PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066740

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066740

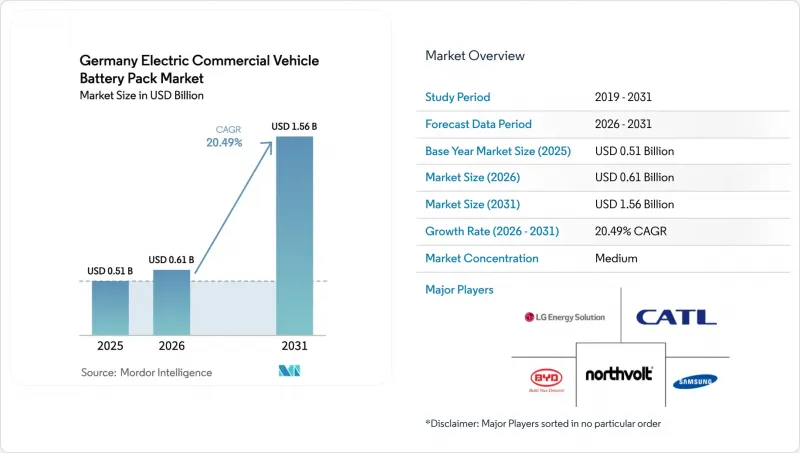

Germany Electric Commercial Vehicle Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the german electric commercial vehicle battery pack market size is expected to increase from USD 0.51 billion in 2025 to USD 0.61 billion in 2026 and reach USD 1.56 billion by 2031, growing at a CAGR of 20.49% over 2026-2031.

This report is Segmented by Vehicle Type (Light Commercial Vehicle, and More), Propulsion Type (Battery Electric Vehicle, and More), Battery Chemistry (Lithium Iron Phosphate, and More), Capacity (Below 15 KWh, and More), Battery Form (Cylindrical, and More), Voltage, Module Architecture, Component. The Market Forecasts are Provided in Terms of Value (USD) and Volume in Units.

Germany Electric Commercial Vehicle Battery Pack Market Trends and Insights

Federal E-CV Subsidy Program Driving the Market Growth

Germany's national incentive program is significantly improving the economics of battery-electric trucks. By reducing ownership costs and accelerating procurement timelines, the scheme enables faster fleet transitions and makes electric commercial vehicles more attractive to operators . Local-content clauses shield domestic suppliers and partially neutralize Chinese cost advantages. The program focuses on packs above 40 kWh, catalyzing demand in medium and heavy-duty classes facing infrastructure gaps. Stakeholders voice concern that the 2027 sunset could create a volume cliff, yet near-term pull-forward orders lend momentum to the German electric commercial vehicle battery pack market. OEMs are now front-loading production schedules to maximize grant capture and lock in cell allocations.

EU HDV CO2 Targets

Brussels' requirement for a 90% cut in heavy-duty vehicle emissions by 2040 converts battery demand from optional to obligatory. Non-compliant trucks will attract penalties per gram of excess CO2, forcing German OEMs to cease new internal-combustion programs. Interim 2030 targets accelerate platform redesign, pushing the German electric commercial vehicle battery pack market toward higher-capacity packs over hybrid stopgaps. Procurement teams now secure four-year supply contracts to de-risk compliance. The regulation stabilizes long-run demand but intensifies short-term sourcing pressure.

Sparse Truck-Charging Corridors

Major logistics firms are increasingly turning to electric urban delivery fleets due to a significant drop in battery pack prices, making them competitive with diesel. Yet, the infrastructure hasn't kept pace, particularly for heavy-duty vehicles. The number of fast-charging points falls short of targets, curtailing long-haul efficiency and potentially leading to future bottlenecks if the rollout doesn't speed up. As a stopgap, OEMs are deploying mobile charging trailers, and in a strategic move to mitigate geopolitical risks, supply chains are pivoting towards European cell assembly.

Other drivers and restraints analyzed in the detailed report include:

- LFP Pack Cost Drops Below USD 100/kWh

- Battery-as-a-Service Bus Contracts

- Graphite-Plant Permitting Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Light commercial vehicles (LCVs) held 48.18% of Germany's electric commercial vehicle battery pack market share in 2025, underpinned by courier and postal fleets operating 100-200 km daily routes. Shipment surges in e-commerce sustain baseline pack demand in the 60-80 kWh bracket. In contrast, medium and heavy trucks show the swiftest 22.38% CAGR as policy subsidies override lingering cost and payload concerns. Federal grants for heavy trucks have expedited orders and hastened platform launches. Urban noise regulations and low-emission zones are bolstering the electrification of light commercial vehicles (LCVs), while EU CO2 penalties are steering original equipment manufacturers (OEMs) towards battery-electric drivetrains for long hauls.

Fleet operators are consolidating orders to gain priority production slots and negotiate better pricing on bulk cells. The focus of innovation is on modular pack designs that enable fleets to interchange cartridges for optimized range. While overnight depot charging is standard for LCVs, public high-power stations are essential for trucks on long routes. As a result, the German market for electric commercial vehicle battery packs is charting a dual-speed path: LCV volumes are driving early revenues, while truck platforms are poised to achieve scale in the future.

Battery-electric vehicles captured 81.62% of 2025 deliveries and will log a 21.21% CAGR as OEMs phase out plug-in hybrids. Zero-tailpipe-emission rules and simpler driveline maintenance tilt fleets toward BEVs despite higher initial prices. PHEVs are only found in regional bus operators that lack depot power upgrades. Regulatory credit systems also incentivize pure BEVs, deepening their advantage in the German electric commercial vehicle battery pack market for propulsion solutions.

Charging ecosystems are adapting: depot smart-charging software staggers load to avoid peak tariffs, while megawatt chargers are piloting along the Rhine-Main corridor. Component suppliers now tune thermal systems to enable quicker DC fast-charge cycles to meet tight delivery windows. With residual values stabilizing, leasing companies are increasingly open to underwriting BEV fleets, thereby broadening access for SMEs. Stakeholders anticipate that PHEV market share will decline, further solidifying the momentum behind battery-electric platforms.

LFP packs commanded a 45.09% share in 2025 due to their lower costs, safety, and stable supply chains. The absence of nickel and cobalt shields prices from metal volatility, giving LFP a strategic edge in the German electric commercial vehicle battery pack market. LMFP, however, posts a brisk 22.52% CAGR, promising an energy density 10-15% higher without compromising thermal stability. OEMs earmark LMFP for premium regional trucks, where pack-weight savings enable extra payload.

NMC chemistries remain essential for long-range buses that require compact footprints, yet high-nickel blends are subject to price swings. Suppliers are increasingly co-locating LFP and LMFP lines to hedge against demand shifts. Solid-state prototypes are entering validation but will not influence volume before 2029. Chemistries are evolving from cost-driven dominance toward performance-tiered portfolios that let fleets match pack characteristics to duty cycles.

List of Companies Covered in this Report:

- Akasol AG (Borgwarner Inc.)

- Automotive Cells Company (ACC)

- BYD Company Ltd.

- Contemporary Amperex Technology Co. Ltd. (CATL)

- Samsung SDI Co. Ltd.

- LG Energy Solution Ltd.

- Northvolt AB

- Panasonic Holdings Corp.

- Microvast Holdings, Inc.

- BMZ Germany GmbH

- Webasto SE

- Forsee Power

- Liacon GmbH

- Super B

- SK On Co., Ltd.

- Ebusco Holding N.V.

- Saft Groupe S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Electric Vehicle Sales

- 4.2 Electric Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Battery Chemistry Price Comparison

- 4.8 EV Battery Capacity and Efficiency

- 4.9 Upcoming EV Models

- 4.10 Cell and Pack Capacity vs Utilization

- 4.11 Regulatory Framework

- 4.12 Type Approval and Pack Safety Standards

- 4.13 Market Access: Incentives, Local Content and Trade

- 4.14 End-of-Life: EPR, Second-Life and Recycling Mandates

- 4.15 Value Chain and Distribution Channel Analysis

- 4.16 Technological Outlook

- 4.17 Porter's Five Forces

- 4.17.1 Threat of New Entrants

- 4.17.2 Bargaining Power of Suppliers

- 4.17.3 Bargaining Power of Buyers

- 4.17.4 Threat of Substitutes

- 4.17.5 Competitive Rivalry

- 4.18 Market Drivers

- 4.18.1 Federal E-CV Subsidy Program Driving Market Growth

- 4.18.2 EU HDV CO2 Targets

- 4.18.3 LFP Pack Cost Drops Below USD 100/kWh

- 4.18.4 Night-Time City-Logistics Noise Caps

- 4.18.5 Shift To 800 V Coach Platforms

- 4.18.6 Battery-As-A-Service Bus Contracts

- 4.19 Market Restraints

- 4.19.1 Sparse Truck-Charging Corridors

- 4.19.2 Up-Front Cost Premium Vs Diesel

- 4.19.3 Graphite-Plant Permitting Delays

- 4.19.4 LMFP License-Fee Volatility

5 Market Size and Growth Forecasts (Value in USD and Volume in Units)

- 5.1 By Vehicle Type

- 5.1.1 Light Commercial Vehicle

- 5.1.2 Medium and Heavy Duty Truck

- 5.1.3 Bus

- 5.2 By Propulsion Type

- 5.2.1 Baterry Electric Vehicle

- 5.2.2 Plug-in Hybrid Electric Vehicle

- 5.3 By Battery Chemistry

- 5.3.1 LFP (Lithium Iron Phosphate)

- 5.3.2 LMFP (Lithium Manganese Iron Phosphate)

- 5.3.3 NMC (Nickel Manganese Cobalt Oxide)

- 5.3.4 NCA (Nickel Cobalt Aluminum Oxide)

- 5.3.5 LTO (Lithium Titanium Oxide)

- 5.3.6 Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.)

- 5.4 By Capacity

- 5.4.1 Below 15 kWh

- 5.4.2 15-40 kWh

- 5.4.3 40-60 kWh

- 5.4.4 60-80 kWh

- 5.4.5 80-100 kWh

- 5.4.6 100-150 kWh

- 5.4.7 Above 150 kWh

- 5.5 By Battery Form

- 5.5.1 Cylindrical

- 5.5.2 Pouch

- 5.5.3 Prismatic

- 5.6 By Voltage Class

- 5.6.1 Below 400 V (48-350 V)

- 5.6.2 400-600 V

- 5.6.3 600-800 V

- 5.6.4 Above 800 V

- 5.7 By Module Architecture

- 5.7.1 Cell-to-Module (CTM)

- 5.7.2 Cell-to-Pack (CTP)

- 5.7.3 Module-to-Pack (MTP)

- 5.8 By Component

- 5.8.1 Anode

- 5.8.2 Cathode

- 5.8.3 Electrolyte

- 5.8.4 Separator

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akasol AG (Borgwarner Inc.)

- 6.4.2 Automotive Cells Company (ACC)

- 6.4.3 BYD Company Ltd.

- 6.4.4 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.5 Samsung SDI Co. Ltd.

- 6.4.6 LG Energy Solution Ltd.

- 6.4.7 Northvolt AB

- 6.4.8 Panasonic Holdings Corp.

- 6.4.9 Microvast Holdings, Inc.

- 6.4.10 BMZ Germany GmbH

- 6.4.11 Webasto SE

- 6.4.12 Forsee Power

- 6.4.13 Liacon GmbH

- 6.4.14 Super B

- 6.4.15 SK On Co., Ltd.

- 6.4.16 Ebusco Holding N.V.

- 6.4.17 Saft Groupe S.A.

7 Market Opportunities and Future Outlook

8 Key Strategic Questions for EV Battery Pack CEOs

9 Who Supplies Whom (OEM-Tier Map)

10 Localization and Cost Stack

- 10.1 BoM Split (USD/kWh)

- 10.2 Local vs Imported Content

- 10.3 Tariff/Subsidy Pass-Through

11 Capacity and Utilization Tracker

- 11.1 Cell GWh (Installed/Under-Build)

- 11.2 Utilization and Bottlenecks

- 11.3 New Plant Pipeline

12 Trade Flow and Import Dependence

13 Recycling and Second-Life Ecosystem