PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066747

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066747

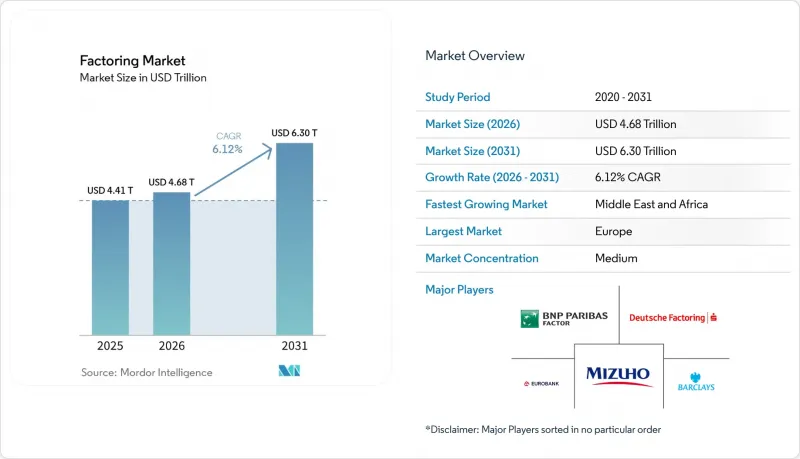

Factoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the factoring market size is projected to expand from USD 4.41 trillion in 2025 and USD 4.68 trillion in 2026 to USD 6.30 trillion by 2031, registering a CAGR of 6.12% between 2026 to 2031.

This report is Segmented by Provider (Banks, Non-Bank Financial Companies), Enterprise Size (Large Enterprises, Small & Medium-Sized Enterprises), Application (Domestic, International), End-Use Industry (IT & Telecommunication, Manufacturing, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Factoring Market Trends and Insights

Rising Adoption of Fintech Platforms Among SMEs

Small and medium-sized enterprises are adopting digital factoring solutions to stabilize cash flow and reduce time to funding, which is improving the reach of the factoring market among underserved borrowers. Triumph Financial reported that it could purchase 75% of small-carrier invoices without manual review using a machine-learning engine, which shows how automation shortens underwriting cycles and lowers operating costs. Its LoadPay virtual wallet provides instant 24/7 funding through bank-licensed subledger accounts, which tightens the loop between invoice purchase and supplier liquidity. Banks are also streamlining access through digital portals and integrated workflows, as seen in HSBC Indonesia's TradePay solution that merged digital payments and working capital in one platform. Deep integration into cloud enterprise software is improving straight-through processing as eligible receivables can flow into embedded receivables programs with accurate journal posting and bank funding, which reduces operational friction for SMEs. These technical and distribution shifts are pulling more SMEs into the factoring market by reducing onboarding burden and connecting credit to everyday business systems.

Expansion of Cross-Border Trade & E-Commerce

Cross-border e-commerce adoption and open-account trade are lifting demand for international receivables financing, which is widening the application set addressed by the factoring market. International factoring is expected to outpace domestic activity with a 9.33% CAGR through 2031 as platform integrations make cross-border funding more seamless for sellers. In 2025, HSBC expanded solutions to support e-commerce sellers with near-real-time data, enabling same-day or next-day currency settlement that cut foreign-exchange costs, which encourages more merchants to export on open-account terms. J.P. Morgan embedded supply-chain finance tools into Oracle Fusion Cloud ERP for FedEx vendors, which allows early payments priced to the buyer's credit and makes adoption easier for suppliers that sell into global markets. These programs strengthen seller confidence because pricing reflects large buyers' credit quality rather than smaller suppliers' balance sheets, which supports international scaling. Leading platforms that accelerate large volumes of invoices and pay suppliers early also underpin cross-border workflows by standardizing documentation and funding routines.

Rising Cyber-Risk & Data-Privacy Breaches

Higher fraud sophistication and data exposure elevate risk in receivables verification and collateral monitoring, which adds cost to operations across the factoring market. BNP Paribas disclosed that a specific receivables-financing fraud case contributed to an almost EUR 1.5 billion rise in doubtful loans during the third quarter of 2025, which highlighted the need for deeper controls and real-time checks. Transportation factors in North America reported rising attempts at identity compromise and false documentation during 2024 and 2025, which shows how fraud rings target fast-growing niches. The European Union's Digital Operational Resilience Act took effect in January 2025 and requires enhanced information and communications technology risk management for financial entities, which widens compliance scope for providers handling invoice and payment data. Providers have responded with tighter onboarding checks, multi-source invoice verification, and secure payment instruction controls, which improve resilience but increase unit costs. As cyber controls intensify, margins can be squeezed even as transaction volumes grow in the factoring market.

Other drivers and restraints analyzed in the detailed report include:

- EU Late-Payment Regulation Intensifying Working-Capital Demand

- Supply-Chain Finance Programs Led by Global Corporations

- Patchy Licensing & Prudential Rules in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Banks retained 64.59% of provider-type share in 2025 and continue to leverage balance-sheet depth and cross-product relationships, while non-bank financial companies are projected to expand faster at 8.92% CAGR through 2031 as embedded finance spreads across the factoring market. Providers are reinforcing scale by wiring solutions into enterprise software so suppliers can trigger early payments from familiar systems, which reduces implementation time and boosts adoption. J.P. Morgan's 2025 launch with Oracle allows vendors to select early payment at rates linked to the buyer's credit with activation inside Oracle Cloud ERP, which shortens deployment cycles and supports supplier uptake. Meanwhile, Triumph is using machine learning to purchase most small-carrier invoices without manual review and fund them instantly via digital wallets, which shows how non-banks can build on real-time payment rails. These shifts, along with bank portals and APIs, are improving speed and experience across the factoring market.

Banks are modernizing to protect core relationships, while non-banks focus on speed and integration that meet specific sector needs in the factoring industry. HSBC Indonesia introduced a digital invoice and payment solution that puts working capital and payouts in one place, which reflects how bank platforms are adapting to client expectations. SAP Taulia's receivables solution integrates natively with SAP Cloud ERP and automates journal posting, which gives finance teams tighter control and audit-ready records while maintaining access to bank funding networks. These integrated experiences compress onboarding time and training needs, which helps both bank and non-bank providers scale with fewer manual touchpoints. As non-banks grow, partnerships with licensed banks and large platforms continue to provide balance-sheet capacity and distribution. The result is a competitive mix that supports wider access to receivables funding across the factoring market.

Small and medium-sized enterprises held 68.42% share in 2025 and are projected to grow at a 7.76% CAGR through 2031 as digital origination, embedded portals, and faster settlement make receivables finance more accessible across the factoring market. SMEs tend to experience more variable cash conversion cycles, so the ability to monetize invoices quickly is a strong fit for working-capital needs. Corporate-led programs that price early payment to a large buyer's credit rating are especially helpful for small vendors that sell to global brands. J.P. Morgan's integration with Oracle Cloud ERP is one example of how supplier enrollment and usage can be simplified to reduce the burden on smaller finance teams. Digital bank offerings like HSBC Indonesia's TradePay also show how banks are packaging flow-of-funds tools for smaller firms in growing markets.

Access remains uneven in places where credit models depend on backward-looking bureau data rather than live cash-flow telemetry, which narrows eligibility for young, thin-file firms in the factoring market. The CFPB's proposed rule excluding factoring from small-business lending data collection and reporting reduces visibility into approval outcomes, which makes it harder to assess model fairness. At the same time, embedded solutions and real-time payment rails are enabling micro-factoring for very small invoices, which supports micro and small businesses with faster access to funds when traditional lines are not available. As banks and non-banks expand data sources to include buyer performance and invoice-level behaviour, more SMEs can qualify with limits that match their cash cycles. These advances balance inclusion with risk control and expand the supplier base served by the factoring market.

Geography Analysis

Europe retained 58.56% of global share in 2025, which reflects a deep base of bank platforms, active corporate programs, and supportive regulation that protects suppliers' right to assign receivables across the factoring market. The European Union's late-payment rules cap terms at 60 days and prohibit anti-assignment clauses, which directly reduces barriers to factoring and encourages early-payment arrangements at scale. Banks and corporates are aligning technology and data to speed enrollment and funding, which enables suppliers to adopt solutions inside the systems they already use. European institutions also continue to expand sustainability-linked programs and deep-tier finance, which extends liquidity further down multi-tier supply chains. These conditions underpin Europe's outsized role in the factoring market while creating room for further gains as digital workflows mature.

North America features scaled platforms and fast-moving fintechs that emphasize automation and real-time funding, which strengthens the region's profile in the global factoring market. Triumph's commitment to machine learning in invoice purchasing and its LoadPay wallet illustrate how technology and proprietary rails can compress decision cycles and support 24/7 liquidity for carriers and other small suppliers. eCapital upsized its asset-based lending facility to USD 1.38 billion in June 2025 and expanded total banking capacity toward USD 2.6 billion, which signals continued investment in working-capital programs across healthcare and commercial operations. First Citizens BancShares announced plans in October 2025 to acquire 138 BMO branches, with closing expected in mid-2026, which is aimed at expanding deposits and credit capacity that can backstop receivables finance. Monetary policy easing has progressed since 2024 in Canada, which influences funding benchmarks even as risk pricing remains firm for higher-volatility segments. These structural and cyclical forces together shape the North American trajectory within the factoring market.

Asia-Pacific benefits from export-driven supply chains, enterprise digitization, and fast-growing embedded solutions, which broaden the base for receivables finance in the factoring market. HSBC Indonesia launched TradePay and signed a sustainability supply-chain finance agreement with Saint-Gobain Indonesia, which underscores local momentum in digital working capital and supplier incentives. Mizuho expanded universal banking capabilities in the European Union and enhanced private assets partnerships, which support cross-border trade offers for Asia-headquartered clients with global operations. Embedded receivables tools inside ERP systems and marketplaces reduce the need for standalone onboarding and allow quicker funding against approved invoices. The Middle East and Africa corridor is projected to be the fastest-growing geography at a 10.21% CAGR through 2031, which reflects rising digitization and expanding fintech infrastructure that supports working-capital distribution. Across South America, providers are aligning digital invoicing and secure data exchange with bank capacity, which supports steady adoption as policy frameworks evolve and corporate programs expand supplier reach.

- Barclays PLC

- BNP Paribas Factoring

- Deutsche Factoring Bank

- Mizuho Financial Group

- Eurobank Ergasias SA

- Mitsubishi HC Capital UK

- AwanTunai

- KUKE Finance JSC

- RTS Financial Services

- Triumph Financial

- First Citizens BancShares

- American Express

- Intuit QuickBooks Financing

- Riviera Finance

- eCapital Corp

- TCI Business Capital

- Taulia (SAP)

- JPMorgan

- HSBC

- Resolve Pay

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of fintech platforms among SMEs

- 4.2.2 Expansion of cross-border trade & e-commerce

- 4.2.3 EU late-payment regulation intensifying working-capital demand

- 4.2.4 Supply-chain finance programs led by global corporates

- 4.2.5 Embedded-finance & B2B-BNPL APIs enabling "in-cart" factoring

- 4.2.6 Real-time payment rails unlocking micro-factoring

- 4.3 Market Restraints

- 4.3.1 High cost of factoring relative to bank credit

- 4.3.2 Rising cyber-risk & data-privacy breaches

- 4.3.3 Patchy licensing & prudential rules in emerging markets

- 4.3.4 Algorithmic-risk models excluding thin-file SMEs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Provider

- 5.1.1 Banks

- 5.1.2 Non-Bank Financial Companies (NBFCs)

- 5.2 By Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small & Medium-sized Enterprises (SMEs)

- 5.3 By Application

- 5.3.1 Domestic

- 5.3.2 International

- 5.4 By End-Use Industry

- 5.4.1 IT & Telecommunication

- 5.4.2 Manufacturing

- 5.4.3 Retail And E-Commerce

- 5.4.4 Healthcare And Pharmaceuticals

- 5.4.5 Travel & Hospitality

- 5.4.6 Transportation & Logistics

- 5.4.7 Other Industry Verticals

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Colombia

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Benelux (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Barclays PLC

- 6.4.2 BNP Paribas Factoring

- 6.4.3 Deutsche Factoring Bank

- 6.4.4 Mizuho Financial Group

- 6.4.5 Eurobank Ergasias SA

- 6.4.6 Mitsubishi HC Capital UK

- 6.4.7 AwanTunai

- 6.4.8 KUKE Finance JSC

- 6.4.9 RTS Financial Services

- 6.4.10 Triumph Financial

- 6.4.11 First Citizens BancShares

- 6.4.12 American Express

- 6.4.13 Intuit QuickBooks Financing

- 6.4.14 Riviera Finance

- 6.4.15 eCapital Corp

- 6.4.16 TCI Business Capital

- 6.4.17 Taulia (SAP)

- 6.4.18 JPMorgan

- 6.4.19 HSBC

- 6.4.20 Resolve Pay

7 Market Opportunities & Future Outlook

- 7.1 Micro-factoring and flexible service models for smaller ticket sizes are a growing niche

- 7.2 Expanding cross-border factoring and trade finance partnerships in high-growth regions