PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066725

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066725

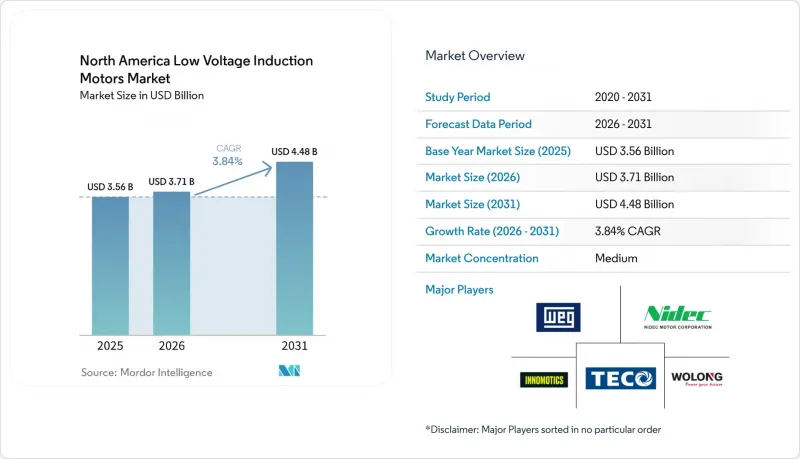

North America Low Voltage Induction Motors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america low voltage induction motors market size is expected to grow from USD 3.56 billion in 2025 to USD 3.71 billion in 2026 and is forecast to reach USD 4.48 billion by 2031 at 3.84% CAGR over 2026-2031.

This report is Segmented by Motor Type (Single Phase, and Poly Phase), Application (Pumps and Fans, Compressors, Conveyors and Material Handling, HVAC and Refrigeration, and More), Efficiency Class (IE1/Standard Efficiency, and More), End-User Industry (Oil and Gas, Water and Wastewater, Food and Beverage, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Low Voltage Induction Motors Market Trends and Insights

Tightening DOE Efficiency Standards for Expanded-Scope Motors

Federal efficiency regulation is shaping the near-term outlook of the North America low voltage induction motors market more than any other structural driver. The U.S. Department of Energy published a final rule in January 2025 for expanded-scope electric motors that covers single-phase and poly phase induction motors rated 0.25 to 3 horsepower, with compliance required by January 1, 2029. A separate rule path for 100-250 horsepower motors is pushing buyers toward IE4-class designs ahead of the June 2027 compliance date, which is pulling forward planning and replacement decisions across industrial sites. DOE also said the expanded-scope standards would generate material annual operating cost savings for end users, which strengthens the financial case for replacing older installed motors instead of delaying upgrades. The practical effect is that the North America low voltage induction motors market is seeing more attention on certified premium-efficiency models, compliance timing, and supplier readiness, especially where procurement teams do not want to face bottlenecks closer to the deadline.

Industrial Automation and Brownfield Retrofit Spending

Brownfield modernization is supporting the North America low voltage induction motors market because older plants can often replace motors and drives without redesigning the surrounding electrical system. Retrofit projects are increasingly tied to predictive maintenance and digital monitoring, which helps plant teams measure energy losses and justify changeouts on a clearer payback basis. ABB has positioned its SP4 line around DOE-ready super-premium performance, and that aligns with the growing preference for compliant motors in upgrade cycles rather than only in new facilities. The upgrade case is especially strong in continuous-duty pump, fan, and conveyor services where electricity use dominates lifecycle cost. This is keeping replacement activity active across manufacturing corridors in the United States and helping the North America low voltage induction motors market hold steady growth even when greenfield spending is uneven.

Copper and Aluminum Cost Volatility

Raw material volatility remains the clearest cost-side restraint for the North America low voltage induction motors market. Copper and aluminum costs affect manufacturer margins, distributor pricing, and end-user replacement timing, especially when projects are price-sensitive and capital approval windows are narrow. This matters most in the move from IE2 to IE3 or IE4, because higher-efficiency designs already carry a higher upfront cost and become harder to justify when input prices are unstable. The result is a wider price gap between lower-tier and premium-tier products, even when buyers understand the energy savings case over time. That keeps the North America low voltage induction motors market growing, but it slows the speed at which some facilities move from basic replacement buying to planned premium-efficiency upgrades.

Other drivers and restraints analyzed in the detailed report include:

- Water and Wastewater Infrastructure Upgrades

- Mexico Nearshoring and Plant Localization

- Higher First-Cost Barrier for Premium-Efficiency Retrofits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Poly phase motors held 90.23% of the North America low voltage induction motors market share in 2025, which kept them far ahead of single phase designs in the regional revenue mix. Their position reflects strong compatibility with three-phase power systems, better torque characteristics, and lower maintenance demands in continuous-duty operations. The segment is also forecast to post the fastest 4.43% CAGR through 2031, which shows that growth is not only coming from base dominance but also from new specification momentum. In food processing, beverage production, and industrial refrigeration, plant teams continue to make poly phase IE3 and IE4 motors the default choice for new lines because reliability and stable operation matter as much as efficiency gains. This keeps the North America low voltage induction motors market centered on industrial duty cycles rather than on fragmented small-load use cases.

Poly phase units above 5 horsepower are often the practical choice in continuous-duty industrial settings because single phase supply in that range adds conversion losses, more complexity, and extra maintenance points. That operating reality supports steady demand across pumps, conveyors, compressors, and plant utility systems. Single phase motors still serve light commercial, agricultural, and residential pump applications where three-phase power is unavailable or too costly to install. DOE's January 2025 final rule for expanded-scope motors is also reshaping the lower-horsepower single phase segment by raising the performance threshold for many designs in the 0.25-3 horsepower range. The result is that volume leadership remains with poly phase motors, while single phase revenue is being influenced more by compliance-driven design upgrades than by broad unit growth.

Pumps and fans accounted for 35.78% of the North America low voltage induction motors market size in 2025, making them the largest application group in the region. Their lead comes from the depth of installed motors across water treatment, oil and gas processing, HVAC chiller loops, cooling systems, and chemical plants. This installed base creates repeat replacement demand that is less exposed to abrupt changes in capital spending because many systems cannot tolerate long outages. It also supports the case for premium-efficiency upgrades when facilities need better reliability, lower heat generation, and stronger inverter-duty performance. The North America low voltage induction motors market, therefore, continues to draw stable demand from pump and fan services even when other applications move in cycles.

Compressors are projected to grow at the fastest 4.25% CAGR through 2031, supported by rising use in cold-chain systems, natural gas handling, and liquid cooling systems tied to AI-linked data center buildouts. Nidec's November 2025 launch of its TEFC Inverter Duty Closed Coupled Pump motor line also shows how suppliers are designing around variable-speed, utility-heavy applications that sit close to both pumping and compression duties. Conveyors and material handling remain important because factory automation and distribution growth continue to add motor-intensive movement systems across the United States and Mexico. HVAC and refrigeration below 37 kW face some substitution from EC and permanent-magnet technologies, but induction motors remain well placed in larger-frame and harsher-duty systems where serviceability and rewind economics matter more. General industrial machinery and the long tail of smaller applications continue to provide a broad demand floor, even if those buyers are more exposed to supply chain and pricing pressure.

List of Companies Covered in this Report:

- WEG S.A.

- Nidec Motor Corporation

- Innomotics GmbH

- TECO Electric & Machinery Co., Ltd.

- Wolong Electric Group Co., Ltd.

- Regal Rexnord Corporation

- Brook Crompton UK Ltd.

- VEM GmbH

- Hoyer Motors A/S

- Lafert S.p.A.

- Cantoni Motor S.A.

- CG Power and Industrial Solutions Limited

- ABB Ltd.

- Bharat Bijlee Limited

- Bonfiglioli Riduttori S.p.A.

- SEW-EURODRIVE GmbH & Co KG

- Getriebebau NORD GmbH & Co. KG

- Neri Motori S.r.l.

- OME Motors S.r.l.

- T-T Electric Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening DOE Efficiency Standards for Expanded-Scope Motors

- 4.2.2 Industrial Automation and Brownfield Retrofit Spending

- 4.2.3 Water and Wastewater Infrastructure Upgrades

- 4.2.4 Mexico Nearshoring and Plant Localization

- 4.2.5 AI Data Center Cooling Loop Expansion

- 4.2.6 Semiconductor and Battery Utility System Build-Out

- 4.3 Market Restraints

- 4.3.1 Copper and Aluminum Cost Volatility

- 4.3.2 Higher First-Cost Barrier for Premium-Efficiency Retrofits

- 4.3.3 EC and Permanent-Magnet Motor Substitution in HVAC

- 4.3.4 Tariff-Driven Component Sourcing Instability

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motor Type

- 5.1.1 Single Phase

- 5.1.2 Poly Phase

- 5.2 By Application

- 5.2.1 Pumps and Fans

- 5.2.2 Compressors

- 5.2.3 Conveyors and Material Handling

- 5.2.4 HVAC and Refrigeration

- 5.2.5 General Industrial Machinery

- 5.2.6 Other Applications

- 5.3 By Efficiency Class

- 5.3.1 IE1/Standard Efficiency

- 5.3.2 IE2/High Efficiency

- 5.3.3 IE3/Premium Efficiency

- 5.3.4 IE4/Super-Premium Efficiency

- 5.4 By End-User Industry

- 5.4.1 Oil and Gas

- 5.4.2 Water and Wastewater

- 5.4.3 Chemicals and Petrochemicals

- 5.4.4 Food and Beverage

- 5.4.5 Discrete Manufacturing

- 5.4.6 Metal and Mining

- 5.4.7 Other End-User Industries

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 WEG S.A.

- 6.4.2 Nidec Motor Corporation

- 6.4.3 Innomotics GmbH

- 6.4.4 TECO Electric & Machinery Co., Ltd.

- 6.4.5 Wolong Electric Group Co., Ltd.

- 6.4.6 Regal Rexnord Corporation

- 6.4.7 Brook Crompton UK Ltd.

- 6.4.8 VEM GmbH

- 6.4.9 Hoyer Motors A/S

- 6.4.10 Lafert S.p.A.

- 6.4.11 Cantoni Motor S.A.

- 6.4.12 CG Power and Industrial Solutions Limited

- 6.4.13 ABB Ltd.

- 6.4.14 Bharat Bijlee Limited

- 6.4.15 Bonfiglioli Riduttori S.p.A.

- 6.4.16 SEW-EURODRIVE GmbH & Co KG

- 6.4.17 Getriebebau NORD GmbH & Co. KG

- 6.4.18 Neri Motori S.r.l.

- 6.4.19 OME Motors S.r.l.

- 6.4.20 T-T Electric Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment