PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066582

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066582

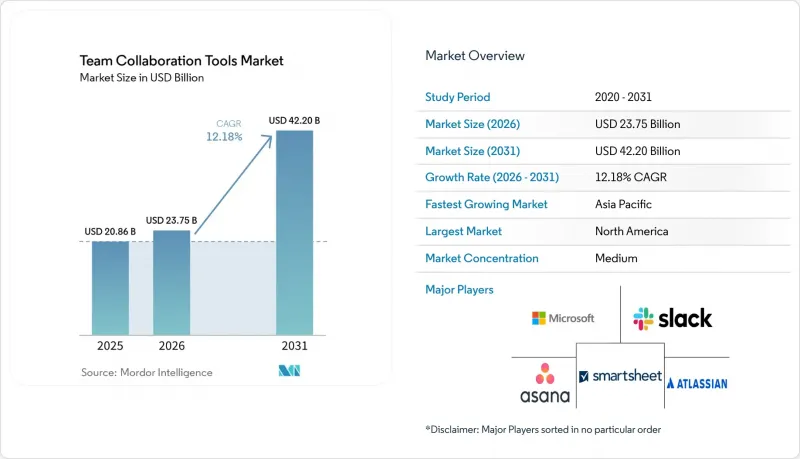

Team Collaboration Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the team collaboration tools market size is expected to increase from USD 20.86 billion in 2025 to USD 23.75 billion in 2026 and reach USD 42.2 billion by 2031, growing at a CAGR of 12.18% over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Organisation Size (SMEs, and Large Enterprises), Software Type (Communication and Coordination, Conferencing, Project Management, and Whiteboarding), Component (Software, and Services), End-User Industry (IT and Telecom, BFSI, Healthcare, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Team Collaboration Tools Market Trends and Insights

Rise Of Hybrid and Asynchronous Work Models

Enterprises are re-architecting digital workplaces so employees scattered across 8-12 time zones can collaborate without endless live meetings. Asynchronous features such as threaded discussions, video clips, and AI-generated summaries have become must-haves, cited by 68% of distributed teams as decisive in platform selection. Slack's Clips usage tripled between Q1 2025 and Q1 2026 as managers replaced daily stand-ups with short video updates that colleagues could watch on demand. Productivity studies show that 81% of workers in asynchronous environments feel more effective versus 52% in meeting-heavy settings. However, shifting to a documentation-centric culture raises training needs, which in turn fuels service revenue growth. Compliance frameworks like ISO 27001 now influence tool choice because asynchronous records must meet audit standards.

Accelerating SaaS Procurement Cycles Among SMBs

Modular pricing has shortened buying decisions from nine months to under ninety days for many SMEs, enabling side-by-side trials of multiple collaboration suites. A 2025 McKinsey study found firms that adopted mix-and-match SaaS stacks cut IT costs by 18-22%. Flexibility brings complexity: companies juggling more than ten apps report 30% higher employee frustration, sparking demand for integration hubs like Workato that consolidate notifications. The Team collaboration tools market therefore bifurcates, with SMEs valuing speed while large enterprises focus on governance.

Shadow-IT And Multi-Tool Sprawl Inflating CIO TCO

Unauthorized adoption of consumer apps inflates enterprise licensing, integration, and security costs by as much as 40%. On average, organizations run fourteen collaboration products but formally govern only six, leaving eight in a gray zone of inconsistent policy enforcement. Each extra platform consumes budget for API maintenance and user support, diverting funds from innovation. Vendors now offer curated marketplaces where employees can self-install pre-approved integrations, shifting emphasis to governance frameworks rather than outright blockage.

Other drivers and restraints analyzed in the detailed report include:

- Generative-AI Plug-ins Boosting Productivity Per User

- Growing Focus on Employee-Experience Platforms

- Rising Data-Sovereignty and Residency Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid solutions expanded at a 12.86% CAGR through 2031, the quickest among deployment types. While cloud still controlled 72.17% of the Team collaboration tools market share in 2025 thanks to low upfront costs, regulatory hurdles prompted banks and governments to keep select workloads on premises. Microsoft reported that hybrid configurations accounted for 34% of new Teams enterprise deals in 2026, up from 22% the year prior. This growing slice of Team collaboration tools market size illustrates how organizations balance sovereign data control with cloud-based AI features.

Demand for true data mobility is pushing vendors to invest in edge appliances and federated identity services that let meeting recordings live on local hardware while transcriptions process in the public cloud. Smaller providers struggle to fund such dual-stack engineering, widening the gap between hyperscale platforms and niche offerings. As more regions adopt data-localization statutes, hybrid will likely shift from exception to default.

SMEs held 58.58% of spending in 2025 and are projected to outpace large enterprises at a 12.96% CAGR. The Team collaboration tools market size for SMEs rises partly because feature-modular SaaS tiers eliminate capital expenditure barriers. Flexible month-to-month licensing lets small firms test three or four platforms concurrently, often combining Slack messaging with Asana tasks and Miro whiteboards.

Cost savings can be substantial McKinsey pegged IT spend reductions at up to 22% for modular adopters but tool sprawl erodes those gains if integration frameworks lag. Vendors courting SMEs therefore ship turnkey automation templates that require no coding. Large enterprises, by contrast, prioritize consolidation with suitelike products from Microsoft or Atlassian, accepting moderately slower innovation in return for single-vendor governance.

Geography Analysis

North America accounted for 39.29% of 2025 revenue. Adoption of AI add-ons such as Microsoft Copilot and Slack AI surpassed 40% among Fortune 500 firms, yet overall growth moderates to 11.8% CAGR as user penetration approaches saturation. Vendors focus on boosting average revenue per seat via premium AI and governance modules. Canada and Mexico grow a bit faster than the United States, but together still represent less than one-sixth of regional spend.

Asia-Pacific is the fastest-growing region at 13.22% CAGR. India's DPDP Act spurs local data-center builds, helping domestic vendor Zoho secure roughly one-fifth of the SME segment. China remains bifurcated between domestic suites like DingTalk and global tools operating in walled-off partitions compliant with PIPL. Japan's more modest 11.2% CAGR reflects cultural preference for in-person interactions, though low-code workflow builders from Cybozu are nudging older firms toward digital processes. Southeast Asian nations log nearly 14% growth as governments mandate digitalization.

Europe holds 24-26% of the Team collaboration tools market size and grows at 11.5% CAGR, heavily shaped by GDPR and DORA. Germany, the United Kingdom, and France contribute 60% of continental spend, prioritizing data-residency guarantees over price. Eastern European outsourcing hubs adopt collaboration suites quickly to manage cross-border developer teams. The Middle East and Africa combined maintain mid-12% growth, led by United Arab Emirates smart-city programs and South African financial-services digitization. South America trails slightly at near-12% CAGR, with Brazil commanding the lion's share.

- Microsoft Corporation

- Salesforce Inc. (Slack)

- Google LLC (Workspace)

- Atlassian Corporation PLC

- Zoom Video Communications Inc.

- Smartsheet Inc.

- Asana Inc.

- Cisco Systems Inc.

- Zoho Corporation Pvt. Ltd.

- Monday.com Ltd.

- Wrike Inc.

- TigerConnect Inc.

- Huddle (Ninian Solutions Ltd.)

- Notion Labs Inc.

- ClickUp Inc.

- Basecamp LLC

- Miro Corporation

- Airtable Inc.

- Symphony Communication Services LLC

- Cybozu Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise of Hybrid and Asynchronous Work Models

- 4.2.2 Accelerating SaaS Procurement Cycles Among SMBs

- 4.2.3 Generative-AI Plug-ins Boosting Productivity per User

- 4.2.4 Growing Focus on Employee-Experience (EX) Platforms

- 4.2.5 In-App Workflow Automation Reducing Context Switching

- 4.2.6 Collaboration Analytics Quantifying Knowledge-Worker ROI

- 4.3 Market Restraints

- 4.3.1 Shadow-IT and Multi-Tool Sprawl Inflating CIO TCO

- 4.3.2 Rising Data-Sovereignty and Residency Mandates

- 4.3.3 Vendor Lock-in Concerns with Hyperscale Ecosystems

- 4.3.4 Escalating Privacy Lawsuits over Meeting Transcripts and Recordings

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Generative-AI Integration Roadmap

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Organisation Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By Software Type

- 5.3.1 Communication and Coordination Software

- 5.3.2 Conferencing Software

- 5.3.3 Project and Task Management Suites

- 5.3.4 Whiteboarding and Ideation Platforms

- 5.4 By Component

- 5.4.1 Software

- 5.4.2 Services

- 5.5 By End-User Industry

- 5.5.1 Information Technology and Telecom

- 5.5.2 Banking, Financial Services and Insurance (BFSI)

- 5.5.3 Healthcare and Life-Sciences

- 5.5.4 Education

- 5.5.5 Retail and E-Commerce

- 5.5.6 Government and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South-East Asia

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Salesforce Inc. (Slack)

- 6.4.3 Google LLC (Workspace)

- 6.4.4 Atlassian Corporation PLC

- 6.4.5 Zoom Video Communications Inc.

- 6.4.6 Smartsheet Inc.

- 6.4.7 Asana Inc.

- 6.4.8 Cisco Systems Inc.

- 6.4.9 Zoho Corporation Pvt. Ltd.

- 6.4.10 Monday.com Ltd.

- 6.4.11 Wrike Inc.

- 6.4.12 TigerConnect Inc.

- 6.4.13 Huddle (Ninian Solutions Ltd.)

- 6.4.14 Notion Labs Inc.

- 6.4.15 ClickUp Inc.

- 6.4.16 Basecamp LLC

- 6.4.17 Miro Corporation

- 6.4.18 Airtable Inc.

- 6.4.19 Symphony Communication Services LLC

- 6.4.20 Cybozu Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis