PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066607

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066607

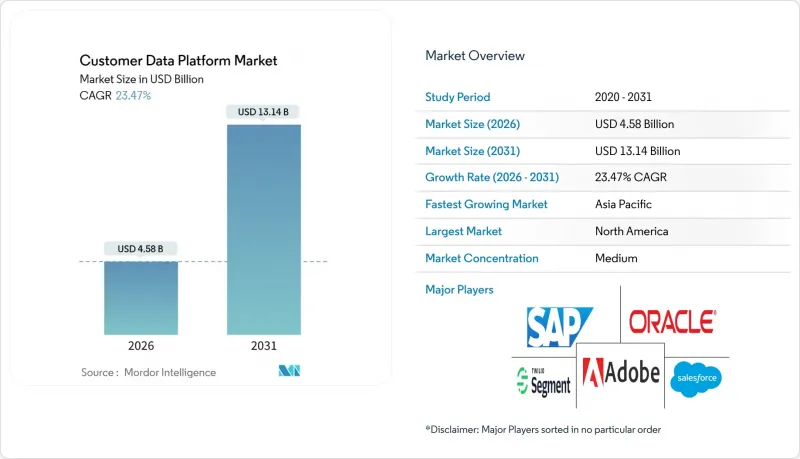

Customer Data Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the customer data platform market size is valued at USD 4.58 billion in 2026 and is projected to reach USD 13.14 billion by 2031, advancing at a 23.47% CAGR over the forecast period.

This report is Segmented by Component (Platform, and Services), Deployment Mode (Cloud, and On-Premise), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance, Media and Entertainment, Healthcare, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Customer Data Platform Market Trends and Insights

Phase-Out of Third-Party Cookies Accelerating First-Party Data Investments by European Retailers

Google's final removal of third-party cookies from Chrome eliminates cross-site identifiers that fueled programmatic advertising. European retailers are rebuilding their audience insights around loyalty programs, authenticated sessions, and progressive profiling to generate deterministic first-party data. Customer data platforms have therefore shifted from optional martech to foundational infrastructure that unifies consented signals across web, store, and call-center interactions. Platforms that provide integrated consent orchestration and deterministic identity stitching are winning deals because they simplify compliance with the General Data Protection Regulation. Early adopters that completed migration before 2025 cited 15-25% lifts in customer lifetime value and 10-12% improvements in media efficiency after reallocating spend toward owned channels. Growing first-party addressability also enables these retailers to negotiate better audience-extension deals with walled-garden publishers, amplifying the economic upside of CDP projects.

Headless and Omnichannel Commerce Boom in Asia Pacific Raising Demand for Event-Driven Data Unification

Retailers in India, Indonesia, and Vietnam are decoupling front-end experiences from back-end engines to support mobile-first shopping journeys. Headless architecture generates thousands of behavioral events from progressive web apps, super-app mini-stores, and social commerce plug-ins, overwhelming batch-oriented marketing suites. Streaming customer data platforms that capture, transform, and join these event flows into real-time profiles allow marketers to trigger personalized offers within milliseconds of basket abandonment. Merchants using event-driven CDPs recorded 30-40% conversion uplifts compared to peers using daily batch workflows. Super-app ecosystems common in Southeast Asia further increase data complexity because a single user ID spans payments, ride-hailing, and marketplace verticals. CDP vendors that resolve identities across those domains without exporting data outside regional borders are therefore preferred as data-localization laws tighten in India and Indonesia.

Fragmented Legacy Banking Schemas Limiting CDP ROI in Europe

Most European banks still run mainframe cores where customer data is scattered across products, each with different identifiers in the customer data platform market. A CDP must reconcile checking, mortgage, and wealth attributes in a single profile, yet conflicting keys lead to 12-18-month engineering projects that inflate budgets by up to 60% compared to greenfield deployments. Data-minimization clauses under the General Data Protection Regulation further constrain profile enrichment because banks must justify every persisted attribute. Several tier-one institutions that launched CDPs without first modernizing schemas realized minimal lift in email conversion because fragmented profiles could not trigger timely offers across channels. Interest is therefore shifting toward composable banking, which wraps legacy systems with application programming interfaces, but adoption remains slow due to migration risk.

Other drivers and restraints analyzed in the detailed report include:

- AI-Powered Predictive Patient Engagement Driving Healthcare CDP Uptake in the United States and Europe

- Generative AI Agents Requiring Real-Time Customer Graphs for Next-Best-Action in North American Retail Banking

- High Total Cost of Ownership of On-Premise CDPs Discourages South American SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform solutions accounted for 79.82% of total 2025 revenue of the customer data platform market, underscoring the importance of proprietary identity graphs that reconcile deterministic and probabilistic signals across every channel. This dominance is expected to persist because many buyers still prefer end-to-end functionality that combines unification, segmentation, and activation into a single vendor contract. The services segment, however, is on a 23.82% annual growth trajectory as organizations seek guidance on configuring composable stacks, instituting privacy governance, and training marketers on low-code orchestration.

Professional services teams are increasingly retained after go-live to monitor data quality and optimize campaigns, generating high-margin recurring revenue. Managed services appeal to firms that lack in-house data engineering talent, especially in regulated verticals where audit trails must be updated continuously. Implementation tasks are slowly being commoditized as offshore centers in India and Eastern Europe automate extract-transform-load mapping using reusable libraries. Consequently, consulting value is migrating toward strategic advisory, such as lifetime-value modeling and multi-touch attribution, areas where domain expertise rather than coding speed confers an advantage.

Cloud deployments accounted for 88.43% of the 2025 customer data platform market share, reflecting the appeal of elastic compute that absorbs Black Friday traffic without over-provisioning servers. The cloud segment is also the fastest-growing, with a 23.89% CAGR through 2031, as zero-copy integrations with Snowflake, Databricks, and Google BigQuery eliminate storage duplication. On-premises installations persist mainly in financial services and healthcare institutions that demand in-house control over sensitive records, yet their share is eroding as hybrid architectures route activation workloads to the public cloud while retaining restricted data locally.

Edge computing is creating a complementary layer where lightweight identity graphs sit close to point-of-sale terminals or connected vehicles in the customer data platform market. Vendors that synchronize these edge profiles with centralized cloud instances achieve latency below 200 milliseconds, meeting in-store personalization requirements without compromising cross-channel orchestration. Multi-cloud strategies are expanding as chief technology officers seek to avoid lock-in; this preference favors CDPs that remain agnostic by containerizing services or adopting open table formats such as Apache Iceberg. Subscription pricing converts capital expenses into operating expenses, improving vendor revenue visibility but requiring stronger cash management among growth-stage entrants.

Geography Analysis

North America remained the single largest region, accounting for 47.32% of 2025 revenue of the customer data platform market, supported by widespread cloud adoption, strong digital ad budgets, and privacy statutes such as the California Consumer Privacy Act that reward transparent first-party data practices. The region also benefits from a dense ecosystem of system integrators and data-science talent that shortens deployment timelines. The customer data platform market is expanding here as banks, insurers, and healthcare providers integrate streaming telemetry into unified profiles for generative AI agents.

Asia Pacific is the fastest-growing region, with a 24.41% CAGR through 2031. Headless commerce in India, Indonesia, and Vietnam generates event streams that legacy marketing clouds cannot reconcile, pushing mid-market retailers toward event-driven CDPs. China's Personal Information Protection Law and India's Digital Personal Data Protection Act require in-country storage, so vendors are launching geo-fenced instances to meet localization mandates. This fragmentation increases operational costs but expands the total addressable market, as every multinational now needs separate regional deployments.

Europe's adoption curve remains healthy as General Data Protection Regulation enforcement intensifies, yet fragmented legacy cores in banking and telecom extend implementation cycles. The Middle East represents a high-growth pocket because 5G monetization drives telcos in Saudi Arabia and the United Arab Emirates to deploy CDPs that unify subscriber, network, and billing data. Africa and South America lag due to limited cloud infrastructure, macroeconomic volatility, and high on-premise costs, though regional cloud providers with local data centers are beginning to close the gap.

- Salesforce.com, Inc.

- Oracle Corporation

- Adobe Inc.

- SAP SE

- Twilio Inc.

- Segment.io Inc.

- Arm Ltd.

- Tealium Inc.

- Acquia Inc.

- BlueConic, Inc.

- mParticle Inc.

- Zeta Global Corp.

- Amperity Inc.

- ActionIQ, Inc.

- Klaviyo Inc.

- RedPoint Global Inc.

- Bloomreach, Inc.

- Lexer Pty Ltd

- RudderStack, Inc.

- Snowplow Analytics Ltd.

- Zeotap GmbH

- Optimove Inc.

- Leadspace, Inc.

- Ometria Ltd.

- Blueshift Labs, Inc.

- Simon Data, Inc

- Lytics, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Phase-Out of Third-Party Cookies Accelerating First-Party Data Investments by European Retailers

- 4.2.2 Headless and Omnichannel Commerce Boom in Asia Pacific Raising Demand for Event-Driven Data Unification

- 4.2.3 AI-Powered Predictive Patient Engagement Driving Healthcare CDP Uptake in U.S. and EU

- 4.2.4 5G Lifecycle Monetization Initiatives Fueling CDP Deployments by Middle East Telcos

- 4.2.5 Zero-Copy Data Warehouse Integrations Cutting Data Egress Costs for Global Enterprises

- 4.2.6 Generative AI Agents Requiring Real-Time Customer Graphs for Next-Best-Action in North American Retail Banking

- 4.3 Market Restraints

- 4.3.1 Fragmented Legacy Banking Schemas Limiting CDP ROI in Europe

- 4.3.2 High TCO of On-Premise CDPs Discouraging South American SMEs

- 4.3.3 Shortage of Reverse-ETL Talent Hindering Composable CDP Rollouts in Asia Pacific

- 4.3.4 Data-Localization Mandates (China PIPL, India DPDP) Restricting Multi-Region CDPs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Outlook (GDPR, CCPA, PIPL, DPDP)

- 4.6 Technological Outlook (AI/ML, Composable and Reverse-ETL, Edge CDP)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-User Industry

- 5.4.1 Retail and E-Commerce

- 5.4.2 Banking, Financial Services, and Insurance

- 5.4.3 IT and Telecommunication

- 5.4.4 Media and Entertainment

- 5.4.5 Healthcare

- 5.4.6 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Funding, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)}

- 6.4.1 Salesforce.com, Inc.

- 6.4.2 Oracle Corporation

- 6.4.3 Adobe Inc.

- 6.4.4 SAP SE

- 6.4.5 Twilio Inc.

- 6.4.6 Segment.io Inc.

- 6.4.7 Arm Ltd.

- 6.4.8 Tealium Inc.

- 6.4.9 Acquia Inc.

- 6.4.10 BlueConic, Inc.

- 6.4.11 mParticle Inc.

- 6.4.12 Zeta Global Corp.

- 6.4.13 Amperity Inc.

- 6.4.14 ActionIQ, Inc.

- 6.4.15 Klaviyo Inc.

- 6.4.16 RedPoint Global Inc.

- 6.4.17 Bloomreach, Inc.

- 6.4.18 Lexer Pty Ltd

- 6.4.19 RudderStack, Inc.

- 6.4.20 Snowplow Analytics Ltd.

- 6.4.21 Zeotap GmbH

- 6.4.22 Optimove Inc.

- 6.4.23 Leadspace, Inc.

- 6.4.24 Ometria Ltd.

- 6.4.25 Blueshift Labs, Inc.

- 6.4.26 Simon Data, Inc

- 6.4.27 Lytics, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment