PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066702

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066702

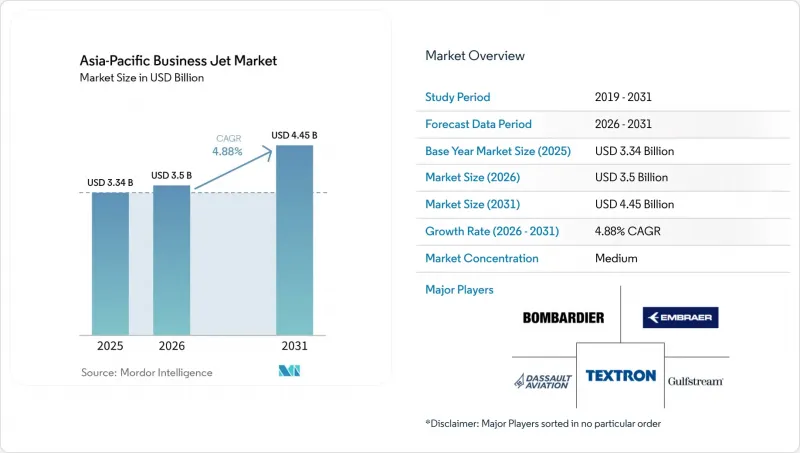

Asia-Pacific Business Jet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific business jet market size is expected to grow from USD 3.34 billion in 2025 to USD 3.50 billion in 2026 and is forecasted to reach USD 4.45 billion by 2031 at a 4.88% CAGR over 2026-2031.

This report is Segmented by Body Type (Large Jet, Mid-Size Jet, and Light/Very-Light Jet), End User (Individual Owners, Businesses and Corporate Entities, Charter/Air-Taxi Operators, and More), Ownership Model (New Aircraft Purchase, Pre-Owned Purchase, and More), and Geography (China, India, Japan, Singapore, Australia, Malaysia and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Business Jet Market Trends and Insights

Rising HNWI and Corporate Wealth in Asia-Pacific

Corporate and private-client travel patterns across the region are increasingly anchored to time savings and schedule control. A survey of Asian organizations reported that 63% of corporate executives now use business aviation for work trips, rising to 69% among private equity, hedge funds, and family offices. Users cited time savings of 2 to 3 hours per journey compared with commercial travel, reinforcing the productivity case for expanding the fleet and using charters. These behavioral shifts align with the projected growth of the Asia-Pacific business jet market as more enterprise users embed point-to-point access into routine itineraries. As private capital and corporate treasuries prioritize reliability, flight departments and charter providers evolve away from discretionary spending cycles toward embedded solutions. The result is a more resilient demand baseline that supports utilization and renewal across the Asia-Pacific business jet market.

Post-COVID Surge in Point-to-Point Charter Demand

Charter demand has moved from recovery to structure, with operators designing networks for short regional missions that bypass airline hubs. Singapore's Changi and Seletar airports recorded business jet departures nearly 28% higher in 2023 compared with 2019, which signals a durable shift toward private lift for time-critical travel in congested corridors. Digital programs are adding flexibility as well, with membership growth in Asia and higher transaction volumes on app-based marketplaces that connect travelers to globally distributed fleets. Together, these changes have raised the practical utility of on-demand flying for corporate teams that value predictability over published airline schedules. This behavioral pivot underpins a broader trend of increased utilization in the Asia-Pacific business jet market as network density builds across secondary city pairs.

High Acquisition and Operating Costs plus FX Volatility

Aircraft purchase and lifecycle costs are primarily denominated in USD, while many operator revenues accrue in local currencies, which elevates financial exposure during procurement and operations. Insurance, spares, and maintenance programs are also linked to USD benchmarks, which limits the ability to localize costs and makes planning sensitive to currency swings. Fiscal measures, such as import duties and luxury taxes in select markets, add to delivered prices, which can deter balance-sheet ownership among mid-sized enterprises. These dynamics have supported the rise of asset-light access models that shift capital and residual risk to operators. They also encourage pre-owned acquisition, where the lower price point can offset higher maintenance costs later in the asset's life. Taken together, these headwinds moderate the pace of new-aircraft absorption in parts of the Asia-Pacific business jet market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of FBO and MRO Infrastructure

- Fleet-Modernization Programs of Charter Operators

- Asia-Pacific Pilot-Shortage Bottleneck

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large jets accounted for 47.62% in 2025, reflecting sustained intercontinental mission needs among corporates and ultra-high-net-worth owners in the Asia-Pacific business jet market. Platform roadmaps continue to reinforce this segment with cabin, range, and connectivity advances that keep long-haul travel productive for executive teams. Purchase and crewing economics favor a diversified approach in markets where domestic and short regional missions dominate.

Light and very-light jets are projected to grow the fastest at a 6.12% CAGR through 2031, supported by shorter stage lengths and the need to access secondary airports with tighter operating windows. New-generation avionics and cabin systems also help reduce crew workload, which is a practical advantage in a tight labor market. The Asia-Pacific business jet industry is therefore balancing capability at the top of the range with higher-frequency deployments on shorter legs. Refresh cycles in the light and super-midsize categories add margin benefits from lower fuel burn and streamlined maintenance events. As operators harmonize fleets around these missions, reliability and access improve on high-density routes between secondary city pairs.

The adoption profile in light and super-midsize categories reflects a consistent push for better economics without sacrificing comfort or connectivity. Incremental upgrades to OEM portfolios support these goals by reducing direct operating costs and delivering modern cabins that meet client expectations. For charter, the ability to right-size aircraft to mission length improves pricing and expands the addressable client base. For corporate flight departments, flexibility across intra-country and regional trips reduces reliance on airline schedules and improves schedule control. These dynamics underpin the fastest growth outlook for light and very-light jets in the Asia-Pacific business jet market. At the same time, large-cabin capability remains essential for transcontinental and trans-Pacific missions. The Asia-Pacific business jet industry will continue to optimize mixes as operators replace older airframes and leverage the latest platform features.

List of Companies Covered in this Report:

- Airbus SE

- Bombardier Inc.

- Cirrus Design Corporation (Aviation Industry Corporation of China)

- Dassault Aviation S.A.

- Embraer S.A.

- Gulfstream Aerospace Corporation (General Dynamics Corporation)

- Honda Aircraft Company (Honda Motor Co., Ltd.)

- Pilatus Aircraft Ltd.

- Textron Inc.

- The Boeing Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 KEY INDUSTRY TRENDS

- 4.1 High-Net-Worth Individual (HNWI) Population Trend

5 MARKET LANDSCAPE

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Rising HNWI and corporate wealth in Asia-Pacific

- 5.2.2 Post-COVID surge in point-to-point charter demand

- 5.2.3 Expansion of FBO and MRO infrastructure

- 5.2.4 Fleet-modernization programs of charter operators

- 5.2.5 Liberalization of secondary-airport night slots (ASEAN)

- 5.2.6 Time-critical cross-border e-commerce executive travel

- 5.3 Market Restraints

- 5.3.1 High acquisition and operating costs plus FX volatility

- 5.3.2 Asia-Pacific pilot-shortage bottleneck

- 5.3.3 Import duties and luxury taxes in emerging Asia-Pacific markets

- 5.3.4 Environmental opposition and potential slot curbs

- 5.4 Value Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces Analysis

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Suppliers

- 5.7.3 Bargaining Power of Buyers

- 5.7.4 Threat of Substitutes

- 5.7.5 Intensity of Competitive Rivalry

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Body Type

- 6.1.1 Large Jet

- 6.1.2 Mid-Size Jet

- 6.1.3 Light/Very-Light Jet

- 6.2 By End User

- 6.2.1 Individual Owners

- 6.2.2 Businesses and Corporate Entities

- 6.2.3 Charter/Air-Taxi Operators

- 6.2.4 Training and Academic Institutions

- 6.2.5 Government and Special-Mission Operators

- 6.3 By Ownership Model

- 6.3.1 New Aircraft Purchase

- 6.3.2 Pre-Owned Purchase

- 6.3.3 Fractional Ownership

- 6.3.4 Jet Cards/Membership

- 6.4 By Geography

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 India

- 6.4.4 Singapore

- 6.4.5 Australia

- 6.4.6 Malaysia

- 6.4.7 South Korea

- 6.4.8 Indonesia

- 6.4.9 Thailand

- 6.4.10 Philippines

- 6.4.11 Rest of Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 Airbus SE

- 7.4.2 Bombardier Inc.

- 7.4.3 Cirrus Design Corporation (Aviation Industry Corporation of China)

- 7.4.4 Dassault Aviation S.A.

- 7.4.5 Embraer S.A.

- 7.4.6 Gulfstream Aerospace Corporation (General Dynamics Corporation)

- 7.4.7 Honda Aircraft Company (Honda Motor Co., Ltd.)

- 7.4.8 Pilatus Aircraft Ltd.

- 7.4.9 Textron Inc.

- 7.4.10 The Boeing Company

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-space and Unmet-Need Assessment