PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066586

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066586

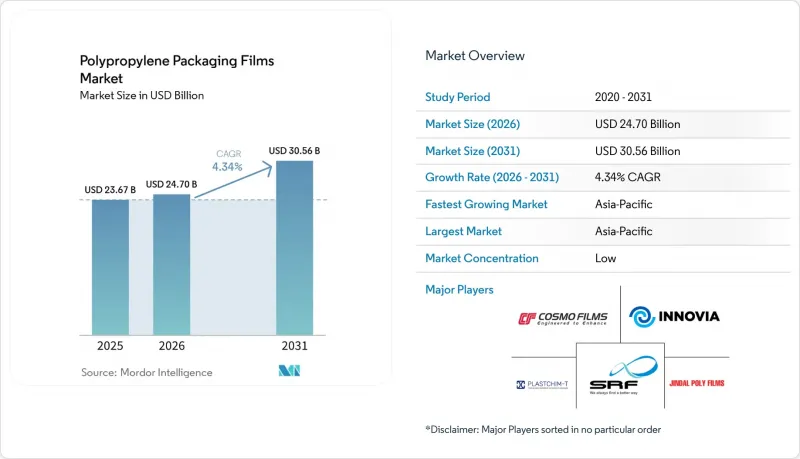

Polypropylene Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, polypropylene packaging films market size in 2026 is estimated at USD 24.7 billion, growing from 2025 value of USD 23.67 billion with 2031 projections showing USD 30.56 billion, growing at 4.34% CAGR over 2026-2031.

This report is Segmented by Film Type (Biaxially Oriented Polypropylene (BOPP) Film and More), Packaging Format (Wraps and Over-Wraps, Labels and Pressure-Sensitive Tapes, Bags and Pouches and More), End-Use Industry ( Food, Beverage, Pharmaceutical and Healthcare and More) and Geography (North America, Europe, Asia-Pacific, South America and Middle East and Africa)

Global Polypropylene Packaging Films Market Trends and Insights

Sustainable Shift from Rigid to Flexible Formats

Reducing package weight by as much as 75% versus rigid plastics, flexible polypropylene films help brand owners curb freight emissions and material costs. Klockner Pentaplast's kp FlexiFlow range delivers recyclable flow-wrap structures containing more than 93% polypropylene, illustrating performance parity with legacy formats while offering circularity. Multinationals adopt refill pouches for home-care and personal-care goods, lowering source-reduction fees under Extended Producer Responsibility rules. Film producers leverage downgauging and higher post-consumer-recycled resin loads without sacrificing puncture strength, solidifying polypropylene's role as a lightweight alternative across e-commerce and retail channels.

Brand Owner Demand for Mono-Material Recycle-Ready Laminates

DNP's polypropylene-based mono-material laminates meet CEFLEX design guidelines, allowing high-speed form-fill-seal operations while entering existing recycling streams. European Packaging and Packaging Waste Regulation targets accelerate adoption, prompting Saica Flex to develop 100% recyclable solutions that incorporate 5% certified post-consumer content. Barrier-coating advances such as ORMOCER and new acrylic chemistries achieve oxygen transmission rates below 0.1 cm3/m2*day*bar, aligning shelf-life demands with recyclability. Brand owners accept small cost premiums to reach 2030 circularity pledges, spurring rapid substitution of mixed-material foil laminates.

Volatility in Propylene and Naphtha Feedstock Prices

Polymer-grade propylene rose 4-5 cents / lb in early 2025 after refinery closures tightened supply, squeezing converter margins. South Asian raffia grades climbed to USD 970-990 / t, reflecting geopolitical pressures on crude benchmarks. Film makers struggle to pass through surcharges in commoditized snack wraps, prompting some regional packers to trial less volatile polyethylene films. Persistent uncertainty complicates annual supply tenders and deters capital spending on new orientation lines.

Other drivers and restraints analyzed in the detailed report include:

- Retort-Grade CPP Replacing Multilayer High-Barrier Structures

- E-commerce Boom Driving High-Clarity Over-Wrap Films

- Growing PET and PE Mono-Material Barrier Film Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

BOPP led the polypropylene packaging films market with 65.58% share in 2025, reflecting broad adoption in snack, bakery, and tobacco over-wraps. Coated BOPP grades with acrylic or PVDC layers extend shelf life in confectionery while retaining low density advantages. Cosmo Films operates 196,000 t / y capacity that supports global distribution, reinforcing BOPP supply security. Volume also flows from new Southeast Asian lines that lower delivered costs into price-sensitive African markets.

CPP posted the quickest 6.87% CAGR forecast, propelled by retort pouches and metallized snack wraps. Mitsui's RXC-22 cast film seals at lower temperatures, trimming energy use on high-speed form-fill-seal machinery. Specialty CPP competes in medical packaging where clarity, chemical resistance, and gamma sterilization tolerance matter. The polypropylene packaging films market size for CPP is set to expand alongside demand for mono-material pouch laminates that facilitate recycling streams. Other niche grades, including breathable microporous films for produce, carve out incremental revenue by solving specific moisture and gas-exchange needs.

Geography Analysis

Asia-Pacific controlled 43.71% of global revenue in 2025 and is poised for a 6.23% CAGR through 2031. China's forecast 2.6 million-ton polypropylene export pool underpins ample film resin supply. Indonesia's national demand of 5.2 million t outstrips domestic capacity of 2.4 million t, necessitating imports even as anti-dumping duties target regional suppliers. Vietnam's Long Son cracker restart in late 2025 will add 400,000 t / y of polypropylene, narrowing deficits and supporting regional downstream processors. Cost-competitive labor and an expanding middle class sustain robust demand across FMCG, pharmaceutical, and electronics supply chains.

Europe remains a technology leader despite modest volume growth. Extended Producer Responsibility fees now vary by recyclability, nudging brands toward mono-material polypropylene solutions. The forthcoming Carbon Border Adjustment Mechanism may impose reporting obligations and implicit carbon costs on imported films, potentially eroding Southeast Asian price advantages. European converters invest in advanced de-inking and solvent-based recycling plants to close material loops, while Ineos ramps recycled-plastic output at its French cracker to comply with EU PPWR mandates.

North America benefits from high food-safety standards and deep e-commerce penetration but battles feedstock-linked cost swings. PureCycle's Ohio plant now produces 107 million lb / y of ultra-pure recycled polypropylene, supplying converters that need FDA-compliant recyclate. US polypropylene imports totaled USD 789.2 million in 2021, revealing reliance on overseas monomer when domestic crackers prioritize polyethylene derivatives. Investment in chemical recycling pilot lines accelerates as state legislation sets recycled-content thresholds for flexible packaging.

- Amcor Plc

- Jindal Poly Films Ltd

- Innovia Films

- Cosmo Films Ltd

- Taghleef Industries LLC

- UFlex Ltd

- Polyplex Corporation Ltd

- SRF Ltd

- Plastchim-T

- Toray Plastics (America) Inc.

- ProAmpac LLC

- Inteplast Group

- Oben Holding Group

- Profol GmbH

- Treofan GmbH

- Vibac Group

- Chiripal Poly Films

- Polinas

- Stenta Films

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainable shift from rigid to flexible formats

- 4.2.2 Brand owner demand for mono-material recycle-ready laminates

- 4.2.3 Retort-grade CPP replacing multilayer high-barrier structures

- 4.2.4 E-commerce boom driving high-clarity over-wrap films

- 4.2.5 Rapid capacity additions in Southeast Asia lowering film prices

- 4.2.6 Chemical-recycling derived PP resin commercialization

- 4.3 Market Restraints

- 4.3.1 Volatility in propylene and naphtha feedstock prices

- 4.3.2 Growing PET and PE mono-material barrier film substitutes

- 4.3.3 Trade-flow disruptions from carbon-border-adjustment tariffs

- 4.3.4 Extended Producer Responsibility (EPR) compliance costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Film Type

- 5.1.1 Biaxially Oriented Polypropylene (BOPP) Film

- 5.1.1.1 Coated BOPP (PVDC, Acrylic, EVOH)

- 5.1.1.2 Uncoated BOPP

- 5.1.2 Chlorinated Polypropylene (CPP) Film

- 5.1.2.1 General-purpose CPP

- 5.1.2.2 Retort-grade CPP

- 5.1.2.3 Metalized CPP

- 5.1.3 Other Polypropylene (PP) Packaging Films

- 5.1.1 Biaxially Oriented Polypropylene (BOPP) Film

- 5.2 By Packaging Format

- 5.2.1 Wraps and Over-wraps

- 5.2.2 Labels and Pressure-sensitive Tapes

- 5.2.3 Bags and Pouches

- 5.2.4 Lidding and Flow-wrap Films

- 5.2.5 Blister and Strip Packs

- 5.3 By End-use Industry

- 5.3.1 Food

- 5.3.1.1 Bakery and Confectionery

- 5.3.1.2 Snacks and Breakfast Cereals

- 5.3.1.3 Fresh Produce

- 5.3.1.4 Meat, Poultry and Seafood

- 5.3.1.5 Dairy Products

- 5.3.2 Beverage

- 5.3.2.1 Non-Alcoholic

- 5.3.2.1.1 Bottled Water

- 5.3.2.1.2 Carbonated Drinks

- 5.3.2.1.3 Juices

- 5.3.2.1.4 Other Non-Alcoholic Beverages

- 5.3.2.2 Alcoholic

- 5.3.2.2.1 Beer

- 5.3.2.2.2 Spirits

- 5.3.2.2.3 Other Alcoholic Beverages

- 5.3.2.1 Non-Alcoholic

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Industrial

- 5.3.6 Other End-use Industry

- 5.3.1 Food

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 Middle East

- 5.4.4.1.1 Saudi Arabia

- 5.4.4.1.2 United Arab Emirates

- 5.4.4.1.3 Turkey

- 5.4.4.1.4 Rest of Middle East

- 5.4.4.2 Africa

- 5.4.4.2.1 South Africa

- 5.4.4.2.2 Kenya

- 5.4.4.2.3 Rest of Africa

- 5.4.4.1 Middle East

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor Plc

- 6.4.2 Jindal Poly Films Ltd

- 6.4.3 Innovia Films

- 6.4.4 Cosmo Films Ltd

- 6.4.5 Taghleef Industries LLC

- 6.4.6 UFlex Ltd

- 6.4.7 Polyplex Corporation Ltd

- 6.4.8 SRF Ltd

- 6.4.9 Plastchim-T

- 6.4.10 Toray Plastics (America) Inc.

- 6.4.11 ProAmpac LLC

- 6.4.12 Inteplast Group

- 6.4.13 Oben Holding Group

- 6.4.14 Profol GmbH

- 6.4.15 Treofan GmbH

- 6.4.16 Vibac Group

- 6.4.17 Chiripal Poly Films

- 6.4.18 Polinas

- 6.4.19 Stenta Films

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment