PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066707

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066707

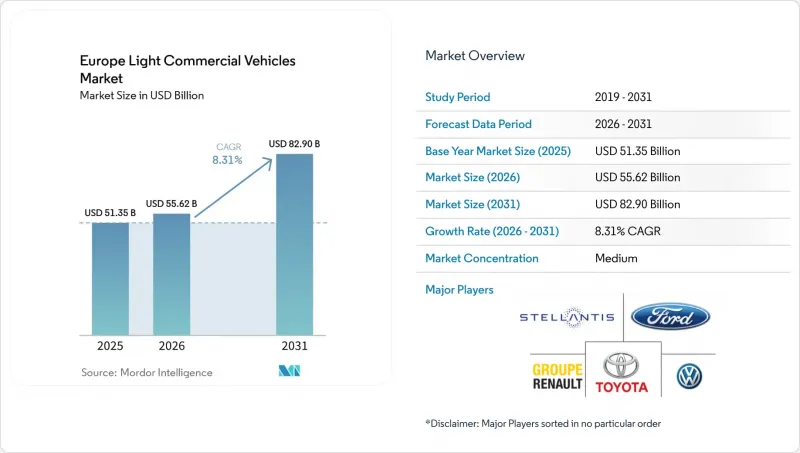

Europe Light Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the european light commercial vehicles market size is expected to grow from USD 51.35 billion in 2025 to USD 55.62 billion in 2026 and is forecast to reach USD 82.90 billion by 2031 at an 8.31% CAGR over 2026-2031.

This report is Segmented by Vehicle Type (Light Commercial Vans, Light Pick-Up Trucks, Chassis-Cab, and More), Gross Vehicle Weight (Less Than 2. 0 T, and More), Propulsion Type (BEV, PHEV, HEV, FCEV, ICE), End-Use Industry (Urban Last-Mile, and More), Ownership Type (Corporate, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Europe Light Commercial Vehicles Market Trends and Insights

E-Commerce-Driven Last-Mile Delivery Boom

Parcel volumes in Europe are projected to continue growing, driven by e-commerce and same-day delivery demand. Leading markets such as Germany, the UK, and France each handle several billion parcels annually, with overall European parcel volumes expected to increase steadily year-on-year. Logistics operators respond by adding zero-emission vans that secure unrestricted access to the city center. Amazon is committed to deploying 10,000 electric delivery vans across Germany, France, and Spain by the end of 2026, following agreements with Rivian and Mercedes-Benz. Quick-commerce firms such as Getir and Gorillas prefer sub-2.0-ton micro-vans, reinforcing double-digit growth in that weight class. Retailers continue to offer in-house delivery to protect brand experience, creating captive demand for purpose-built electric LCVs pre-equipped with telematics and route-optimization software.

Stricter EU CO2 and NOx Limits for City Access

The EU's CO2 emission performance standards regulation (Regulation (EU) 2019/631) requires that the average CO2 emissions of new vans (light commercial vehicles) be reduced by approximately 50 % by 2030 compared to 2021 levels, under current law. OEMs are front-loading battery electric launches, for instance, Stellantis released the Peugeot e-Partner and Citroen e-Berlingo in March 2025, targeting tradespeople traversing daily low-emission zones. London expanded its Ultra-Low Emission Zone to all 32 boroughs in August 2025, imposing a GBP 12.50 daily charge on non-compliant vans, accelerating fleet replacement cycles. Paris enforced a diesel van ban within the Peripherique in January 2025, while Euro 7 standards, coming in 2027, mandate real-world emissions tests that further shift economics toward zero-emission powertrains.

Up-Front EV Van Cost Premium

A mid-size BEV van in 2025 carried a EUR 12,000-18,000 premium over diesel, shrinking to EUR 8,000-10,000 after incentives, yet still deterring SMEs in Eastern Europe with limited access to low-cost credit. Poland's electric LCV registrations rose only 9% in 2025, compared with 34% in Germany, mirroring weaker subsidy structures. Battery-as-a-service contracts reduce purchase prices by EUR 6,000-8,000 but add monthly fees, leaving rural operators with lower mileage outside the break-even range.

Other drivers and restraints analyzed in the detailed report include:

- Government Fleet-Renewal Incentives and Scrappage

- Proliferation of Urban Low-Emission Zones (LEZs)

- Semiconductor and Battery-Cell Supply Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Light commercial vans captured 46.11% of Europe's light commercial vehicle market share in 2025, anchored by familiar box-van formats that now ship with standardized 50-80 kWh battery packs capable of 240-300 km real-world range. The category is forecast to post an 18.67% CAGR through 2031 as postal services and courier companies lock in bulk orders that lower pack costs by a further 14%. Pick-ups serving construction and agriculture remain dominated by diesel, yet electric variants are entering pilot trials as bidirectional-power sockets enable on-site tool use. Micro-LCVs such as the Citroen Ami Cargo tripled registrations in 2025 and now appeal to quick-commerce firms that value ease of curbside parking.

Platform-cab and chassis-cab variants accounted for 18% of volume, with body-in-white designs that simplify upfitting for refrigeration, mobile workshops, or tipper beds. Modular architectures adopted by Stellantis cut body-swap lead times to 6-8 weeks, half the industry average, allowing fleets to redeploy chassis across duty cycles. Homologation under EU Whole Vehicle Type Approval continues to add 6-9 months for niche bodies, although digital twins and virtual testing are shortening physical crash-validation phases.

The 2.6-3.0 ton class accounted for 41.34% of Europe's light commercial vehicle market in 2025, offering the best payload-to-range compromise for urban and peri-urban logistics. Operators appreciate that drivers can operate these vans with standard Category B licenses, eliminating the need for additional training or higher wages. Sub-2.0-ton vans, while smaller, are growing at a 12.28% CAGR to 2031 as quick-commerce firms require agile platforms able to slip through congestion-charge windows without weight-based toll surcharges.

The 3.1-3.5 ton bracket supports furniture delivery and light construction, yet diesel still commands 78% share, given energy-density limitations for battery packs at higher curb weights. CATL's shift toward cost-efficient LFP chemistry now supplies Renault and Nissan, trimming pack pricing by 15-20% and starting to make electric adoption viable in the mid-weight segment.

List of Companies Covered in this Report:

- Stellantis N.V.

- Ford Motor Company

- Renault Group

- Mercedes-Benz Group AG

- Volkswagen AG

- Toyota Motor Corporation

- Iveco Group N.V.

- Nissan Motor Co., Ltd.

- MAN Truck & Bus SE

- SAIC Motor - Maxus

- Hyundai Motor Company

- Arrival Ltd.

- Isuzu Motors Ltd.

- Mitsubishi Fuso Truck & Bus Corp.

- DFSK Motor

- Rivian Automotive, Inc.

- StreetScooter GmbH

- Volta Trucks AB

- Opel Automobile GmbH

- Piaggio Commercial Vehicles

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Key Industry Trend

- 4.1 Urbanization, Population and Vehicle/Transit Demand

- 4.2 Fuel vs Electricity Price Spread (Per km, ICE vs EV)

- 4.3 EV vs ICE Total Cost of Ownership (TCO) Gap

- 4.4 Financing and Ownership Models (Loans, Leasing, Subscription)

- 4.5 Battery Chemistry Mix and Pack Energy Density (LFP vs NMC)

- 4.6 Home, Workplace and Public Charger Access/Density

- 4.7 Fast-Charging Network Coverage and Power Bands

- 4.8 Alternative Fuels Infrastructure (Hydrogen for FCEVs)

- 4.9 Subsidy and Consumer Incentive Value (Purchase, Tax, Toll/Parking Benefits)

- 4.10 OEM EV Line-up and Model Pipeline

- 4.11 Value-Chain and Distribution-Channel Analysis

- 4.12 Regulatory, Fiscal and Industrial Policy Framework

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 E-Commerce-Driven Last-Mile Delivery Boom

- 5.2.2 Stricter EU CO2 and NOx Limits for City Access

- 5.2.3 Government Fleet-Renewal Incentives and Scrappage

- 5.2.4 Proliferation of Urban Low-Emission Zones (LEZs)

- 5.2.5 Modular Up-Fitting Platforms Enabling Quick Body Swaps

- 5.2.6 Vehicle-to-Grid (V2G) Revenue Stacks Enhancing TCO

- 5.3 Market Restraints

- 5.3.1 Up-Front EV Van Cost Premium

- 5.3.2 Semiconductor and Battery-Cell Supply Constraints

- 5.3.3 Payload Penalties from Heavy Battery Packs

- 5.3.4 Slow Homologation Cycles for Fuel-Cell LCVs

- 5.4 Value/Supply-Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Suppliers

- 5.7.3 Bargaining Power of Buyers

- 5.7.4 Threat of Substitutes

- 5.7.5 Competitive Rivalry

6 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 6.1 By Vehicle Type

- 6.1.1 Light Commercial Vans

- 6.1.2 Light Pick-up Trucks (Less than 3.5 t GVW)

- 6.1.3 Chassis-Cab / Platform Cab

- 6.1.4 Mini-Trucks / Micro-LCVs

- 6.1.5 Minibuses (Less than 20 seats)

- 6.2 By Gross Vehicle Weight (GVW) Class

- 6.2.1 Less than 2.0 t

- 6.2.2 2.1 to 2.5 t

- 6.2.3 2.6 to 3.0 t

- 6.2.4 3.1 to 3.5 t

- 6.2.5 3.6 to 5.0 t

- 6.3 By Propulsion Type

- 6.3.1 BEV (Battery Electric Vehicle)

- 6.3.2 PHEV (Plug-in Hybrid Electric Vehicle)

- 6.3.3 HEV (Hybrid Electric Vehicle)

- 6.3.4 FCEV (Fuel Cell Electric Vehicle)

- 6.3.5 ICE (Internal Combustion Engine)

- 6.4 By End-Use Industry

- 6.4.1 Urban Last-Mile Delivery and Courier

- 6.4.2 Utilities and Field Services

- 6.4.3 Construction and Building Supplies

- 6.4.4 Postal and Parcel

- 6.4.5 Agriculture and Rural Services

- 6.4.6 Mobile Workshops and Special Purpose

- 6.5 By Ownership/Fleet Type

- 6.5.1 Corporate Fleets

- 6.5.2 SME Fleets

- 6.5.3 Self-Employed/Sole Proprietors

- 6.5.4 Rental and Leasing Companies

- 6.5.5 Government and Municipal Fleets

- 6.6 By Country

- 6.6.1 Austria

- 6.6.2 Belgium

- 6.6.3 Czech Republic

- 6.6.4 Denmark

- 6.6.5 Estonia

- 6.6.6 France

- 6.6.7 Germany

- 6.6.8 Ireland

- 6.6.9 Italy

- 6.6.10 Latvia

- 6.6.11 Lithuania

- 6.6.12 Norway

- 6.6.13 Poland

- 6.6.14 Russia

- 6.6.15 Spain

- 6.6.16 Sweden

- 6.6.17 United Kingdom

- 6.6.18 Rest of Europe

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 Stellantis N.V.

- 7.4.2 Ford Motor Company

- 7.4.3 Renault Group

- 7.4.4 Mercedes-Benz Group AG

- 7.4.5 Volkswagen AG

- 7.4.6 Toyota Motor Corporation

- 7.4.7 Iveco Group N.V.

- 7.4.8 Nissan Motor Co., Ltd.

- 7.4.9 MAN Truck & Bus SE

- 7.4.10 SAIC Motor - Maxus

- 7.4.11 Hyundai Motor Company

- 7.4.12 Arrival Ltd.

- 7.4.13 Isuzu Motors Ltd.

- 7.4.14 Mitsubishi Fuso Truck & Bus Corp.

- 7.4.15 DFSK Motor

- 7.4.16 Rivian Automotive, Inc.

- 7.4.17 StreetScooter GmbH

- 7.4.18 Volta Trucks AB

- 7.4.19 Opel Automobile GmbH

- 7.4.20 Piaggio Commercial Vehicles

8 Market Opportunities and Future Outlook

- 8.1 White-Space and Unmet-Need Assessment