PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066646

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066646

Virtual Cards - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

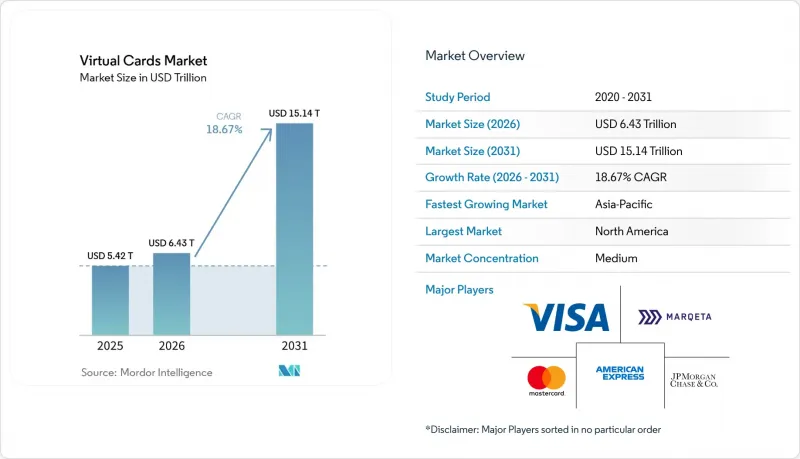

According to Mordor Intelligence, the virtual cards market size is projected to expand from USD 5.42 trillion in 2025 and USD 6.43 trillion in 2026 to USD 15.14 trillion by 2031, registering a CAGR of 18.67% between 2026 to 2031.

This report is Segmented by Use (Single-Use, Multi-Use), Payment Type (Remote Payments, POS Payments), End User (Consumer, Business), Card Type (Virtual Debit Card, Virtual Credit Card, Virtual Prepaid Card), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD)

Global Virtual Cards Market Trends and Insights

Accelerating B2B adoption of virtual cards for accounts payable automation

Finance leaders are moving payables from paper checks and manual ACH into virtual card workflows that integrate directly with ERP and AP automation, which shortens cycle times and supports interchange-funded rebates. In March 2025, an American Express survey of senior executives reported that 83% considered automated invoicing and payment processing important for supplier relationships, and 77% linked payments innovation to business growth. Platforms and networks are meeting this demand as Mastercard continues to expand virtual card enablement across leading procure-to-pay ecosystems. Oracle Fusion Cloud ERP users can now provision virtual cards natively through recent product integrations, which removes middleware steps for AP teams. Mid-sized and large enterprises are also signaling stronger working capital adoption of corporate and virtual cards in survey data that Visa published across global CFO and treasurer cohorts.

Rapid growth in e-commerce and digital commerce channels

Digital commerce is lifting remote and in-app transactions, with companies reporting higher usage of tokenized credentials provisioned into mobile wallets and merchant apps. Central bank statistics confirm that, in the first half of 2025, Finland recorded 1.2 billion card payments worth EUR 36.9 billion (USD 38.2 billion), reflecting strong growth in digital payment activity. Payments made via mobile applications accounted for 334 million transactions valued at EUR 8.1 billion (USD 8.4 billion), while virtual terminals represented 21 % of total card payment value, EUR 7.8 billion (USD 8.1 billion), up from 16 % three years earlier. This shift toward mobile and virtual payment channels highlights rising adoption of digital and card-not-present transactions, supporting demand for virtual card solutions. Wallet-centric models are also broadening cross-border access through virtual card issuance, including a program expansion allowing Orange Money customers to pay online across the Visa network. Networks are standardizing digital wallet launches and wallet tokenization at the point of provisioning, which supports tap-to-pay and card-not-present approvals with higher security. As tokenization reaches broader coverage, virtual cards continue to anchor merchant acceptance for e-commerce and in-app use cases.

Gaps in supplier acceptance and concerns over interchange costs

Acceptance friction remains a hurdle where suppliers resist card fees on large-ticket invoices and prefer lower-cost domestic A2A rails. Surveys of finance leaders highlight operational pain points around remittance data ingestion, invoice matching, and manual workflows when handling emailed or portal-based virtual card details. Supplier education on interchange programs and large-ticket pricing can improve acceptance when the total cost of payment is weighed against speed, certainty, and data benefits. Platforms are countering objections by embedding straight-through processing that maps Level III data into ERP systems, which reduces reconciliation time for supplier AR teams. Network programs that target B2B supplier onboarding and automated acceptance continue to expand, but broad-based adoption depends on clearer ROI for suppliers and simpler data flows.

Other drivers and restraints analyzed in the detailed report include:

- Government and regulatory initiatives promoting cash-lite economies and open banking framework

- Enhanced fraud prevention and security features compared with physical cards

- Complexity related to system connectivity and ERP integration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-use virtual cards commanded 59.13% share in 2025 and are projected to grow at a 20.03% CAGR through 2031, reflecting a security-first preference for ephemeral credentials in AP and travel payments, and this profile is a material driver of the virtual cards market. Single-use credentials simplify approval policies and vendor-locking, which reduces the risk of compromised numbers and makes out-of-policy spend easier to block at authorization. Online travel agencies use single-use virtual card numbers for supplier prepayments and settlement, which enhances reconciliation and reduces exposure if bookings are amended. Networks are also scaling issuer participation in virtual card programs for travel and lodging, which supports wider supplier acceptance and automated matching of detailed line items. As tokenization scales across e-commerce, the operational gap between single-use and multi-use narrows, but single-use remains the default for high-risk transactions in the virtual cards market.

Multi-use virtual cards serve recurring suppliers, subscriptions, and managed expense programs where persistent credentials reduce re-issuance overhead, though they grew more slowly than single-use variants. Recent ERP-native integrations, including Oracle Fusion Cloud ERP connectivity, are lowering deployment friction and enabling real-time policy controls across multi-use portfolios. Providers are adding PIN controls and enhanced merchant controls for international point-of-sale and online transactions to reduce fraud risk on persistent credentials. The combined effect improves the operational case for multi-use in categories like SaaS, cloud infrastructure, and logistics, where recurring billing dominates. Over time, near-ubiquitous tokenization can further close the security gap as multi-use tokens refresh dynamically, which supports broader adoption without sacrificing control.

Remote payments held a 73.64% share in 2025, with e-commerce and in-app transactions capturing a rising share of card value, and this behavior is visible in payments data published by national banks that track channel mix in the virtual cards market. The Bank of Finland reported that card payments initiated via mobile applications rose in H1 2025, and virtual terminals captured a larger share of value compared to prior years. Networks and issuers are provisioning virtual credentials into digital wallets at scale, which supports tap-to-pay growth in retail and streamlines e-commerce checkouts. Tokenization and network-managed credentials reduce false declines and fraud by replacing primary account numbers in transit and at rest during remote payments. As a result, remote use cases continue to anchor growth while in-person contactless rises from a lower base in the virtual cards market.

Point-of-sale usage is projected to grow at a 21.22% CAGR through 2031 as contactless acceptance nears ubiquity and more wallets support in-store provisioning of virtual credentials. European markets demonstrate the acceleration as networks report strong contactless penetration, with wallet launches enabling consumers to tap their phones or wearables for in-store payments. Brazil's Pix rail is capturing domestic A2A payments at scale, which adds competition at POS while virtual cards continue to serve international and wallet-funded use cases in the region. Hybrid flows are emerging where domestic instant payment rails handle small-value transactions, while virtual card tokens remain the preferred method in cross-border, travel, and controlled-spend scenarios. This dual-track evolution supports sustained growth across both channels as acceptance and wallet integration expand.

Geography Analysis

North America led with a 38.74% share in 2025, supported by a mature commercial card infrastructure, strong adoption of AP automation, and a large enterprise base that values rebates and working capital benefits in the virtual cards market. Canada enters 2026 with an open banking implementation framework that formalizes API-based data sharing, liability, and technical standards, and this reduces connectivity friction for virtual card funding and reconciliation. Issuers and platforms are also integrating with ERP systems and procurement software to bring virtual card issuance into native workflows for corporate finance teams. Growth corporates in the region are using cards more frequently for unplanned working capital needs, as captured in Visa's research across CFOs and treasurers. Together, these conditions strengthen share retention and support continued expansion across B2B and consumer use cases in the virtual cards market.

Asia-Pacific is projected to post the fastest 23.44% CAGR to 2031 as cash-lite programs, super-app ecosystems, and wallet-led checkouts normalize tokenized credentials across channels in the virtual cards market. Regional initiatives that emphasize instant payments and digital identity are increasing the utility of wallets, while virtual cards backstop cross-border purchases where domestic instant rails do not interoperate. Issuers and platforms are also expanding into APAC to capture growth in B2B and travel categories, supported by vendor partnerships that embed card creation into software. Cross-regional efforts that link wallets to global networks are broadening access for consumers and SMBs, including partnerships designed to allow online shopping across international merchants. These factors position Asia-Pacific to add share as deployments scale and digital credentials become the default in mobile-first markets, which further enlarges the virtual cards market.

Europe continues to expand on the back of regulatory convergence and strong contactless habits, with networks reporting broad wallet launches and high in-person tap rates that lift POS usage alongside e-commerce in the virtual cards market. Tokenization initiatives are improving approval rates and reducing online fraud, and the region is investing in data center capacity and digital infrastructure for payments resilience. In parallel, regulators are moving toward harmonized rules on instant payments and API access, which complements the adoption of virtual cards by creating interoperability and clear liability regimes. These steps encourage issuers, acquirers, and software vendors to build to common standards that simplify deployment across multiple markets in the region. As the regulatory and technology foundations mature, Europe remains a core demand center with balanced growth across B2B and consumer use cases in the virtual cards market.

- American Express Company

- Mastercard Incorporated

- Visa Inc.

- JPMorgan Chase & Co.

- Marqeta Inc.

- Stripe Inc.

- PayPal Holdings Inc.

- WEX Inc.

- Corpay (Fleetcor)

- AirPlus International

- Revolut Ltd.

- Brex Inc.

- Adyen NV

- Citi (Citigroup Inc.)

- BMO Financial Group

- MineralTree Inc.

- Billtrust Inc.

- Fraedom Holdings Ltd.

- Coupa

- Tribal Credit

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in B2B virtual card adoption for AP automation

- 4.2.2 E-commerce boom propelling remote-payment virtual cards

- 4.2.3 Regulatory push for cash-lite economies & open banking

- 4.2.4 Superior fraud-protection versus physical cards

- 4.2.5 Embedded-finance APIs integrating virtual cards in SaaS

- 4.2.6 Tokenisation enabling IoT machine-to-machine payments

- 4.3 Market Restraints

- 4.3.1 Supplier acceptance gaps & interchange cost concerns

- 4.3.2 Connectivity / ERP-integration complexity

- 4.3.3 Limited cross-border acceptance networks

- 4.3.4 Instant-payment rails cannibalising card volumes

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Use

- 5.1.1 Single-Use

- 5.1.2 Multi-Use

- 5.2 By Payment Type

- 5.2.1 Remote Payments

- 5.2.2 POS Payments

- 5.3 By End User

- 5.3.1 Consumer

- 5.3.2 Business

- 5.4 By Card Type

- 5.4.1 Virtual Debit Card

- 5.4.2 Virtual Credit Card

- 5.4.3 Virtual Prepaid Card

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Peru

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Benelux (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 American Express Company

- 6.4.2 Mastercard Incorporated

- 6.4.3 Visa Inc.

- 6.4.4 JPMorgan Chase & Co.

- 6.4.5 Marqeta Inc.

- 6.4.6 Stripe Inc.

- 6.4.7 PayPal Holdings Inc.

- 6.4.8 WEX Inc.

- 6.4.9 Corpay (Fleetcor)

- 6.4.10 AirPlus International

- 6.4.11 Revolut Ltd.

- 6.4.12 Brex Inc.

- 6.4.13 Adyen NV

- 6.4.14 Citi (Citigroup Inc.)

- 6.4.15 BMO Financial Group

- 6.4.16 MineralTree Inc.

- 6.4.17 Billtrust Inc.

- 6.4.18 Fraedom Holdings Ltd.

- 6.4.19 Coupa

- 6.4.20 Tribal Credit

7 Market Opportunities & Future Outlook

- 7.1 Expansion of Virtual Cards in Emerging Markets

- 7.2 Integration of Virtual Cards with Advanced Security Technologies