.15 Diptyque

- 6.4.16 Ryohin Keikaku Co., Ltd.

- 6.4.17 The Estee Lauder Companies Inc.

- 6.4.18 ScentAir Technologies LLC

- 6.4.19 Faultless Brands

- 6.4.20 Seda France Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK