PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066709

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066709

Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

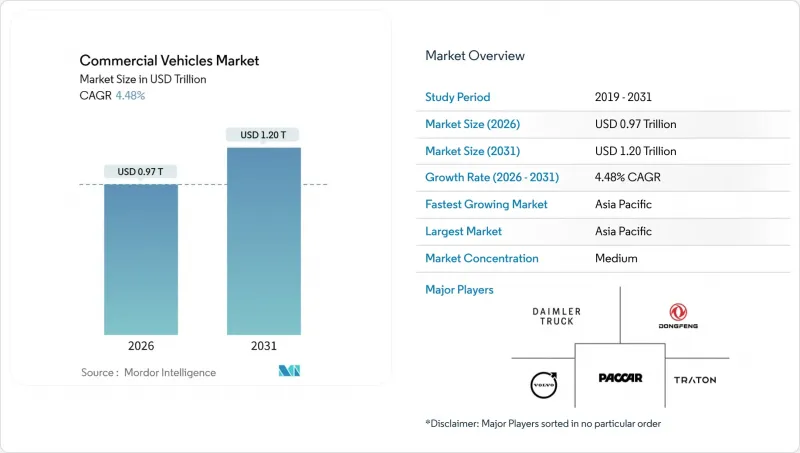

According to Mordor Intelligence, the commercial vehicles market size reached USD 0.97 trillion in 2026 and is projected to climb to USD 1.20 trillion by 2031, advancing at a 4.48% CAGR over the forecast period.

This report is Segmented by Vehicle Type (Buses, Heavy-Duty Commercial Trucks, and More), Propulsion Type (Hybrid and Electric Vehicles, Internal Combustion Engine), Gross Vehicle Weight Rating (Class 1, Class 2, and More), End-Use Industry (Logistics and E-Commerce, Construction and Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Commercial Vehicles Market Trends and Insights

Tightening CO2 and NOx Emission Limits in the United States, EU and China

After 2024, governments ramped up stringent carbon regulations, shortening OEM development timelines and increasing compliance expenses. However, subsidies and tax credits are now offsetting the total ownership costs for zero-emission trucks. The new EPA Phase 3 targets mandate reduced CO2 emissions for 2027 heavy-duty vehicle models. Meanwhile, Europe's clean-transport corridors are set to install megawatt chargers at regular intervals. In China, the extension of stricter emission standards to larger trucks has significantly reduced NOx emissions, leading to the premature retirement of non-compliant diesel units. Fleet operators in California and Germany have made long-term commitments to electric truck purchases, valuing regulatory clarity over the challenges of early infrastructure deployment. As a result, initiatives like subsidized capital expenditures and carbon pricing are propelling the commercial vehicles market upward.

Explosive E-commerce and 3PL Growth Requiring Last-mile Fleets

As parcel volumes surged, outpacing the pace of warehouse automation, logistics firms found themselves compelled to electrify their light-duty vans, especially those operating in urban zero-emission zones. Amazon has rolled out a substantial fleet of electric vans across North America and Europe by the end of 2025. Meanwhile, DHL has committed significant investments, aiming to electrify a majority of its urban fleet in the coming years. In response to municipal diesel restrictions in cities like London, Paris, and Beijing, which curtail peak-hour access for internal combustion engine (ICE) vans, electric vans are increasingly becoming a preferred choice for urban delivery vehicles in Europe. While the United States trails in adoption-attributed to its longer suburban routes and a sparse network of chargers-pilot programs in Los Angeles and New York have showcased that depot charging can effectively support daily operational cycles. These developments highlight a robust and growing demand for electrified light-duty vehicles in the commercial vehicles market.

Grid-connection Delays (Above 24 Months) for 5 MW Depot Chargers

Fleet electrification timelines are being stretched by utility backlogs. In the United Kingdom, connection requests face significant delays. Meanwhile, in California, larger projects often encounter extended waiting periods. Substation upgrades are hindered by transformer shortages and a regulatory sequence that prioritizes residential solar tie-ins. In Germany, while co-funding is available for infrastructure, the disbursement process is slow, with any relief not expected in the near term. Unless utilities expedite approvals or regulators enforce fast-track queues, depot electrification will continue to lag, dampening the near-term potential for the commercial vehicles market.

Other drivers and restraints analyzed in the detailed report include:

- Record Low Battery-pack USD/kWh Unlocking HD-truck Parity

- Megawatt-charging Corridor Pilots on I-5 and Rhine-Alpine

- Insurance-premium Spike for BEV Trucks in North America and EU (Above 35%)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Heavy-duty trucks, despite a 42.15% 2025 volume share, shoulder payload and range constraints that keep diesel dominant until megawatt chargers proliferate. Medium-duty units await infrastructure clarity, while buses depend on municipal budgets and political cycles. Pick-up trucks remain mostly gasoline in rural North America, although pilot fleets featuring Ford F-150 Lightning and Rivian variants signal an early transition in utilities and construction. Light commercial vans grew fastest, propelled by parcel density and city-center emission rules. Vans require 150-200 kWh packs-less than those of heavy-duty trucks-supporting three-year payback horizons even before fuel levies. The commercial vehicles market size for light vans is set to expand at a 6.24% CAGR, outpacing bus and medium-duty segments.

European zero-emission zones accelerate van adoption by banning diesel deliveries during peak hours, and subsidies shorten payback in urban operations. North America's longer routes retain diesel dominance, yet pilot data suggest depot charging can sustain daily range needs. Heavy-duty truck growth hinges on battery-cost curves and corridor charging funding, meaning vans will be the workhorse of commercial vehicles market expansion through 2031.

Internal-combustion engines kept 69.03% of 2025 revenue in the commercial vehicles market, but hybrid and electric variants log an 8.33% CAGR, signaling structural rebalancing. Battery-electric leads electrification, while plug-in hybrids bridge infrastructure gaps for cautious fleets. Diesel engines face nickel-moly inflation and regulatory complexity, eroding cost advantages. CNG persists in refuse and transit fleets with central refueling, yet growth stays modest as electric TCO declines. Gasoline and LPG fade under urban restrictions.

Battery-electric uptake varies by region: China and Europe advance fastest via subsidies and access rules; North America electrifies urban delivery while preserving diesel for long haul; emerging markets delay until chargers proliferate. Fuel-cell pilots progress for long-range duty cycles, but high hydrogen costs stall scale-up. The propulsion mix through 2031 will pivot on policy timing and battery-density milestones, reshaping supply chains in the commercial vehicles market.

Geography Analysis

Asia-Pacific generated 46.25% of global revenue in 2025 and will post a 7.74% CAGR, the highest worldwide in the commercial vehicles market. China leads with 1.2 million electric commercial vehicles produced by BYD, SAIC Motor, and Foton Motor, benefiting from purchase-tax waivers and battery-swap corridors. India's FAME-II extensions spur light-duty electrification in top metros, while Japan and South Korea double down on hydrogen heavy-duty pilots. Southeast Asia attracts Chinese assembly plants, yet slower infrastructure roll-outs limit penetration.

Europe advances on the strength of Germany's significant charger fund and expanding zero-emission zones . France and the United Kingdom restrict diesel van access to city centers, boosting van electrification but straining urban grids. Southern Europe trails in infrastructure and fiscal leeway, though incentives through 2026 aim to narrow the gap. Russia remains mostly diesel amid sanctions, and harsh winters degrade battery efficiency.

North America is bifurcated: California and the Northeast push zero-emission mandates, while the Midwest keeps diesel for long haul. Canada's federal rebates spark adoption in Ontario and Quebec, yet rural distances mute impact. Brazil and Argentina pilot electric buses, but most freight stays diesel until charging costs fall. The Middle East and Africa show early interest in logistics free zones, but oil economies and nascent infrastructure delay meaningful share shifts. Collectively, Asia-Pacific and Europe will drive the commercial vehicles market expansion, while North America and emerging regions catch up post-2028.

- Daimler Truck AG

- Volvo Group

- PACCAR Inc.

- Traton SE

- Dongfeng Motor Corporation Ltd.

- Tata Motors Limited

- BYD Auto Co., Ltd.

- SAIC Motor Corporation Limited

- Ford Motor Company

- General Motors Company

- Toyota Motor Corporation

- Hyundai Motor Company

- Nissan Motor Co., Ltd.

- Mahindra & Mahindra Ltd.

- Renault Group

- Rivian Automotive Inc.

- Iveco Group N.V.

- Isuzu Motors Ltd.

- Beiqi Foton Motor Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Key Industry Trend

- 4.1 Urbanization, Population and Vehicle/Transit Demand

- 4.2 EV Penetration in Commercial Vehicle

- 4.3 Fuel vs Electricity Price Spread (Per km, ICE vs EV)

- 4.4 EV vs ICE Total Cost of Ownership (TCO) Gap

- 4.5 Financing and Ownership Models (Loans, Leasing, Subscription)

- 4.6 Battery Chemistry Mix and Pack Energy Density (LFP vs NMC etc.)

- 4.7 Home, Workplace and Public Charger Access / Density

- 4.8 Fast-Charging Network Coverage and Power Bands

- 4.9 Alternative Fuels Infrastructure (Hydrogen for FCEVs)

- 4.10 Subsidy and Consumer Incentive Value

- 4.11 OEM EV Line-up and Model Pipeline

- 4.12 Value-Chain and Distribution-Channel Analysis

- 4.13 Regulatory, Fiscal and Industrial Policy Framework

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Tightening CO2 and NOx Emission Limits in the United States, EU and China

- 5.2.2 Explosive E-commerce and 3PL Growth Requiring Last-mile Fleets

- 5.2.3 Record Low Battery-pack USD/kWh Unlocking HD-truck Parity

- 5.2.4 Megawatt-charging Corridor Pilots on I-5 and Rhine-Alpine

- 5.2.5 Commercial Battery-swap Ecosystems Proven in China's Mining Hubs

- 5.2.6 OEM Battery-as-a-Service (BaaS) Subscription Rollout

- 5.3 Market Restraints

- 5.3.1 Grid-connection Delays (Above 24 Months) for 5 MW Depot Chargers

- 5.3.2 Insurance-premium Spike for BEV Trucks in North America and EU (Above 35%)

- 5.3.3 Residual-value Uncertainty for First-gen Electric HD Trucks

- 5.3.4 Rising Nickel and Moly Surcharges Inflating Diesel Powertrain Costs

- 5.4 Value / Supply-Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces

- 5.7.1 Bargaining Power of Suppliers

- 5.7.2 Bargaining Power of Buyers

- 5.7.3 Threat of New Entrants

- 5.7.4 Threat of Substitutes

- 5.7.5 Competitive Rivalry

6 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 6.1 By Vehicle Type

- 6.1.1 Buses

- 6.1.2 Heavy-Duty Commercial Trucks

- 6.1.3 Medium-Duty Commercial Trucks

- 6.1.4 Light Commercial Pick-up Trucks

- 6.1.5 Light Commercial Vans

- 6.2 By Propulsion Type

- 6.2.1 Hybrid and Electric Vehicles

- 6.2.1.1 Battery Electric Vehicle (BEV)

- 6.2.1.2 Fuel Cell Electric Vehicle (FCEV)

- 6.2.1.3 Hybrid Electric Vehicle (HEV)

- 6.2.1.4 Plug-in Hybrid Electric Vehicle (PHEV)

- 6.2.2 Internal Combustion Engine (ICE)

- 6.2.2.1 Diesel

- 6.2.2.2 Compressed Natural Gas (CNG)

- 6.2.2.3 Gasoline

- 6.2.2.4 Liquefied Petroleum Gas (LPG)

- 6.2.1 Hybrid and Electric Vehicles

- 6.3 By Gross Vehicle Weight Rating (Tonnage Class)

- 6.3.1 Class 1 (Below 1.8 t)

- 6.3.2 Class 2 (1.8-3.5 t)

- 6.3.3 Class 3 (3.5-7.5 t)

- 6.3.4 Class 4 (7.5-16 t)

- 6.3.5 Class 5 (Above 16 t)

- 6.4 By End-Use Industry

- 6.4.1 Logistics and E-commerce

- 6.4.2 Construction and Mining

- 6.4.3 Public Transport

- 6.4.4 Utilities and Municipal Services

- 6.4.5 Others (Agriculture, Retail)

- 6.5 By Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.1.3 Rest of North America

- 6.5.2 South America

- 6.5.2.1 Brazil

- 6.5.2.2 Argentina

- 6.5.2.3 Rest of South America

- 6.5.3 Europe

- 6.5.3.1 Germany

- 6.5.3.2 United Kingdom

- 6.5.3.3 France

- 6.5.3.4 Italy

- 6.5.3.5 Russia

- 6.5.3.6 Rest of Europe

- 6.5.4 Asia-Pacific

- 6.5.4.1 China

- 6.5.4.2 India

- 6.5.4.3 Japan

- 6.5.4.4 South Korea

- 6.5.4.5 Rest of Asia-Pacific

- 6.5.5 Middle East and Africa

- 6.5.5.1 Saudi Arabia

- 6.5.5.2 United Arab Emirates

- 6.5.5.3 South Africa

- 6.5.5.4 Rest of the Middle East and Africa

- 6.5.1 North America

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 7.4.1 Daimler Truck AG

- 7.4.2 Volvo Group

- 7.4.3 PACCAR Inc.

- 7.4.4 Traton SE

- 7.4.5 Dongfeng Motor Corporation Ltd.

- 7.4.6 Tata Motors Limited

- 7.4.7 BYD Auto Co., Ltd.

- 7.4.8 SAIC Motor Corporation Limited

- 7.4.9 Ford Motor Company

- 7.4.10 General Motors Company

- 7.4.11 Toyota Motor Corporation

- 7.4.12 Hyundai Motor Company

- 7.4.13 Nissan Motor Co., Ltd.

- 7.4.14 Mahindra & Mahindra Ltd.

- 7.4.15 Renault Group

- 7.4.16 Rivian Automotive Inc.

- 7.4.17 Iveco Group N.V.

- 7.4.18 Isuzu Motors Ltd.

- 7.4.19 Beiqi Foton Motor Co., Ltd.

8 Market Opportunities & Future Outlook

- 8.1 White-space & Unmet-Need Assessment

9 Key Strategic Questions for CEOs