PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066654

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066654

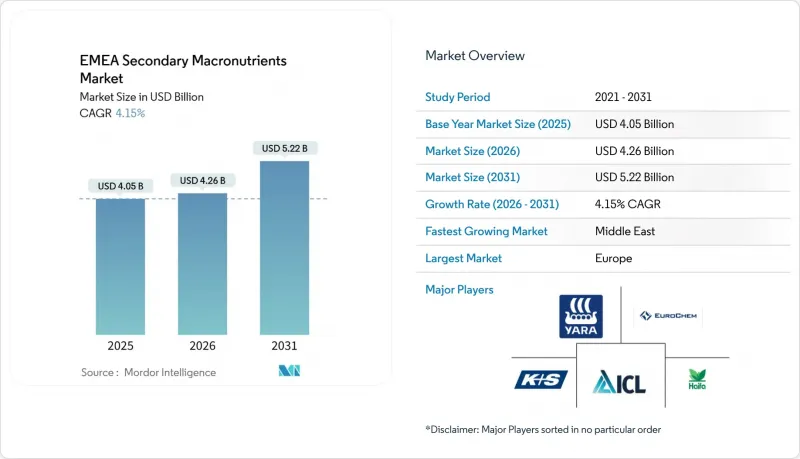

EMEA Secondary Macronutrients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the eMEA secondary macronutrients market size was valued at USD 4.05 billion in 2025 and estimated to grow from USD 4.26 billion in 2026 to reach USD 5.22 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031).

This report is Segmented by Nutrient Type (Sulfur, Calcium, and Magnesium), by Application Method (Solid, and Liquid), by Crop Type (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, Turf and Ornamentals, and Other Crop Types), and by Geography (Europe, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

EMEA Secondary Macronutrients Market Trends and Insights

European Union Green Deal Pushing Balanced Fertilization Compliance

The European Commission targets a 20% drop in nutrient losses by 2030, and national regulators have extended compliance auditing to include sulfur, calcium, and magnesium. The February 2026 RENURE amendment lets processed manure qualify as high quality fertilizer, tightening synthetic nitrogen ceilings and raising demand for high-efficiency secondary macronutrients that deliver crop-specific doses without breaching nitrogen caps. Germany now mandates soil tests every six years, steering growers toward calcium ammonium nitrate blends containing 4% magnesium oxide. This policy triad combines cash incentives, legal requirements, and residue scrutiny to accelerate balanced nutrient adoption throughout the EMEA secondary macronutrients market.

Magnesium Deficiency Issues Under LED Horticulture Lighting

Light-emitting diode arrays shift crop physiology and raise magnesium demand. A 2025 study showed diffusive greenhouse covers boosted calcium and magnesium in asparagus spears, and Dutch tomato growers recorded classic magnesium deficiency interveinal chlorosis in older leaves within weeks of converting from high-pressure sodium lamps. Israel increased magnesium guidelines by 15-20% for LED-lit crops. Haifa Group reformulated Magnisal with a higher magnesium-to-nitrogen ratio, and K+S promotes kieserite as a slow-release option for open fields. Because magnesium drives chlorophyll synthesis, quality-minded greenhouse producers see immediate visual gains from balanced feeds, fueling segment acceleration within the EMEA secondary macronutrients market.

Preference for NPK Bulk Blends Over Standalone Secondary Nutrients

The increasing preference for NPK bulk blends over standalone secondary nutrients is limiting the growth of the EMEA secondary macronutrients market. This trend reduces the direct consumption of individual products such as sulfur, calcium, and magnesium. Farmers are opting for blended fertilizers that combine nitrogen (N), phosphorus (P), and potassium (K) with secondary nutrients in a single application. This approach simplifies farming operations, reduces labor costs, and ensures balanced nutrient delivery. Consequently, the demand for separately applied secondary macronutrient products is declining, particularly in large-scale farming systems where efficiency and cost optimization are priorities.

