PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066581

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066581

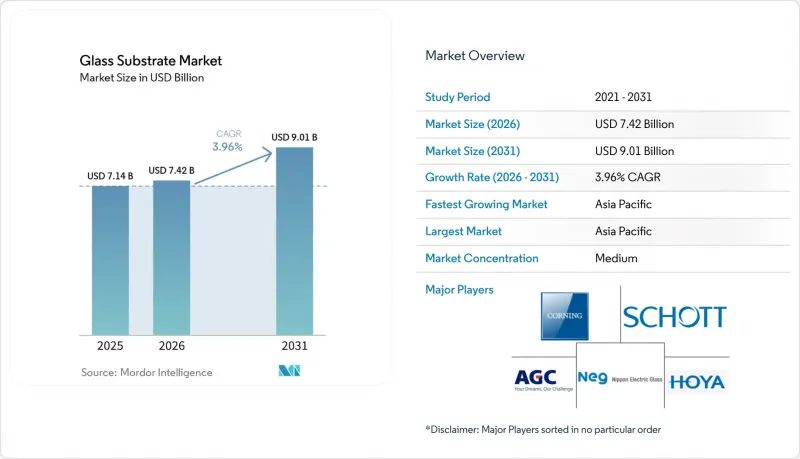

Glass Substrate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the glass substrate market size was valued at USD 7.14 billion in 2025 and is estimated to grow from USD 7.42 billion in 2026 to reach USD 9.01 billion by 2031, at a CAGR of 3.96% during the forecast period (2026-2031).

This report is Segmented by Material Type (Borosilicate, Silicon, and Other Types), Application (Display Panels, Semiconductors, and More), End-User Industry (Electronics, Automotive, Aerospace and Defense, Medical, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Glass Substrate Market Trends and Insights

Growing Usage of LCDs in Consumer Electronics

Persistent LCD volumes in mid-range smartphones, tablets, and monitors keep the glass substrates market firmly anchored in Asia-Pacific manufacturing hubs. Large-format gaming and professional monitors are now adopting thinner, lighter substrates to enable borderless designs that cut shipping weight and curb panel breakage. The mix shift toward higher value LCD panels favors suppliers capable of precision thinning and surface treatments alongside commodity-scale output. These dual capabilities strengthen incumbent positions for vertically integrated producers that can amortize R&D across multiple applications. Display OEM roadmaps also signal incremental glass demand from automotive infotainment retrofits, where existing LCD fabs redeploy capacity toward curved cockpit clusters.

Expansion of Semiconductor Fabrication Lines

The USD 150 billion wave of new fabs announced by Intel, Samsung, and TSMC through 2030 is reshaping the glass substrates market. Demand is ramping across three vectors: quartz photomask blanks for EUV patterning, glass-core substrates for 2.5D and 3D packages, and chemically inert inspection windows used in extreme-clean-room environments. Rapidus's demonstration of a 600 mm X 600 mm glass panel promises 10-fold chip yield relative to silicon interposers, highlighting the area-economy edge of rectangular glass panels over round wafers. Early design wins in this ecosystem lock suppliers into long qualification cycles, rewarding those who scale capacity in tandem with foundry outputs.

High Manufacturing and Capital Costs

Greenfield float or fusion-draw lines cost USD 200 million-USD 500 million, with melting furnaces consuming up to 40% of initial outlays. SCHOTT's EUR 40 million electric-melting retrofit at Mainz highlights the capex premium of decarbonization, yet integrated players deem it essential to hedge energy volatility. Specialty paths-ultra-thin glass, quartz blanks-stack extra investments in chemical strengthening, polishing, and Class 1 clean rooms, pushing fully loaded project costs above USD 300 million. This barrier consolidates the glass substrates market around incumbents capable of cross-subsidizing long paybacks with broad product portfolios.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Automotive and AR/VR Displays

- Emergence of Glass Core Substrates in Advanced Packaging

- Persistent Supply-Chain Volatility and Energy Price Spikes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Borosilicate glass accounted for 45.76% of the glass substrates market size in 2025 and continues to underpin TFT-LCD production due to its thermal stability and cost advantage. Its share growth is slowing as legacy LCD capacity pivots toward automotive and industrial displays, yet the sheer throughput of Gen 8.5 and Gen 10.5 fabs keeps borosilicate volumes high. Suppliers are adding precision thinning and surface-treatment lines to command better margins, particularly for curved infotainment and larger gaming monitors. Meanwhile, quartz substrates are projected to post a 4.41% CAGR through 2031 on the back of EUV lithography's relentless scaling below 3 nm. Near-zero CTE and sub-ppb metallic purity push quartz unit pricing multiples higher than borosilicate, insulating margins from commodity swings.

Quartz's rising demand transforms supply chains: HOYA and Shin-Etsu's synthetic-quartz duopoly now invests in additional CVD reactors, while semiconductor OEMs co-fund capacity to avoid EUV blank shortages. The glass substrates market, therefore, bifurcates into high-volume borosilicate workshops chasing cost efficiencies and low-volume quartz operations emphasizing defect-free quality. Both materials remain indispensable, but profit pools skew toward quartz and emerging glass-ceramic hybrids for foldables that blend flexibility with scratch resistance.

Geography Analysis

Asia-Pacific dominated the glass substrates market with a 48.82% share in 2025 and is projected to post the highest 4.19% CAGR through 2031. China's BOE, CSOT, and HKC run the bulk of global TFT-LCD capacity, generating massive demand for borosilicate glass. Japan maintains control of the synthetic-quartz supply for EUV mask blanks, while South Korea spearheads ultra-thin glass and foldable OLED innovations. Taiwan's foundry cluster consumes quartz blanks and glass carriers, with TSMC's expansion in Arizona and Kumamoto creating secondary hubs outside the region. India's Vedanta-AvanStrate investment signals an emerging domestic substrate base aimed at local smartphone and TV assembly.

North America market growth is buoyed by semiconductor packaging and automotive display projects rather than commodity LCD output. Intel's Ohio and Arizona fabs will validate panel-scale glass-core substrates, and Absolics' CHIPS Act-supported plant anchors the first U.S. manufacturing footprint in this field. Corning's New York and North Carolina sites supply Gorilla Glass, UTG, and precision optics to regional electronics and vehicle OEMs. Automotive makers in the United States, Canada, and Mexico are integrating windshield-wide HUDs into 2026-2027 models, intensifying demand for curved glass mirrors and holographic laminates.

The European glass substrates demand is anchored by significant consumption in Germany, France, and the United Kingdom. SCHOTT's electric-melting retrofit showcases Europe's decarbonization push, while its 2024 acquisition of quartz-glass specialist QSIL strengthens strategic exposure to EUV lithography. Automotive OEMs such as BMW and Mercedes-Benz deploy AR windshields that rely on ZEISS and Panasonic optics laminated in high-clarity glass. Elevated energy costs and tighter emission norms pressure commodity borosilicate margins, driving European producers toward high-margin specialty segments and energy-efficient melting technologies.

South America and the Middle East & Africa are witnessing a rising demand for glass substrates, mostly float-glass for construction and autoglass, with limited exposure to semiconductor or advanced display markets.

- AGC Inc.

- AvanStrate Inc.

- Corning Incorporated

- HOYA Corporation

- Irico Group New Energy Company Limited

- Kyocera Corporation

- Nippon Electric Glass Co., Ltd.

- Nitto Boseki Co., Ltd.

- Ohara Inc.

- Planoptik AG

- Saint-Gobain

- Samtec

- SCHOTT AG

- SHENZHEN LAIBAO HI-TECH CO., LTD

- TOPPAN Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing usage of LCDs in consumer electronics

- 4.2.2 Expansion of semiconductor fabrication lines

- 4.2.3 Rising demand for automotive and AR/VR displays

- 4.2.4 Growth of high-efficiency photovoltaic cells

- 4.2.5 Emergence of glass core substrates in advanced packaging

- 4.3 Market Restraints

- 4.3.1 High manufacturing and capital costs

- 4.3.2 Persistent supply-chain volatility and energy price spikes

- 4.3.3 Stringent environmental regulations on boron emissions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

- 4.6 Technological Snapshot

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Borosilicate

- 5.1.2 Silicon

- 5.1.3 Ceramic

- 5.1.4 Quartz

- 5.1.5 Other Types (Sapphire, Aluminosilicate, etc.)

- 5.2 By Application

- 5.2.1 Display Panels

- 5.2.2 Semiconductors

- 5.2.3 Solar Cells

- 5.2.4 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Electronics

- 5.3.2 Automotive

- 5.3.3 Aerospace and Defense

- 5.3.4 Medical

- 5.3.5 Solar Power

- 5.3.6 Other End-user Industries (Equipment Manufacturing, Telecommunication, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 South Korea

- 5.4.1.4 India

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 AvanStrate Inc.

- 6.4.3 Corning Incorporated

- 6.4.4 HOYA Corporation

- 6.4.5 Irico Group New Energy Company Limited

- 6.4.6 Kyocera Corporation

- 6.4.7 Nippon Electric Glass Co., Ltd.

- 6.4.8 Nitto Boseki Co., Ltd.

- 6.4.9 Ohara Inc.

- 6.4.10 Planoptik AG

- 6.4.11 Saint-Gobain

- 6.4.12 Samtec

- 6.4.13 SCHOTT AG

- 6.4.14 SHENZHEN LAIBAO HI-TECH CO., LTD

- 6.4.15 TOPPAN Holdings Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment