PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066603

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066603

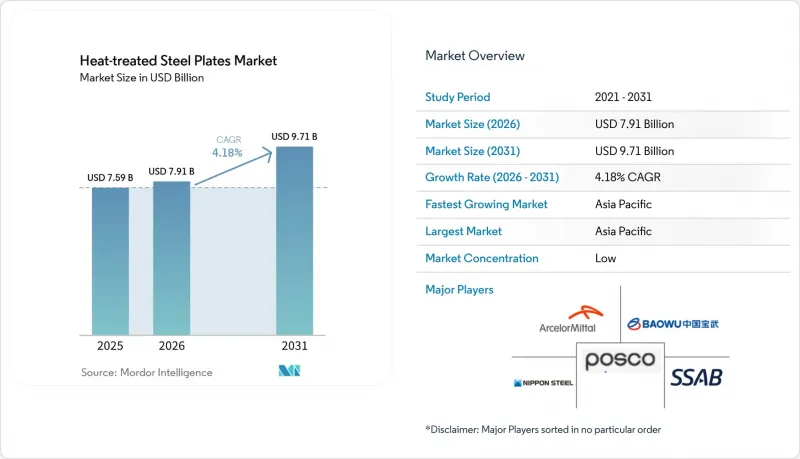

Heat-treated Steel Plates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the heat-treated steel plates market size is expected to grow from USD 7.59 billion in 2025 to USD 7.91 billion in 2026 and is forecast to reach USD 9.71 billion by 2031 at 4.18% CAGR over 2026-2031.

This report is Segmented by Steel Type (Carbon Steel, Alloy Steel, and Stainless Steel), Heat-Treatment Type (Annealing, Tempering, and More), End-Use Sector (Automotive and Heavy Machinery, Building and Construction, and More), and Geography (North America, South America, Europe, Middle East and Africa, Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Global Heat-treated Steel Plates Market Trends and Insights

Offshore-Wind Monopile Foundations Driving Demand

Monopile diameters have climbed to 11 m and wall thicknesses to 150 mm for 15-MW turbines, pushing demand for normalized or TMCP plate that meets DNV fracture-toughness rules. Taiwan's China Steel Corporation secured a 5-year order for 180,000 tons of S355G10+N plate in 2025, specifying 100 J Charpy toughness at -20 °C to mitigate typhoon-induced brittle fracture. Dillinger and Orsted agreed in 2024 to co-develop 12-m monopiles using quenched-and-tempered S690QL, reducing steel weight per MW by 18% and cutting installation costs. The Global Wind Energy Council foresees 110 GW of new offshore capacity by 2030, equal to about 8 million tons of plate if monopiles keep a 65% share. Each GW of offshore wind consumes an estimated 70,000 tons of heavy plate, underlining the sector's pull on heat-treatment capacity.

Abrasion-Resistant Plates Adopted in Autonomous Mining Truck Bodies

Autonomous haul trucks run 24 h per day, intensifying liner wear and raising demand for 500-Brinell quenched plate that stretches replacement cycles from 8,000 h to 14,000 h. SSAB's Hardox 500 Tuf, launched in 2025, delivers 45-J Charpy toughness, avoiding crack propagation when 220-t payloads strike the bed. JFE's EVERHARD 450 debuted in 2024 with phosphorus micro-alloying that cuts quenching distortion and lets users laser-cut without preheating. Austin Engineering reported a 32% jump in autonomous-fleet orders in 2025, with abrasion-resistant plate making up 68% of material spend. Rio Tinto's Pilbara fleet of 220 Komatsu 930E trucks switched to Hardox liners and reduced maintenance downtime by 22%.

Composites Replacing Wear Plate in Next-Generation Earth-Moving Equipment

Ultra-high-molecular-weight polyethylene liners bonded to basalt fiber captured 18% of haul-truck bed retrofits in 2025, lowering weight by 40% and eliminating weld spatter that seeds fatigue cracks. Caterpillar's 794 AC truck, launched in 2024, offers composite beds rated to 400-Brinell equivalent abrasion resistance and extends life to 16,000 h. Komatsu introduced a carbon-fiber reinforced bucket edge in 2025 that trims tip weight by 35% and cuts fuel burn by 2.1%. Volvo Construction Equipment disclosed that composite wear parts climbed to 12% of its articulated-hauler material spend in 2025, up from 4% in 2023. Bruce Rock Engineering demonstrated a USD 31,000 three-year savings per truck when switching to UHMWPE liners, accelerating adoption in cost-focused mines.

Other drivers and restraints analyzed in the detailed report include:

- Seismic-Resilient Normalized Plate Mandated by New Building Codes

- Duplex Stainless Plates for Green-Hydrogen Electrolyzer Pressure Vessels

- Energy-Price Volatility Reducing Furnace Utilization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The carbon steel accounted for 45.58% of the heat-treated steel plates market share in 2025, while alloy steel is forecast to expand at a 5.05% CAGR to 2031 as duplex stainless and martensitic grades penetrate electrolyzer vessels and subsea lines. Duplex stainless, notably EN 1.4462, covered about 8% of alloy tonnage in 2025, propelled by EU green-hydrogen projects. Stainless plate stays niche but essential in cryogenic and pharmaceutical uses, commanding price premiums that offset lower volume.

Cost differentials explain carbon steel's resilience-S355 normalized sells near USD 650/ton, versus duplex plate at roughly USD 2,400/ton. Even so, alloy formulations gain ground through innovations such as ArcelorMittal's Usibor 2000 press-hardening steel, which enables 2,000-MPa tensile strength for EV battery enclosures, and POSCO's PosMAC, which offers tenfold marine corrosion resistance relative to galvanized alternatives. Nippon Steel's NSGP1 normalized alloy meets -60 °C Charpy toughness for Arctic offshore rigs, further widening the addressable field for high-specification alloy plates.

Geography Analysis

Asia-Pacific held 52.95% of global revenue in 2025 and is forecast to grow at 5.74% through 2031, driven by Chinese wind-turbine supply chains, India's infrastructure pipeline, and Southeast Asian shipbuilding. China produced around 580 million tons of crude steel in 2025, with heat-treated variants accounting for close to 1.8%, indicating ample headroom for value-added migration. India's National Infrastructure Pipeline, worth INR 111 trillion (USD 1.3 trillion), is triggering 2.2 million tons of fresh plate capacity from JSW and Tata.

Europe trails in share but leads on margin-rich duplex output. H2 Green Steel's Boden mill, coming online in 2026, will supply 500,000 tons of fossil-free plate annually, aiming at users willing to pay EUR 50-80/ton green premiums. Germany's thyssenkrupp is co-developing hydrogen DRI, and UK offshore wind projects such as Dogger Bank are set to consume 1.2 million tons of normalized and TMCP plate from 2026 to 2031.

North America combines seismic mandates and LNG growth. Nucor's new normalizing line adds 300,000 tons of capacity for East Coast builders and Gulf Coast energy plants. The Middle East pivots on Saudi Arabia's NEOM, desalination, and petrochemical projects, anticipating a 6.2% annual steel-consumption rise to 2031. South America, led by Brazil and Argentina, benefits from lithium mining and farm-equipment production, with POSCO building a lithium-hydroxide plant requiring duplex pressure vessels.

- ArcelorMittal

- Baosteel Co.,Ltd.

- China Ansteel Group Corporation Limited

- China BaoWu Steel Group Corporation Limited

- Dillinger Hutte Saarstahl AG

- Essar

- Hyundai Steel

- JFE Steel Corporation

- JSW Steel Ltd.

- Nippon Steel Corporation

- Nucor Corporation

- POSCO

- SSAB AB

- thyssenkrupp Steel Europe

- Voestalpine AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Offshore-wind monopile foundations driving demand

- 4.2.2 Abrasion-resistant plates adopted in autonomous mining truck bodies

- 4.2.3 Seismic-resilient normalized plate mandated by new building codes

- 4.2.4 Duplex stainless plates for green-hydrogen electrolyzer pressure vessels in Europe

- 4.2.5 Lightweight cargo-ship designs utilising heat treated steel plate

- 4.3 Market Restraints

- 4.3.1 Composites replacing wear plate in next-gen earth-moving equipment

- 4.3.2 Energy-price volatility reducing furnace utilisation

- 4.3.3 Stricter NOx/CO2 furnace-emission caps raising compliance cost

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Steel Type

- 5.1.1 Carbon Steel

- 5.1.2 Alloy Steel

- 5.1.3 Stainless Steel

- 5.2 By Heat-Treatment Type

- 5.2.1 Annealing

- 5.2.2 Tempering

- 5.2.3 Normalizing

- 5.2.4 Thermo-Mechanical Controlled Process (TMCP)

- 5.2.5 Quenching

- 5.3 By End-Use Sector

- 5.3.1 Automotive and Heavy Machinery

- 5.3.2 Building and Construction

- 5.3.3 Shipbuilding and Offshore Structures

- 5.3.4 Energy and Power (Oil, Gas, Renewables)

- 5.3.5 Others (Metalworking, Transportation)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Russia

- 5.4.3.8 Turkey

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Egypt

- 5.4.5.5 South Africa

- 5.4.5.6 Nigeria

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ArcelorMittal

- 6.4.2 Baosteel Co.,Ltd.

- 6.4.3 China Ansteel Group Corporation Limited

- 6.4.4 China BaoWu Steel Group Corporation Limited

- 6.4.5 Dillinger Hutte Saarstahl AG

- 6.4.6 Essar

- 6.4.7 Hyundai Steel

- 6.4.8 JFE Steel Corporation

- 6.4.9 JSW Steel Ltd.

- 6.4.10 Nippon Steel Corporation

- 6.4.11 Nucor Corporation

- 6.4.12 POSCO

- 6.4.13 SSAB AB

- 6.4.14 thyssenkrupp Steel Europe

- 6.4.15 Voestalpine AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment