PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066580

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066580

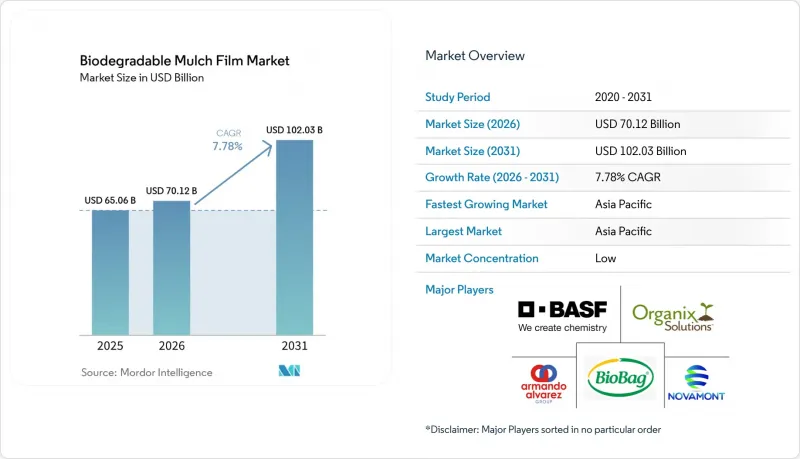

Biodegradable Mulch Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, biodegradable mulch film market size in 2026 is estimated at USD 70.12 million, growing from 2025 value of USD 65.06 million with 2031 projections showing USD 102.03 million, growing at 7.78% CAGR over 2026-2031.

This report Segments by Polymer (Starch, Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Aliphatic-Aromatic Copolymers (AAC), and More), Crop Type (Fruits and Vegetables, Flowers and Ornamentals, and More), Farming System (Open-Field Cultivation, and More), Film Thickness (Up To 0. 6 Mil, and More), Sales Channel (B2B, and B2C) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Biodegradable Mulch Film Market Trends and Insights

Expansion of Greenhouse Cultivation

Global greenhouse acreage keeps rising, creating a premium niche inside the biodegradable mulch film market where growers willingly absorb higher material costs to secure certification compliance and eliminate plastic-removal labor. Controlled environments stabilize soil temperature and moisture, ensuring predictable degradation and strong crop-yield uplifts. European vegetable clusters now demand soil-biodegradable films to meet retailer sustainability scorecards, while high-tech greenhouse hubs in Japan employ film farming systems that integrate seamlessly with bio-based polymers. Reliable in-house monitoring of degradation data accelerates iterative formulation improvements, reinforcing manufacturer feedback loops and justifying premium price positions within the biodegradable mulch film market.

Government Mandates and Subsidies for Soil-Biodegradable Films

Subsidy programs and labeling rules are translating sustainability goals into near-term sales. California's AB 1201 compels compostable products used in agriculture to satisfy USDA National Organic Program requirements by January 2026, effectively carving out an early-mover advantage for certified films. Minnesota mirrors the approach with third-party certification deadlines in the same year. The European Union's tighter migration thresholds for plastic materials from March 2025 raise compliance costs for polyethylene mulch, driving substitution. Inclusion of soil-biodegradable mulch films on the US National List of Approved Synthetic Substances further expands organic-farming addressable acreage. Collectively, these interventions inject clarity into return-on-investment calculations and spur R&D budgets across the biodegradable mulch film market.

High Film and Installation Cost vs. PE Alternatives

At farm-gate, biodegradable rolls remain 2-3 times pricier than standard polyethylene, and specialized applicators may be needed to prevent premature tearing during laying. Lower-margin grain growers therefore hesitate, limiting rapid uptake outside premium crops. Although savings from avoided removal labor and landfill fees balance costs over multi-season horizons, financing hurdles persist for smallholder operations in Southeast Asia and Africa. Manufacturers must continue resin cost-down programs if the biodegradable mulch film market is to penetrate price-sensitive commodity segments.

Other drivers and restraints analyzed in the detailed report include:

- Rising Disposal-Cost Penalties on Polyethylene Mulch

- Localization of Low-Cost Cassava and Potato Starch Feedstock

- Inconsistent Field-Degradation and Additive-Leaching Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Starch-based products held 46.88% of biodegradable mulch film market share in 2025, reflecting favorable feedstock economics and mature extrusion know-how. Hybrid blends that combine starch, PLA, and PBS are seeing 10.78% CAGR, propelled by durability in films thicker than 1.0 mil. BASF's Ecovio M2351 demonstrates how tailored PBAT/PLA mixes meet mechanical-strength thresholds while passing soil-disintegration standards.

Advances in cassava- and potato-modified starch have narrowed moisture-barrier gaps, cutting defect rates in tropical field trials and improving mechanical performance relative to earlier starch films.The biodegradable mulch film market size for hybrids is forecast to climb once microplastic rules force incremental PBAT replacement, pushing demand toward fully mineralizable systems. Polylactic-acid volumes remain stable in premium greenhouse crops where predictable degradation outweighs cost concerns, while emerging PHA captures coastal acreage building on its marine-safe profile.

Fruits and vegetables captured 67.74% of the biodegradable mulch film market size in 2025, underpinned by high per-acre revenue that justifies premium field inputs. Flowers and ornamentals, though smaller, will log 10.42% CAGR as consumer demand for sustainably produced blooms grows across Europe and North America.

Watermelon-specific Bio360 films exemplify crop-tailored design, offering heat management and wind resistance features valued in melon belts. Herbs and organic salad greens follow similar trajectories, leveraging yield lifts of 8-9% recorded in recent MDPI trials. Lower-margin grains remain tentative adopters as price gaps vs. polyethylene persist, but pilot projects integrating carbon-credit revenue are beginning to shift the calculus, broadening the biodegradable mulch film market.

Geography Analysis

Asia-Pacific commanded 41.02% of global revenue in 2025 and is expanding at 11.98% CAGR through 2031, buoyed by China's vast protected-vegetable acreage and India's subsidy schemes for bio-based farm inputs. Thailand's cassava industry underpins local resin supply, trimming landed costs and enhancing competitiveness for domestic suppliers. Japanese material-evaluation breakthroughs shorten R&D cycles, ensuring regionally formulated films suit humid monsoon climates. Collectively, these factors cement Asia-Pacific as the centerpiece of the biodegradable mulch film market.

Europe ranks second by value, anchored by aggressive plastic-waste directives and large organic-farming footprints. German and Italian greenhouse hubs intensify demand, while EU migration-limit rules on food-contact plastics indirectly favor soil-biodegradable alternatives. Novamont collaborates with Bayer to integrate Mater-Bi clips and twine, extending system solutions beyond film alone. This holistic approach positions Europe as a technology and standards leader within the biodegradable mulch film market.

North America shows steady but policy-led growth. California's compostability labeling law and extended-producer-responsibility schemes elevate compliance hurdles for polyethylene mulch, steering acreage toward certified soil-biodegradable alternatives. The United States processes only 9% of farm plastic waste, magnifying disposal cost savings when growers switch. Precision-ag mapping further supports regional expansion, identifying micro-zones of optimum degradation in the Corn Belt. Together, these levers sustain a healthy pipeline for the biodegradable mulch film market across the continent.

- BASF SE

- Novamont SpA

- BioBag International AS

- Kingfa Sci & Tech Co Ltd

- Armando Alvarez Group

- Organix Solutions

- RKW Group

- Barbier Group

- Dubois Agrinovation

- Agriplast Tech India Pvt Ltd

- Pooja Plastic Industries

- Walki Group

- Hopewell Industries

- AEP Industries Inc.

- NatureWorks LLC

- Groupe Guillin

- Taghleef Industries

- Braskem S.A.

- GreenPak LLC

- Plastiroll Oy (BioBag Finland)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of greenhouse cultivation

- 4.2.2 Government mandates and subsidies for soil-biodegradable films

- 4.2.3 Rising disposal-cost penalties on polyethylene mulch

- 4.2.4 Localization of low-cost cassava/potato starch feedstock

- 4.2.5 Biochar-enriched films unlocking carbon-credit revenue

- 4.2.6 GIS-based suitability mapping widens arable adoption zones

- 4.3 Market Restraints

- 4.3.1 High film and installation cost vs. PE alternatives

- 4.3.2 Inconsistent field-degradation and additive-leaching risks

- 4.3.3 Impending microplastic rules on PBAT blends

- 4.3.4 Competition from paper mulch and spray-on biopolymer coatings

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Polymer

- 5.1.1 Starch

- 5.1.2 Polylactic Acid (PLA)

- 5.1.3 Polyhydroxyalkanoates (PHA)

- 5.1.4 Aliphatic-Aromatic Copolymers (AAC)

- 5.1.5 Polybutylene Adipate-Terephthalate (PBAT)

- 5.1.6 Polybutylene Succinate (PBS)

- 5.1.7 Hybrid Biodegradable Polymer

- 5.2 By Crop Type

- 5.2.1 Fruits and Vegetables

- 5.2.2 Flowers and Ornamentals

- 5.2.3 Grains and Oilseeds

- 5.2.4 Other Specialty Crops

- 5.3 By Farming System

- 5.3.1 Open-Field Cultivation

- 5.3.2 Greenhouse / High Tunnel

- 5.4 By Film Thickness

- 5.4.1 <=0.6 mil

- 5.4.2 0.7-1.0 mil

- 5.4.3 More than 1.0 mil (heavy-duty)

- 5.5 By Sales Channel

- 5.5.1 B2B (Agricultural Dealers and Distributors)

- 5.5.2 B2C (Direct-to-Farmer and E-commerce)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Russia

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 Rest of Asia-Pacifc

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Kenya

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Novamont SpA

- 6.4.3 BioBag International AS

- 6.4.4 Kingfa Sci & Tech Co Ltd

- 6.4.5 Armando Alvarez Group

- 6.4.6 Organix Solutions

- 6.4.7 RKW Group

- 6.4.8 Barbier Group

- 6.4.9 Dubois Agrinovation

- 6.4.10 Agriplast Tech India Pvt Ltd

- 6.4.11 Pooja Plastic Industries

- 6.4.12 Walki Group

- 6.4.13 Hopewell Industries

- 6.4.14 AEP Industries Inc.

- 6.4.15 NatureWorks LLC

- 6.4.16 Groupe Guillin

- 6.4.17 Taghleef Industries

- 6.4.18 Braskem S.A.

- 6.4.19 GreenPak LLC

- 6.4.20 Plastiroll Oy (BioBag Finland)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment