PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066628

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066628

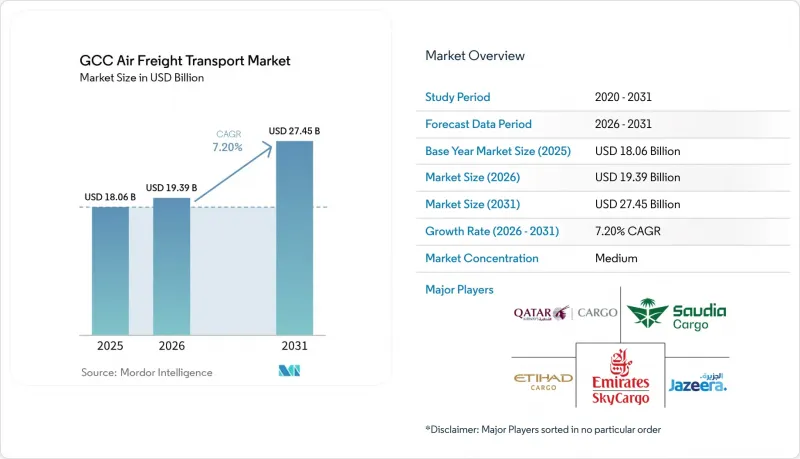

GCC Air Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the gCC air freight transport market size is expected to increase from USD 18.06 billion in 2025 to USD 19.39 billion in 2026 and reach USD 27.45 billion by 2031, growing at a 7.2% CAGR over 2026-2031.

The region is shifting from a pure trans-shipment corridor into a value-added logistics hub where forwarders orchestrate multi-modal flows between Asian manufacturers, European consumers, and emerging African demand centers. This report is Segmented by Destination (Domestic and International), by Carrier Type (Belly Cargo and Freighter), by Cargo Type (General Cargo and Special Cargo), by End-User Industry (E-Commerce and Retail, Manufacturing and Automotive, Healthcare and Pharmaceuticals, and More), and by Country (Saudi Arabia, UAE, Qatar, Kuwait, and More). The Market Forecasts are Provided in Terms of Value (USD).

GCC Air Freight Transport Market Trends and Insights

Near-Shoring Led Component Inflows to GCC Free Zones

Light manufacturers moving into tax-free industrial zones are generating two-way air freight flows. Dubai South's Logistics District offers full foreign ownership and duty deferment, prompting forwarders to open bonded facilities that allow staged clearance. Saudi Arabia is investing USD 266 billion to build 59 specialized logistics centers, each designed with direct apron access so parts can move from aircraft to assembly lines in under four hours posted 22% tenant growth during 2024, with electronics and automotive sub-assemblies leading inflows. The bidirectional model increases forwarder revenue touchpoints by adding kitting, labeling, and quality checks to traditional uplift. Customs brokers holding warehouse licenses capture more value than pure capacity brokers because they can defer duties until goods reach their final GCC market.

Reverse Logistics of E-Commerce Returns by Air

GCC online retail is set to hit USD 49.78 billion in 2027 with return rates of 15-20% for fashion and electronics. Kuehne+Nagel's new Dubai site, operational since Q2 2025, integrates return processing so rejected items ride the same flight as outbound orders, lowering per-unit transport costs by 30%. Returns need re-import documentation, inspection, and refurbishment, services that airlines have little incentive to provide. Emirates Delivers launched in Saudi Arabia during 2024 to serve direct-to-consumer flows, yet still outsources last-mile and returns to forwarders. Fragmented regulations across GCC states heighten compliance complexity, tilting competitive advantage toward multi-country customs specialists.

CORSIA and EU ETS Carbon-Cost Pass-Through

EU ETS charges of EUR 80-100 per tonne CO2 now apply to non-EU airlines, adding roughly USD 15-20 per tonne of cargo on Europe-bound flights. Emirates has earmarked USD 200 million for sustainability projects, yet sustainable aviation fuel costs remain two to four times higher than Jet A-1. Cost escalation encourages shippers of non-urgent goods to switch to ocean freight, shrinking the accessible pool for forwarders. Fragmented carbon disclosure regimes across the GCC add further administrative overhead.

Other drivers and restraints analyzed in the detailed report include:

- Open-Skies Pacts Unlocking Extra Belly Capacity

- AI-Driven Dynamic Capacity Marketplaces

- Freighter Oversupply from P2F Wave

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

International services captured 80.12% market share of traffic in 2025, reflecting the GCC air freight transport market's traditional bridge role between Asia, Europe, and Africa. Domestic uplift is forecast to post an 8.57% CAGR as Saudi Arabia's industrial clusters in Riyadh, Jeddah, and Dammam require same-day component deliveries that bypass port congestion. The GCC air freight transport market size for domestic corridors is projected to double by 2031, supported by Riyadh's move to allow foreign charter operators on intra-Kingdom runs.

Forwarders continue to dominate cross-border flows because every shipment still needs dual customs clearances and multi-currency documentation. Digital booking tools win small parcels, but larger component movements depend on bonded facilities that stage parts for assembly plants. Saudia Cargo's "Landing in China in 24" service validates growing eastbound export appetite for Saudi electronics and auto parts.

Belly holds supplied 66.30% market size of lift in 2025 because passenger flights offer dense frequency and competitive tariffs. The GCC air freight transport market share for freighter solutions will rise as oversized project cargo and -80°C pharma lanes outgrow dimensional and temperature limits of passenger aircraft.

Freighter tonnage is projected to record a 7.90% CAGR through 2031, yet charter yields may soften if P2F conversions overshoot demand. Forwarders arbitrage between lower belly spot rates in slack months and main-deck charters in peak seasons, protecting margin with dynamic procurement systems backed by AI. Emirates SkyCargo's extra B777Fs expand the GCC air freight transport market size for main-deck moves that cannot fit through lower-deck doors.

List of Companies Covered in this Report:

- Emirates SkyCargo

- Qatar Airways Cargo

- Saudia Cargo

- Etihad Cargo

- Jazeera Airways Cargo

- Maximus Air

- Gulf Air Cargo

- Oman Air Cargo

- Bahrain Air Cargo

- Air Charter Service

- Chapman-Freeborn

- Turkish Cargo

- Kuwait Airways Cargo

- Texel Air

- EGYPTAIR

- Royal Jordanian Cargo

- Middle East Airlines (MEA) Cargo

- Silk Way West Airlines

- Cathay Cargo

- Cargolux

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Near-Shoring Led Component Inflows to GCC Free Zones

- 4.2.2 Reverse-Logistics of E-Commerce Returns by Air

- 4.2.3 Open-Skies Pacts Unlocking Additional Belly Capacity

- 4.2.4 AI-Driven Dynamic Capacity Marketplaces

- 4.2.5 Hydrogen-Electric UAV Feeder Networks Pilot Projects

- 4.2.6 Precision-Therapy Cold-Chain Corridors (Cell and Gene)

- 4.3 Market Restraints

- 4.3.1 CORSIA and EU ETS Carbon-Cost Pass-Through

- 4.3.2 Freighter Oversupply from P2F Wave

- 4.3.3 Mega-Event Apron Congestion Risk

- 4.3.4 Cyber Vulnerabilities in Cargo Community Systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Pricing Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Dangerous Goods Standards Review

- 4.10 Impact of Geo-Political Events on the Market

5 Market Size and Growth Forecasts

- 5.1 By Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 By Carrier Type

- 5.2.1 Belly Cargo

- 5.2.2 Freighter

- 5.3 By Cargo Type

- 5.3.1 General Cargo

- 5.3.2 Special Cargo

- 5.4 By End-User Industry

- 5.4.1 E-commerce and Retail

- 5.4.2 Manufacturing and Automotive

- 5.4.3 Healthcare and Pharmaceuticals

- 5.4.4 Perishables and Fresh Produce

- 5.4.5 High-Tech and Electronics

- 5.4.6 Others

- 5.5 By Country

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Qatar

- 5.5.4 Kuwait

- 5.5.5 Bahrain

- 5.5.6 Oman

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, Recent Developments)

- 6.4.1 Emirates SkyCargo

- 6.4.2 Qatar Airways Cargo

- 6.4.3 Saudia Cargo

- 6.4.4 Etihad Cargo

- 6.4.5 Jazeera Airways Cargo

- 6.4.6 Maximus Air

- 6.4.7 Gulf Air Cargo

- 6.4.8 Oman Air Cargo

- 6.4.9 Bahrain Air Cargo

- 6.4.10 Air Charter Service

- 6.4.11 Chapman-Freeborn

- 6.4.12 Turkish Cargo

- 6.4.13 Kuwait Airways Cargo

- 6.4.14 Texel Air

- 6.4.15 EGYPTAIR

- 6.4.16 Royal Jordanian Cargo

- 6.4.17 Middle East Airlines (MEA) Cargo

- 6.4.18 Silk Way West Airlines

- 6.4.19 Cathay Cargo

- 6.4.20 Cargolux

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment