PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066626

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066626

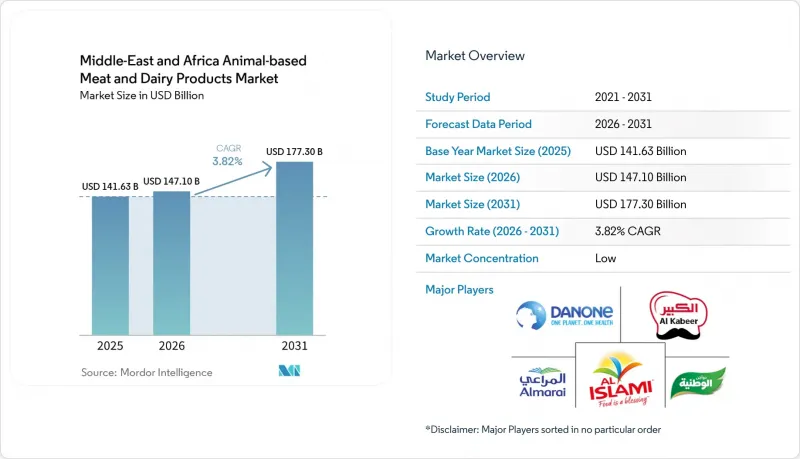

Middle-East And Africa Animal-based Meat And Dairy Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the middle east and Africa animal-based meat and dairy products market size is projected to expand from USD 141.63 billion in 2025 to USD 147.10 billion in 2026. This report is Segmented by Product Type (Dairy Products and Meat Products), Distribution Channels (On-Trade and Off-Trade), and Geography (Saudi Arabia, South Africa, United Arab Emirates, Nigeria, Egypt, Morocco, Rest of Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Middle-East And Africa Animal-based Meat And Dairy Products Market Trends and Insights

Growing Demand for Protein-Rich Products

Per-capita animal-protein intake in the Gulf Cooperation Council reached 63 kilograms in 2025, outpacing the global average by 40%, yet micronutrient deficiencies persist among lower-income expatriate cohorts who rely on cheaper processed meats with suboptimal amino-acid profiles. This paradox drives premiumization: Al Safi Danone launched a 36-gram-protein milk format in 2025, targeting fitness enthusiasts willing to pay a 30% premium over commodity UHT milk, while Almarai's protein smoothie line delivers 30 grams per 330-milliliter serving, embedding whey isolates sourced from its vertically integrated dairy farms. South Africa's poultry sector, supplying 60% of national meat consumption, benefits from maize-price deflation, local yellow maize fell 12% year-on-year in December 2025, enabling processors to hold retail prices flat while expanding margins, according to the United States Department of Agriculture. Nigeria's National Livestock Transformation Plan, allocating 5-year tax holidays and import-duty waivers, aims to triple domestic yogurt capacity by 2028, reducing reliance on powdered imports that accounted for USD 1.5 billion in 2024. The protein pivot also reshapes retail: hypermarkets in Riyadh and Dubai now dedicate 18-20% of chilled space to high-protein SKUs, up from 12% in 2023, signaling structural demand rather than fad.

Population Growth and Urbanization Boost Consumption of Convenient Processed Products

Nigeria's urban population surpassed 110 million in 2025, with Lagos and Abuja metro areas absorbing 2.8 million net migrants annually, compressing meal-preparation time and elevating demand for pre-marinated chicken, portion-controlled meatballs, and single-serve yogurt cups. Egypt's convenience-store footprint expanded 22% in 2024-2025, stocking ambient-stable processed cheese and UHT flavored milk that bypasses cold-chain gaps in secondary cities like Aswan and Luxor. Saudi Arabia's Vision 2030 target of 150 million annual tourists by 2030, up from 109 million in 2024, fuels quick-service restaurant proliferation; Dubai welcomed 19.5 million visitors in 2025, each generating 4.2 kilograms of meat and dairy consumption during their stay, according to UAE Ministry of Economy estimates. Processed-meat formats, like sausages, burgers, and kebabs, capture 38% of total meat volume in the GCC, versus 22% in sub-Saharan Africa, reflecting infrastructure maturity and disposable income. Morocco's dairy cooperatives introduced 200-milliliter flavored-milk pouches in 2025, priced at MAD 5 (USD 0.50), undercutting imported Tetra Pak cartons by 35% and penetrating rural souks previously reliant on loose milk.

Heavy Reliance on Imports

Egypt imported 90% of its feed crops in 2024, exposing dairy and poultry margins to currency devaluation. The Egyptian pound weakened 38% against the dollar during 2024-2025, inflating maize costs by 40% and forcing processors to raise retail prices 12-18%, dampening volume growth. Nigeria's USD 1.5 billion annual dairy-powder import bill persists despite government incentives, as local milk collection remains fragmented across 180,000 smallholders lacking refrigeration, resulting in 22% spoilage before processing. The GCC's 80-85% food-import dependency spiked logistics costs when Red Sea disruptions in 2024-2025 rerouted shipments around the Cape of Good Hope, adding 14 days transit time and lifting freight premiums 250-500%, eroding processor margins by 3-5 percentage points. Sudan's civil conflict curtailed livestock exports to Egypt and Saudi Arabia, removing 1.2 million head of cattle from the regional supply in 2024 and pushing beef prices up 40% in Cairo's wholesale markets. South Africa's foot-and-mouth outbreak in 2024 triggered import bans from the UAE, Saudi Arabia, and Qatar, costing the industry ZAR 1.25 billion (USD 68 million) in lost beef exports and forcing producers to absorb inventory at 30% discounts domestically.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances Enhance Production Efficiency and Quality Control

- Shift to Premium, Artisanal Dairy and Meat Appeals to Affluent Segments

- Competition from Plant-Based Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, meat products accounted for 62.38% of total revenues. However, dairy beverages are on the rise, boasting a 5.46% CAGR through 2031, the fastest growth rate among all product categories. This shift comes as Gulf consumers transition from sugary soft drinks to protein-fortified milk and probiotic smoothies. Al Safi Danone introduced a 36-gram protein milk format in 2025, targeting fitness enthusiasts and priced at a 30% premium over standard UHT milk. Their Greek Gelato yogurt line, featuring 15 grams of protein in a 150-gram cup, swiftly captured 8% of Saudi Arabia's chilled yogurt market within just six months. In the GCC, processed meats, encompassing sausages, burgers, and meatballs, constitute 38% of the total meat volume. This surge is fueled by the proliferation of quick-service restaurants and a booming tourism sector. In 2025, Dubai's 19.5 million visitors each consumed an estimated 4.2 kilograms of meat and dairy, heightening the demand for portion-controlled, halal-certified products. In South Africa, poultry, dominating the white meat category, accounts for 60% of the nation's meat consumption. Benefiting from a 12% year on year deflation in maize prices as of December 2025, processors managed to keep retail prices stable while boosting their margins. Meanwhile, red meats, comprising beef, lamb, and mutton, grapple with challenges. A foot and mouth outbreak in 2024 led to import bans in South Africa, halting exports to the UAE and costing the industry USD 68 million. Yet, premium lamb products, despite making up only 6% of the volume, command a notable 11% share of red meat revenue, driven by heightened demand during Ramadan gifting.

Cheese premiumization is reshaping the dairy landscape. South Africa's artisanal cheese producers clinched 12 medals at the 2024 World Cheese Awards. However, with an annual output of just 8,000 tons, less than 2% of the national production, their export potential remains largely untapped. Ice cream and frozen dairy products are witnessing steady growth, buoyed by Saudi Arabia's ambitious target of attracting 150 million tourists annually by 2030. The UAE's hospitality sector, with 650 hotel projects adding 161,574 rooms by 2032, is embedding dessert offerings as lucrative upsells. While health-conscious millennials are pressuring traditional dairy and butter volumes, Nigeria's National Livestock Transformation Plan, featuring 5-year tax holidays, is set to triple the country's yogurt capacity by 2028. This move aims to replace the USD 1.5 billion spent annually on dairy powder imports. The rising prominence of dairy beverages is underscored by structural demand shifts: Gulf hypermarkets have increased their chilled space allocation for high protein SKUs from 12% in 2023 to 18-20% now, highlighting the mainstreaming of functional nutrition.

List of Companies Covered in this Report:

- Almarai Company

- Al-Watania Poultry Co.

- Al Islami Foods

- Al Kabeer Group

- Al Ain Farms

- Danone S.A.

- Clover Industries Ltd

- Lactalis S.A.

- Astral Foods Ltd

- RCL Foods Ltd

- Juhayna Food Industries

- Savola Group

- Al Rawabi Dairy Company

- FrieslandCampina WAMCO Nigeria

- Tnuva Israel Ltd

- BRF S.A. (Sadia & Seara MEA)

- Mezzan Holding Co.

- Al Dahra Agriculture

- JBS S.A.

- BIDCORO Africa Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand For Protein-Rich Products

- 4.2.2 Population Growth And Urbanization Boost Consumption Of Convenient Processed Products

- 4.2.3 Technological Advances Enhance Production Efficiency And Quality Control

- 4.2.4 Shift To Premium Artisanal Dairy And Meat Appeals To Affluent Segments

- 4.2.5 Infrastructure Investments Improve Cold Chain Logistics For Perishables

- 4.2.6 Rising Government Food-Security Investment Programs

- 4.3 Market Restraints

- 4.3.1 Heavy Reliance On Imports

- 4.3.2 Competition From Plant-Based Alternatives

- 4.3.3 Regulatory Hurdles And Food Safety Standards

- 4.3.4 High Production Costs Limit Scalability

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Product Type

- 5.1.1 Dairy Products

- 5.1.1.1 Milk

- 5.1.1.2 Yogurt

- 5.1.1.3 Cheese

- 5.1.1.4 Butter

- 5.1.1.5 Ice Cream & Frozen Dairy

- 5.1.1.6 Dairy Beverages (Flavored / Functional)

- 5.1.1.7 Others

- 5.1.2 Meat Products

- 5.1.2.1 Red Meat

- 5.1.2.1.1 Beef

- 5.1.2.1.2 Lamb & Mutton

- 5.1.2.1.3 Others

- 5.1.2.2 White Meat

- 5.1.2.2.1 Chicken

- 5.1.2.2.2 Others

- 5.1.2.3 Processed Meat

- 5.1.2.3.1 Sausages

- 5.1.2.3.2 Burgers & Patties

- 5.1.2.3.3 Meatballs

- 5.1.2.3.4 Others

- 5.1.2.1 Red Meat

- 5.1.1 Dairy Products

- 5.2 Distribution Channels

- 5.2.1 On-Trade

- 5.2.2 Off-Trade

- 5.2.2.1 Supermarkets/Hypermarkets

- 5.2.2.2 Convenience Stores

- 5.2.2.3 Online Retail Channels

- 5.2.2.4 Other Distrbution Channels

- 5.3 Geography

- 5.3.1 Saudi Arabia

- 5.3.2 South Africa

- 5.3.3 United Arab Emirates

- 5.3.4 Nigeria

- 5.3.5 Egypt

- 5.3.6 Morocco

- 5.3.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Almarai Company

- 6.4.2 Al-Watania Poultry Co.

- 6.4.3 Al Islami Foods

- 6.4.4 Al Kabeer Group

- 6.4.5 Al Ain Farms

- 6.4.6 Danone S.A.

- 6.4.7 Clover Industries Ltd

- 6.4.8 Lactalis S.A.

- 6.4.9 Astral Foods Ltd

- 6.4.10 RCL Foods Ltd

- 6.4.11 Juhayna Food Industries

- 6.4.12 Savola Group

- 6.4.13 Al Rawabi Dairy Company

- 6.4.14 FrieslandCampina WAMCO Nigeria

- 6.4.15 Tnuva Israel Ltd

- 6.4.16 BRF S.A. (Sadia & Seara MEA)

- 6.4.17 Mezzan Holding Co.

- 6.4.18 Al Dahra Agriculture

- 6.4.19 JBS S.A.

- 6.4.20 BIDCORO Africa Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK