PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066627

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066627

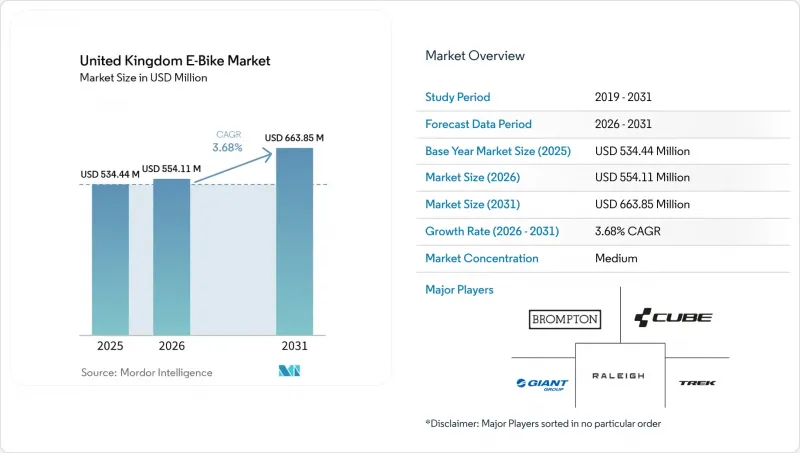

United Kingdom E-Bike - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united kingdom e-bike market size is expected to grow from USD 534.44 million in 2025 to USD 554.11 million in 2026 and is forecast to reach USD 663.85 million by 2031 at a 3.68% CAGR over 2026-2031.

This report is Segmented by Propulsion Type (Pedal Assisted and More), Application Type (Cargo/Utility and More), Battery Type (Lead-Acid Battery and More), Motor Placement (Hub Front/Rear and Mid-Drive), Drive Systems (Chain Drive and Belt Drive), Motor Power, Price Band, Sales Channel, End-Use, and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

United Kingdom E-Bike Market Trends and Insights

Growth of E-Cargo in Last-Mile Delivery

Cargo bike deployments jumped 63% year-on-year in London, and Transport for London forecasts that approximately 17% of van deliveries in central London could be replaced by cargo bikes by 2030. Operators like Evri are committed to tripling their e-cargo bike fleets between 2024 and 2025, validating the operational cost savings and congestion benefits. Food-delivery couriers represent a ready demand pool, accounting for around 10% of London cycle trips. Freight-innovation grants and city access rules strengthen the commercial case, making cargo the fastest-growing professional use case.

Expansion of Protected Cycling Infrastructure

The Consolidated Active Travel Fund has awarded GBP 168.5 million (USD 211 million) for 2025-26, 76% of which is earmarked for hard infrastructure. New protected lanes reduce perceived risk, a chief deterrent among older riders and families, and spur network effects as routes become contiguous. Greater Manchester, West Midlands, and West Yorkshire secure the largest grants, ensuring dense urban corridors that maximize usage. As safety improves, latent commuter demand converts into sales, supporting sustained growth beyond initial policy cycles.

Rising Battery-Fire Incidents and Safety Regulation

Safety incidents pose the most significant regulatory headwind, with 211 e-bike and e-scooter fires recorded in 2024, resulting in several fatalities and leading to tighter product-safety rules. Transport for London introduced a ban on folding e-bikes on rail in March 2025, hampering multimodal commutes. The United Kingdom's forces seized 937 illegally modified bikes, up 83%, signaling stricter enforcement. Compliance costs increase for new entrants, but certified brands can turn safety credentials into a selling point.

Other drivers and restraints analyzed in the detailed report include:

- Cycle-to-Work Tax Incentives and Employer Uptake

- Falling Lithium-Ion Battery Costs

- Inventory Overhang and Weak Bicycle Retail Sales

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pedal-assisted e-bikes led the United Kingdom's market, accounting for a significant 79.91% share in 2025. This dominance is largely due to the legal 250 W power limit, which classifies them as bicycles instead of mopeds. This classification provides key benefits like access to bike lanes, no need for vehicle registration, and lower insurance costs, making it popular among commuters and leisure riders. Manufacturers are improving torque-sensor algorithms to make the assistance feel more natural, which has led to positive reviews and repeat purchases, further strengthening the segment's position. As a result, the market for pedal-assist models in the UK is expected to grow steadily, aligning with the overall market's 3.68% CAGR through 2031.

Throttle-assisted e-bikes, while a smaller segment, are projected to grow at a 3.67% CAGR. These bikes are particularly favored by delivery couriers who need quick power in stop-and-go traffic. Regulatory actions, such as the seizure of 937 illegal high-power bikes by August 2024, show that authorities are enforcing compliance. However, certified throttle models still attract buyers where the productivity benefits outweigh the challenges of meeting regulations. To address this, component suppliers are offering firmware-locked throttles that can be adjusted to the legal 250 W limit, giving fleets a way to comply without losing functionality. While pedal-assist bikes maintain their lead, this approach allows throttle-assist models to thrive in specific commercial niches. Additionally, increasing urban congestion charges and restricted van access are pushing operators to adopt any legal option that ensures fast and efficient parcel delivery.

Urban trips accounted for 71.34% of total revenue in 2025, driven by factors such as dense populations, dedicated bike lanes, and high parking costs, which made e-bikes a convenient option for door-to-door travel. During 2025-26, Greater Manchester, West Midlands, and West Yorkshire received significant investments to develop new cycle corridors, boosting commuter confidence with improved infrastructure. Employers are also supporting this shift through Cycle-to-Work schemes that reduce purchase costs, making battery assistance indispensable for daily riders. As a result, the e-bike market in the United Kingdom is expected to grow steadily in urban commuting while maintaining its leadership in volume throughout the forecast period.

Although cargo and utility bikes currently represent a smaller segment, they are expected to grow faster than any other use case, with a 3.67% CAGR through 2031. Studies on cost-per-parcel show savings of over 20% compared to diesel vans, especially when factoring in traffic fines and congestion fees - a finding that appeals to logistics CFOs. Transport for London estimates that cargo bikes could handle around 17% of inner-city van deliveries by 2030, creating demand for thousands of additional units. Fleet operators are increasingly requesting factory-installed telematics for better logistics oversight, which raises entry barriers for low-cost brands. These trends place cargo bikes at the center of commercial electrification efforts, even though commuter volumes remain higher.

Lithium-ion technology accounted for 99.37% of the United Kingdom e-bike market in 2025. It is expected to grow steadily at a 3.68% CAGR through 2031. This growth is driven by lithium-ion's high energy density, which provides a good range without adding too much weight-an essential feature for folding e-bikes popular among rail commuters. As cell prices continue to decline, brands have two key options: keep their Manufacturer's Suggested Retail Prices (MSRPs) unchanged or offer higher-capacity battery packs at the same price. Both approaches help expand the total addressable market. While safety regulations are becoming stricter, established manufacturers already use certified battery management systems, thereby strengthening their competitive position. As a result, lithium-ion technology is expected to grow in line with the United Kingdom's overall 3.68% CAGR in the e-bike market, with no significant competition from alternative chemistries during the forecast period.

Local sourcing remains a challenge. The planned gigafactory in Coventry aims to produce up to 60 GWh of small-format batteries. However, data from the Faraday Institution show a 47% gap between projected demand and announced production capacity. This reliance on imports leaves OEMs vulnerable to currency fluctuations and shipping delays, forcing them to manage risks across both pricing and logistics. To address potential supply disruptions, some brands are designing modular battery bays that can work with cells from multiple suppliers. If domestic production ramps up as planned, manufacturers could benefit from shorter lead times and the ability to market "British-made" battery packs as an additional safety feature.

List of Companies Covered in this Report:

- Brompton Bicycle Ltd

- CUBE Bikes

- Evans Cycles

- Giant Manufacturing Co. Ltd

- Karbon Kinetics Ltd

- Maxon Group

- Powabyke UK Ltd

- Raleigh UK Ltd

- Tandem Group Cycles Ltd

- Trek Bicycle Corporation

- Volt Electric Bikes Ltd

- Estarli Ltd

- Whyte Bikes Ltd

- Ribble Cycles Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Key Industry Trends

- 4.1 Annual Bicycle Sales

- 4.2 Average Selling Price and Price to Band Mix

- 4.3 Cross to Border Trade in E to Bikes and Parts

- 4.4 E to Bike Share of Total Bicycle Sales

- 4.5 Commuters with 5to15 km One to Way Trips (%)

- 4.6 Bicycle / E to Bike Rental Market Size

- 4.7 E to Bike Battery Pack Price

- 4.8 Battery Chemistry Price Comparison

- 4.9 Last to Mile (Hyper to Local) Delivery Volume

- 4.10 Protected Bicycle Lanes (km)

- 4.11 Trekking / Outdoor Activity Participation

- 4.12 E to Bike Battery Capacity (Wh)

- 4.13 Urban Traffic Congestion Index

- 4.14 Regulatory Framework

- 4.14.1 Homologation and Certification

- 4.14.2 ExporttoImport and Trade Rules

- 4.14.3 Classification, Road Access and User Rules

- 4.14.4 Battery, Charger and Charging Safety

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Growth of E-Cargo in Last-Mile Delivery

- 5.2.2 Expansion of Protected Cycling Infrastructure

- 5.2.3 Cycle to Work Tax Incentives and Employer Uptake

- 5.2.4 Falling Lithium-Ion Battery Costs

- 5.2.5 U.K. Gigafactory Plans for Small-Format Cells

- 5.2.6 500W Power-Limit Proposal Unlocking New Models

- 5.3 Market Restraints

- 5.3.1 Rising Battery-Fire Incidents and Safety Regulation

- 5.3.2 Inventory Overhang and Weak Bicycle Retail Sales

- 5.3.3 TfL Ban on Non-Folding E-Bikes on Rail Network

- 5.3.4 Rental-Housing Storage Bans for E-Bikes

- 5.4 Value / Supply to Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Suppliers

- 5.7.3 Bargaining Power of Buyers

- 5.7.4 Threat of Substitutes

- 5.7.5 Intensity of Industry Rivalry

6 Market Size and Growth Forecasts (Value and Volume)

- 6.1 By Propulsion Type

- 6.1.1 Pedal Assisted

- 6.1.2 Speed Pedelec

- 6.1.3 Throttle Assisted

- 6.2 By Application Type

- 6.2.1 Cargo / Utility

- 6.2.2 City / Urban

- 6.2.3 Trekking / Mountain

- 6.3 By Battery Type

- 6.3.1 Lead-Acid Battery

- 6.3.2 Lithium-ion Battery

- 6.3.3 Others

- 6.4 By Motor Placement

- 6.4.1 Hub (Front / Rear)

- 6.4.2 Mid-Drive

- 6.5 By Drive Systems

- 6.5.1 Chain Drive

- 6.5.2 Belt Drive

- 6.6 By Motor Power

- 6.6.1 Below 250 W

- 6.6.2 251 to 350 W

- 6.6.3 351 to 500 W

- 6.6.4 501 to 600 W

- 6.6.5 Above 600 W

- 6.7 By Price Band

- 6.7.1 Up to EUR 1,000

- 6.7.2 EUR 1,000 to 1,499

- 6.7.3 EUR 1,500 to 2,499

- 6.7.4 EUR 2,500 to 3,499

- 6.7.5 EUR 3,500 to 5,999

- 6.7.6 Above EUR 6,000

- 6.8 By Sales Channel

- 6.8.1 Online

- 6.8.2 Offline

- 6.9 By End to Use

- 6.9.1 Commercial Delivery

- 6.9.1.1 Retail and Goods Delivery

- 6.9.1.2 Food and Beverage Delivery

- 6.9.2 Service Providers

- 6.9.3 Personal and Family Use

- 6.9.4 Institutional

- 6.9.5 Others

- 6.9.1 Commercial Delivery

- 6.10 By Region

- 6.10.1 England

- 6.10.2 Scotland

- 6.10.3 Wales

- 6.10.4 Northern Ireland

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 Brompton Bicycle Ltd

- 7.4.2 CUBE Bikes

- 7.4.3 Evans Cycles

- 7.4.4 Giant Manufacturing Co. Ltd

- 7.4.5 Karbon Kinetics Ltd

- 7.4.6 Maxon Group

- 7.4.7 Powabyke UK Ltd

- 7.4.8 Raleigh UK Ltd

- 7.4.9 Tandem Group Cycles Ltd

- 7.4.10 Trek Bicycle Corporation

- 7.4.11 Volt Electric Bikes Ltd

- 7.4.12 Estarli Ltd

- 7.4.13 Whyte Bikes Ltd

- 7.4.14 Ribble Cycles Ltd

8 Market Opportunities and Future Outlook

9 Key Strategic Questions for E to Bikes CEOs