Other drivers and restraints analyzed in the detailed report include:

- Oil and Gas Desulfurization Creating Low-Cost Elemental Sulfur

- Digital Variable-Rate Technology Boosting Site-Specific Use

- Rising Demand for Organic Produce Limiting Synthetic Fertilizer Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sulfur held the largest segment, 46.0% of the EMEA secondary macronutrients market size in 2025, reflecting its dual role as protein-synthesis catalyst and soil-pH corrector in alkaline zones across Spain, Morocco, and Egypt. Sulfur's role in enhancing chlorophyll formation and improving nitrogen use efficiency makes it essential for crops like oilseeds and cereals, where its deficiency can adversely affect yield and quality. The widespread sulfur deficiency in intensively cultivated soils across Europe has significantly increased demand for sulfur. Continuous cropping practices and reduced atmospheric sulfur deposition have depleted natural soil sulfur levels, prompting farmers to increasingly adopt sulfur-based fertilizers to restore nutrient balance and sustain soil productivity.

Magnesium is the fastest-growing, projected to grow at a 6.9% CAGR through 2026-2031, driven by LED lighting in greenhouses, which alters magnesium uptake kinetics. Calcium stays pivotal because greenhouse tomatoes and peppers rely on calcium nitrate to prevent blossom-end rot without adding nitrate to already saturated feeding schedules. Together, the three nutrients illustrate a mix of volume stability for sulfur and value-based upside for magnesium and calcium.

List of Companies Covered in this Report:

- Yara International ASA

- EuroChem Group AG

- ICL Group

- K+S AG

- Haifa Group

- Al-Tayseer Chemical Industry

- Saudi United Fertilizer Company (Al-Asmida)

- SAF Sulphur Company

- Trade Corporation International SA

- SQM

- OCP Group

- Ma'aden Phosphate Company

- Toros Tarim

- Balchem Corporation

- Nufarm Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soil sulfur depletion in high-yield European cereal belts

- 4.2.2 European Union Green Deal pushing balanced fertilization compliance

- 4.2.3 Expansion of controlled-environment agriculture in GCC countries

- 4.2.4 Magnesium deficiency issues under LED horticulture lighting

- 4.2.5 Oil and gas desulfurization creating plentiful low-cost elemental sulfur

- 4.2.6 Digital variable-rate technology boosting site-specific secondary nutrient use

- 4.3 Market Restraints

- 4.3.1 Preference for NPK bulk blends over standalone secondary nutrients

- 4.3.2 Premium pricing for liquid calcium and magnesium formulations

- 4.3.3 Rising demand for organic produce limiting synthetic fertilizer use

- 4.3.4 Supply-chain volatility for sulfur linked to refining capacity cuts

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Nutrient Type

- 5.1.1 Sulfur

- 5.1.2 Calcium

- 5.1.3 Magnesium

- 5.2 By Application Method

- 5.2.1 Solid

- 5.2.2 Liquid

- 5.3 By Crop Type

- 5.3.1 Grains and Cereals

- 5.3.2 Pulses and Oilseeds

- 5.3.3 Fruits and Vegetables

- 5.3.4 Turf and Ornamentals

- 5.3.5 Other Crop Types

- 5.4 By Geography

- 5.4.1 Europe

- 5.4.1.1 Germany

- 5.4.1.2 United Kingdom

- 5.4.1.3 France

- 5.4.1.4 Italy

- 5.4.1.5 Spain

- 5.4.1.6 Russia

- 5.4.1.7 Rest of Europe

- 5.4.2 Middle East

- 5.4.2.1 United Arab Emirates

- 5.4.2.2 Saudi Arabia

- 5.4.2.3 Kuwait

- 5.4.2.4 Egypt

- 5.4.2.5 Rest of Middle East

- 5.4.3 Africa

- 5.4.3.1 South Africa

- 5.4.3.2 Morocco

- 5.4.3.3 Nigeria

- 5.4.3.4 Rest of Africa

- 5.4.1 Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for key Companies, Products and Services, and Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 EuroChem Group AG

- 6.4.3 ICL Group

- 6.4.4 K+S AG

- 6.4.5 Haifa Group

- 6.4.6 Al-Tayseer Chemical Industry

- 6.4.7 Saudi United Fertilizer Company (Al-Asmida)

- 6.4.8 SAF Sulphur Company

- 6.4.9 Trade Corporation International SA

- 6.4.10 SQM

- 6.4.11 OCP Group

- 6.4.12 Ma'aden Phosphate Company

- 6.4.13 Toros Tarim

- 6.4.14 Balchem Corporation

- 6.4.15 Nufarm Limited

7 Market Opportunities and Future Outlook