PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066585

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066585

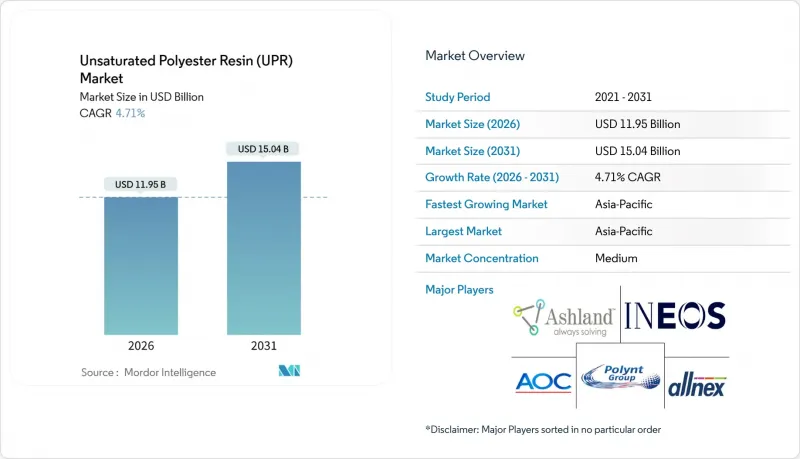

Unsaturated Polyester Resin (UPR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the unsaturated polyester resin market size is estimated at USD 11.95 billion in 2026, and is expected to reach USD 15.04 billion by 2031, at a CAGR of 4.71% during the forecast period (2026-2031).

This report is Segmented by Raw Material (Maleic Anhydride, Phthalic Anhydride, and More), Product Type (Ortho-Resins, Isoresins, DCPD, and Other Types), Form (Liquid and Powder), End-Use Industry (Building and Construction, Chemical, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Unsaturated Polyester Resin (UPR) Market Trends and Insights

Surging Adoption in Wind-Turbine Blades

Offshore installations lifted global blade-composite demand by 22% in 2025 as average rotor lengths moved beyond 85 meters in the North Sea andthe Taiwan Strait in the unsaturated polyester resin market [1]. Unsaturated polyester resin remains the default matrix for spar-cap and shell laminates because vacuum-infusion delivers attractive cost-per-kilowatt figures versus epoxy systems. European circular-economy mandates now require end-of-life blade recovery pathways by 2030, which is prompting trials of UPR blends incorporating recycled-PET polyols that can cut decommissioning logistics costs by up to 15%. China's National Energy Administration allocated USD 18 billion for new offshore capacity in 2025, confirming Asia-Pacific as the primary growth engine through 2031. Blade makers therefore seek resins with documented recyclability, low exotherm, and fatigue durability suitable for 20-year service intervals.

Growth of Automotive and Transportation Sectors

Automotive manufacturers processed roughly 1.8 million t of composite resins in 2025 in the unsaturated polyester resin market, and 40% of that volume relied on unsaturated polyester resin-based sheet-molding-compound for underbody shields, battery trays, and Class-A body panels. Electric-vehicle platforms need electromagnetic-interference shielding and flame retardancy while maintaining low mass; isoresin and dicyclopentadiene grades therefore gain share. General Motors and Stellantis lifted SMC press capacity by 30% during 2025 to support curb-weight reduction targets that improve driving range by 10-15%. Closed-mold presses eliminate styrene emissions and already comply with California rules that limit volatile-organic compounds to 50 g L-1 for composite parts. Supply contracts increasingly stipulate UL 94 V-0 flame-retardant performance and dimensional stability from -40 °C to 120 °C across a decade of service.

Maleic Anhydride Price Volatility

Spot prices swung between USD 1,400 and USD 2,100 t-1 in 2025 in the unsaturated polyester resin market as crude-oil and benzene disruptions rippled through the value chain. Resin makers without long-term supply contracts faced margin compression of 200-300 basis points, prompting vertical-integration moves such as Polynt's 50,000 t y-1 maleic-anhydride acquisition in Italy. China controls 55% of global maleic-anhydride capacity, exposing Western buyers to freight and tariff risks under Section 301 measures in the United States. Alternative bio-based pathways remain pilot-scale and carry 40-60% cost premiums, limiting broad adoption.

Other drivers and restraints analyzed in the detailed report include:

- Construction and Infrastructure Boom in Emerging Asia

- OEM Shift to Closed-Mold SMC/BMC for E-Mobility

- Environmental and Regulatory Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Maleic Anhydride held 51.26% of 2025 revenue within the unsaturated polyester resin market share, underscoring its central role in ortho-phthalic and iso-phthalic backbones that balance cost and mechanical strength. Propylene Glycol is expanding at a 5.70% CAGR through 2031, driven by processors who seek lower viscosity and better wet-out during vacuum-infusion of wind-turbine spar caps. Phthalic Anhydride continues to serve general-purpose ortho grades, while Styrene Monomer remains indispensable as a cross-linking diluent, despite pressure for recovery systems that cap emissions.

Propylene Glycol growth mirrors wider substitution toward neopentyl glycol and dipropylene glycol co-reactants that enhance hydrolytic stability in marine and chemical-processing equipment. China expanded propylene-glycol capacity by 18% in 2025 on the back of coal-to-olefin routes, reducing delivered costs within Asia. OEM audits now require ISO 9001 certification and batch traceability, reinforcing quality expectations for raw-material suppliers targeting aerospace and medical components.

Ortho-resins captured 53.31% of 2025 revenue in the unsaturated polyester resin market because broad formulation latitude keeps prices competitive across construction and sanitary-ware uses. Isoresins, however, are projected to climb 6.56% CAGR through 2031, propelled by marine vessels, desalination plants, and chemical-processing equipment that demand elevated temperature and corrosion resistance. Dicyclopentadiene resin occupies a niche in wind-turbine nacelles and large storage tanks, where low exotherm enables thick-section casting without cracking.

Isoresin uptake aligns with the expansion of liquefied-natural-gas terminals, offshore production platforms, and industrial wastewater facilities that specify fiberglass-reinforced equipment meeting EN 13121 flexural-strength thresholds. Suppliers such as AOC and Ashland launched iso-NPG grades in 2025 that provide corrosion resistance while processing on unheated molds, enabling adoption by fabricators with limited capital investment.

Geography Analysis

Asia-Pacific led the unsaturated polyester resin market with a delivered 43.45% of global revenue in 2025 and is forecast to grow at a 5.78% CAGR to 2031, driven by Chinese infrastructure outlays, India's housing boom, and Southeast Asian industrial expansion. China allocated USD 800 billion in 2025 for urban rail, water systems, and renewable energy installations that consume corrosion-resistant piping and blade-grade composites. India's production-linked incentives attracted USD 30 billion in foreign investment, spurring component demand in electric two-wheelers, appliances, and telecom equipment. Regulatory frameworks in the region remain fragmented, yet local compounders adept at navigating GB and BIS standards win share against multinational incumbents.

North America's share is anchored by United States demand in automotive composites, wind-energy blades, and chemical-processing equipment. The Inflation Reduction Act unlocked USD 15 billion in composite capital expenditure during 2025 across resin compounding, SMC presses, and blade-molding plants. California Air Resources Board rules speed the migration to closed-mold and low-styrene resin systems, opening premium segments for suppliers with ultra-low emission portfolios. Mexico's vehicle assemblies exceeded 4 million units in 2025, and local Tier-1s expanded SMC capacity to serve North American and European electric-vehicle programs.

Europe focuses on high-value marine, automotive, and wind-energy uses in the unsaturated polyester resin market. Germany's carmakers consumed 180,000 t of composite resins in 2025 as Volkswagen, BMW, and Mercedes-Benz integrated SMC battery enclosures and structural components. The Circular Economy Action Plan and stricter Industrial Emissions rules push suppliers toward recyclable, bio-based chemistries. South America and Middle East and Africa remain smaller but fast-growing in the unsaturated polyester resin market, buoyed by Brazilian sanitation investments, Saudi chemical diversification, and South African mining infrastructure, each favoring fiberglass-reinforced equipment that lowers total life-cycle costs versus metals.

- Allnex GmbH

- AOC

- Ashland

- BASF SE

- Covestro AG

- Crystic Resins India Pvt. Ltd.

- DIC Corporation

- INEOS

- Interplastic Corporation

- Polynt S.p.A.

- Scott Bader Company Ltd

- SWANCOR

- U-Pica Company

- Xinyang Technology Group

- Zhangzhou Yabang Chemical Co., Ltd.

- Zhejiang Tianhe Resin Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption in Wind-Turbine Blades

- 4.2.2 Growth of Automotive and Transportation Sectors

- 4.2.3 Construction And Infrastructure Boom in Emerging Asia

- 4.2.4 EU REACH Pressure for Low-Styrene Resins

- 4.2.5 OEM Shift to Closed-Mold SMC/BMC for E-Mobility

- 4.3 Market Restraints

- 4.3.1 Maleic Anhydride Price Volatility

- 4.3.2 Environmental and Regulatory Challenges

- 4.3.3 Rising LCA Scrutiny Favouring Bio-Epoxy Systems

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Raw Material

- 5.1.1 Maleic Anhydride

- 5.1.2 Phthalic Anhydride

- 5.1.3 Propylene Glycol

- 5.1.4 Styrene Monomer

- 5.1.5 Others (Additives, Initiators)

- 5.2 By Product Type

- 5.2.1 Ortho-resins

- 5.2.2 Isoresins

- 5.2.3 Dicyclopentadiene (DCPD)

- 5.2.4 Other Types

- 5.3 By Form

- 5.3.1 Liquid

- 5.3.2 Powder

- 5.4 By End-use Industry

- 5.4.1 Building and Construction

- 5.4.2 Chemical

- 5.4.3 Electrical and Electronics

- 5.4.4 Paints and Coatings

- 5.4.5 Transportation

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Allnex GmbH

- 6.4.2 AOC

- 6.4.3 Ashland

- 6.4.4 BASF SE

- 6.4.5 Covestro AG

- 6.4.6 Crystic Resins India Pvt. Ltd.

- 6.4.7 DIC Corporation

- 6.4.8 INEOS

- 6.4.9 Interplastic Corporation

- 6.4.10 Polynt S.p.A.

- 6.4.11 Scott Bader Company Ltd

- 6.4.12 SWANCOR

- 6.4.13 U-Pica Company

- 6.4.14 Xinyang Technology Group

- 6.4.15 Zhangzhou Yabang Chemical Co., Ltd.

- 6.4.16 Zhejiang Tianhe Resin Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Emergence of Bio-based Unsaturated Polyester Resins