PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066622

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066622

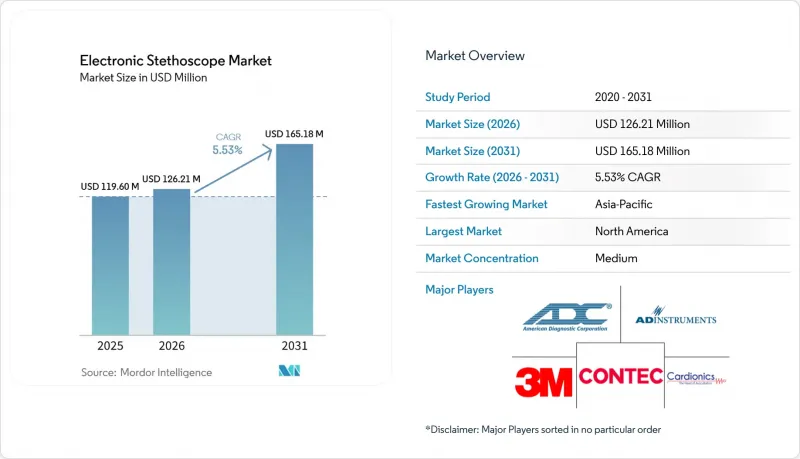

Electronic Stethoscope - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the electronic stethoscope market size is projected to expand from USD 119.60 million in 2025 and USD 126.21 million in 2026 to USD 165.18 million by 2031, registering a CAGR of 5.53% between 2026 to 2031.

This report Segments the Industry Into by Product (Amplified Electronic Stethoscopes, Digital Electronic Stethoscopes), Technology (Integrated Chest-Piece System, Wireless Transmission System, and More), End User (Hospitals and Clinics, Ambulatory Surgery Centers, and More), Connectivity (Wired, Bluetooth, and Wi-Fi), Distribution Channel (Offline Retail & Distributors, and More), and Geography

Global Electronic Stethoscope Market Trends and Insights

High Prevalence of Cardiovascular & Pulmonary Diseases Globally

Cardiovascular diseases remain the leading global cause of mortality, and rising respiratory morbidity is amplifying demand for acoustically sophisticated tools. Amplification chips and adaptive noise-cancellation circuits embedded in electronic stethoscopes now allow clinicians to discern Grade I murmurs in crowded emergency rooms, a scenario nearly impossible with traditional acoustic models. Peer-reviewed research demonstrates that AI-augmented devices can reach 88 % sensitivity for valvular heart murmur detection . Hospitals using digital stethoscopes in primary care are seeing a drop in referrals to echocardiography. This suggests that accurate early triage is changing the demand for larger imaging equipment.

Increasing Shift Toward Home-Based Chronic-Disease Management in Ageing Populations

Home healthcare, forecast to grow at 6.4% CAGR through 2030, is becoming the test-bed for consumer-grade digital auscultation. Devices with single-button data upload let older adults conduct daily heart-sound checks while family physicians review waveforms asynchronously. A recent pediatric asthma study recorded 93.2% accuracy using an AI-aided home stethoscope, and clinicians note a behavioral dividend: parents who hear audible feedback through smartphone apps tend to adhere more consistently to inhaler regimens. That feedback loop quietly lowers payer risk by nudging patients toward evidence-based self-management, a benefit that seldom shows up in device ROI spreadsheets but increasingly resonates with capitated payment models.

High Upfront Device and Maintenance Costs Versus Conventional Acoustic Stethoscopes

Premium digital units can cost up to ten times more than acoustic instruments, a hurdle in procurement cycles that favor low unit-prices. Yet executive interviews in budget-constrained facilities reveal a subtle shift: decision makers are now comparing total diagnostic pathway costs rather than sticker prices. When savings from avoided referrals or duplicated imaging are factored in, CFOs increasingly view electronic stethoscopes as cost-neutral within two to three years of adoption. The insight here is that vendors who frame value propositions around care-pathway economics, rather than hardware features, accelerate purchase approvals even in emerging markets.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements

- Growing Demand for Teleconsultation

- EHR Integration Partnerships Enhancing Diagnostic Workflow Efficiency

- Data-Privacy & Cybersecurity Concerns Limiting Cloud Connectivity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital electronic stethoscopes hold a 58.62% share in 2025, expanding at 7.65 % CAGR toward 2031. They convert acoustic signals into high-resolution digital waveforms, enabling noise filtering, data storage, and tele-streaming-capabilities that legacy amplified electronic devices cannot match. Institutions that embed these digital models into chronic-care programs also gain a growing archive of patient-specific heart-sound "fingerprints," which machine-learning tools mine to predict decompensation events days before symptoms appear. Thinklabs One, which uses electromagnetic diaphragm technology, exemplifies how premium sound fidelity can unlock niche use cases such as neonatal cardiology wards where low-amplitude murmurs matter most .

AI-enabled auscultation systems, expected to grow at 7.72 % CAGR (2026-2031), are rapidly converging hardware and software roadmaps. Eko Health's FDA-cleared algorithm detects heart murmurs with 88 % sensitivity and specificity . More specialized solutions, such as VoqX for aortic stenosis detection, illustrate the business logic of targeting single-disease verticals where reimbursement codes already exist. Wireless transmission modules running on Bluetooth 5.2 chipsets further expand utility by streaming lossless audio to smartphones with sub-50 millisecond latency, a threshold clinicians cite as "good enough" for real-time teleconsults.

Geography Analysis

North America holds a 37.92% share in 2025, underpinned by sophisticated reimbursement codes for remote auscultation and clear FDA pathways that de-risk capital deployment. Multistate hospital chains increasingly stipulate EHR-integration compatibility in tenders, a requirement that favors vendors with mature application-programming interfaces.

Asia-Pacific's 8.45% CAGR tells a different story: government programs in India now fund tele-auscultation pilots in district hospitals, effectively underwriting demand for Bluetooth-capable devices. Vendors able to localize user interfaces into regional languages are finding lower churn rates, hinting at the long-run importance of cultural tailoring. Europe sits in a middle position; CE-marking rigor elevates quality thresholds, but once a device clears regulatory gates, publicly funded health systems can authorize rapid nationwide rollouts. Meanwhile, early-adopter hospitals in the Gulf Cooperation Council region often leapfrog straight to AI-enabled models, leveraging favorable oil-backed healthcare budgets to deploy cutting-edge diagnostics as prestige projects.

- 3M

- Eko Health Inc.

- Thinklabs Medical LLC

- American Diagnostic

- Cardionics, Inc.

- HD Medical Group

- eKuore (BID BIOTECH)

- Contec Medical Systems

- ADInstruments Pty Ltd

- Meditech Equipment

- Welch Allyn (Hillrom)

- Rudolf Riester

- SensiCardiac

- CliniCloud

- A&D Company, Ltd.

- Dongjin Medical

- M3DICINE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Prevalence of Cardiovascular & Pulmonary Diseases Globally

- 4.2.2 Increasing shift toward home-based chronic-disease management in ageing populations

- 4.2.3 Technological advancements

- 4.2.4 Expansion of reimbursed telehealth and remote-patient-monitoring programs across major healthcare systems

- 4.2.5 Growing demand for teleconsultation

- 4.2.6 EHR Integration Partnerships Enhancing Diagnostic Workflow Efficiency

- 4.3 Market Restraints

- 4.3.1 High upfront device and maintenance costs versus conventional acoustic stethoscopes

- 4.3.2 Electromagnetic Interference with Other Medical Electronics

- 4.3.3 Data-Privacy & Cybersecurity Concerns Limiting Cloud Connectivity

- 4.3.4 Limited Physician Training and Change Resistance

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Amplified Electronic Stethoscopes

- 5.1.2 Digital Electronic Stethoscopes

- 5.2 By Technology

- 5.2.1 Integrated Chest-Piece System

- 5.2.2 Wireless Transmission System

- 5.2.3 Integrated Receiver Head-Piece System

- 5.2.4 AI-Enabled Auscultation System

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Ambulatory Surgery Centers

- 5.3.3 Home Healthcare Settings

- 5.3.4 Veterinary Clinics

- 5.4 By Connectivity

- 5.4.1 Wired

- 5.4.2 Bluetooth

- 5.4.3 Wi-Fi

- 5.5 By Distribution Channel

- 5.5.1 Offline Retail & Distributors

- 5.5.2 Online Marketplaces

- 5.5.3 Direct Institutional Tenders

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 3M

- 6.3.2 Eko Health Inc.

- 6.3.3 Thinklabs Medical LLC

- 6.3.4 American Diagnostic Corporation

- 6.3.5 Cardionics, Inc.

- 6.3.6 HD Medical Group

- 6.3.7 eKuore (BID BIOTECH)

- 6.3.8 Contec Medical Systems Co., Ltd.

- 6.3.9 ADInstruments Pty Ltd

- 6.3.10 Meditech Equipment Co., Ltd.

- 6.3.11 Welch Allyn (Hillrom)

- 6.3.12 Rudolf Riester GmbH

- 6.3.13 SensiCardiac

- 6.3.14 CliniCloud

- 6.3.15 A&D Company, Ltd.

- 6.3.16 Dongjin Medical

- 6.3.17 M3DICINE

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment