PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066596

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066596

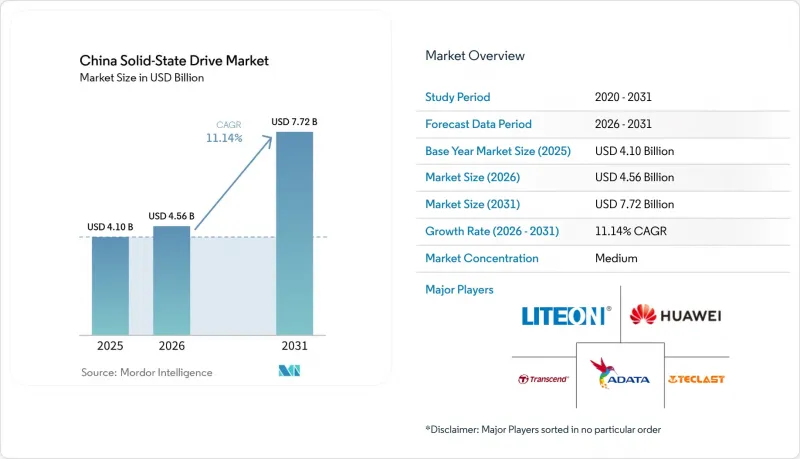

China Solid-State Drive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china solid-state drive market size is expected to grow from USD 4.10 billion in 2025 to USD 4.56 billion in 2026 and is forecast to reach USD 7.72 billion by 2031 at 11.14% CAGR over 2026-2031.

This report is Segmented by Interface (Serial ATA (SATA), PCI Express (PCIe/NVMe) and More), Form Factor (2. 5-Inch Drives. M. 2 Modules, and More), NAND Technology (SLC / MLC, TLC, and More), Application (Enterprise, Client), End-User Industry (Cloud Service Providers, Hyperscale and Colocation Data Centres, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Solid-State Drive Market Trends and Insights

Data-centre Expansion for AI Workloads

China's AI computing footprint is on track to exceed 300 exaflops by 2025, lifting SSD capacity requirements for model training servers from 30 TB today to 100 TB by decade-end. Kingsoft Cloud's KS3 Extreme Speed deployment, built on Solidigm QLC devices, already sustains 1 Tbps per petabyte-100X faster than comparable HDD arrays. Inference workloads are expanding even faster, with storage demand forecast to reach 447 exabytes by 2030. Cloud providers are switching to domestically packaged PCIe 5.0 NVMe SSDs to secure supply amid export controls. As a result, the China solid-state drive market enjoys a direct volume lift from every incremental rack of AI servers commissioned.

Shift from HDD to SSD in Consumer Devices

Consumer adoption of SSD-equipped laptops and desktops is accelerating as content-creation workloads move to 4K and 8K formats. Samsung's Xi'an plant rebounded to 70% utilization in 2024, stabilizing local NAND supply for smartphone OEMs. Domestic player UNIS now ships PCIe 5.0 drives at 14.9 GB/s, narrowing the performance gap with international alternatives while offering cost relief to channel partners. Though pandemic-era PC weakness tempered retail pricing, controlled production schedules signal firmer conditions in late 2025, sustaining the China solid-state drive market's consumer channel.

NAND Price-cycle Volatility

Spot prices swung sharply in 2024 as weak laptop demand met elevated fab utilization at Kioxia and Western Digital. Chinese tier-2 SSD brands faced squeezed margins, delaying controller upgrades and tightening promotional budgets. Forward contracts with YMTC are emerging as a hedge, but inventory misalignment can still hinder near-term sell-in volumes across the China solid-state drive market.

Other drivers and restraints analyzed in the detailed report include:

- East-Data-West-Compute" Government Build-out

- Localization of NAND Supply Chain

- Export-control Limits on Advanced Tools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PCIe/NVMe devices accounted for 61.35% of the China solid-state drive market size in 2025 and are on pace for a 14.32% CAGR, propelled by AI clusters that demand low-latency throughput. Enterprise buyers favour PCIe 4.0 and 5.0 lanes to cut training time on transformer models, lifting blended ASPs for domestic suppliers. SATA maintains a toehold in entry-level notebooks, but its share slides each quarter as consumers migrate to PCIe-based laptops. SAS continues in legacy mission-critical arrays where dual-port reliability trumps raw speed. Interface upgrades therefore remain a centerpiece of product differentiation across the China solid-state drive market.

Second-generation PCIe 5.0 controllers from Innogrit and Maxio add co-processing blocks for on-drive AI caching. As ODMs qualify these chips at cloud scale, the China solid-state drive industry unlocks fresh performance tiers without sacrificing power budgets. PCIe 6.0 roadmaps promise double-digit efficiency gains, aligning with the national goal of curbing data-center emissions. These advances reinforce China's ambition to climb the storage value chain while enlarging export potential for indigenous IP blocks.

M.2 modules held 47.20% of the China solid-state drive market share in 2025, favoured by OEMs for thin-and-light designs. Yet the U.2/E1.S category is forecast to grow 15.55% annually through 2031 as hyperscalers prioritize serviceability and airflow in AI racks. E1.S drives support 25 W envelopes, easing thermal throttling in PCIe 5.0 deployments. Their hot-swap convenience accelerates failure recovery, a key metric in cloud SLAs.

Converters from 2.5-inch bays to EDSFF trays are underway at Alibaba's Zhangbei campus, signalling a migration path for brownfield sites. Meanwhile, add-in-card SSDs retain a niche in specialized accelerator nodes where bandwidth saturation overrides density concerns. Collectively, the form-factor shift exemplifies how rack-level design choices ripple across the China solid-state drive market supply chain.

List of Companies Covered in this Report:

- Samsung Electronics Co., Ltd.

- Yangtze Memory Technologies Co., Ltd. (YMTC)

- Western Digital Corporation

- Kingston Technology Company, Inc.

- SK Hynix Inc.

- Huawei Technologies Co., Ltd.

- ADATA Technology Co., Ltd.

- Transcend Information Inc.

- Lenovo Group Limited

- Memblaze Technology Co., Ltd.

- Shenzhen Longsys Electronics Co., Ltd.

- Dapu Microelectronics Co., Ltd.

- Kimtigo Technology Co., Ltd.

- BIWIN Storage Technology Co., Ltd.

- Kioxia Holdings Corporation

- Micron Technology Inc.

- Intel Corporation (Solidigm)

- Seagate Technology Holdings plc

- LITE-ON Technology Corporation

- Maxiotek Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Data-centre expansion for AI workloads

- 4.2.2 Shift from HDD to SSD in consumer devices

- 4.2.3 East-Data-West-Compute government build-out

- 4.2.4 Localization of NAND supply chain

- 4.2.5 Edge and in-storage processing for IIoT

- 4.3 Market Restraints

- 4.3.1 NAND price-cycle volatility

- 4.3.2 Export-control limits on advanced tools

- 4.3.3 Power-supply caps for hyperscale DCs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Interface

- 5.1.1 Serial ATA (SATA)

- 5.1.2 PCI Express (PCIe/NVMe)

- 5.1.3 Serial-Attached SCSI (SAS)

- 5.1.4 USB/Other Embedded

- 5.2 By Form Factor

- 5.2.1 2.5-inch Drives

- 5.2.2 M.2 Modules

- 5.2.3 U.2 / E1.S

- 5.2.4 Add-in Cards

- 5.3 By NAND Technology

- 5.3.1 SLC / MLC

- 5.3.2 TLC

- 5.3.3 QLC

- 5.3.4 PLC (Prototype)

- 5.4 By Application

- 5.4.1 Enterprise

- 5.4.2 Client

- 5.5 By End-User Industry

- 5.5.1 Cloud Service Providers

- 5.5.2 Hyperscale & Colocation Data Centres

- 5.5.3 Consumer Electronics OEMs

- 5.5.4 Industrial & Manufacturing

- 5.5.5 Automotive & Transportation

- 5.5.6 Aerospace & Defence

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 Yangtze Memory Technologies Co., Ltd. (YMTC)

- 6.4.3 Western Digital Corporation

- 6.4.4 Kingston Technology Company, Inc.

- 6.4.5 SK Hynix Inc.

- 6.4.6 Huawei Technologies Co., Ltd.

- 6.4.7 ADATA Technology Co., Ltd.

- 6.4.8 Transcend Information Inc.

- 6.4.9 Lenovo Group Limited

- 6.4.10 Memblaze Technology Co., Ltd.

- 6.4.11 Shenzhen Longsys Electronics Co., Ltd.

- 6.4.12 Dapu Microelectronics Co., Ltd.

- 6.4.13 Kimtigo Technology Co., Ltd.

- 6.4.14 BIWIN Storage Technology Co., Ltd.

- 6.4.15 Kioxia Holdings Corporation

- 6.4.16 Micron Technology Inc.

- 6.4.17 Intel Corporation (Solidigm)

- 6.4.18 Seagate Technology Holdings plc

- 6.4.19 LITE-ON Technology Corporation

- 6.4.20 Maxiotek Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis