PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066766

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066766

Automotive Display Panel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

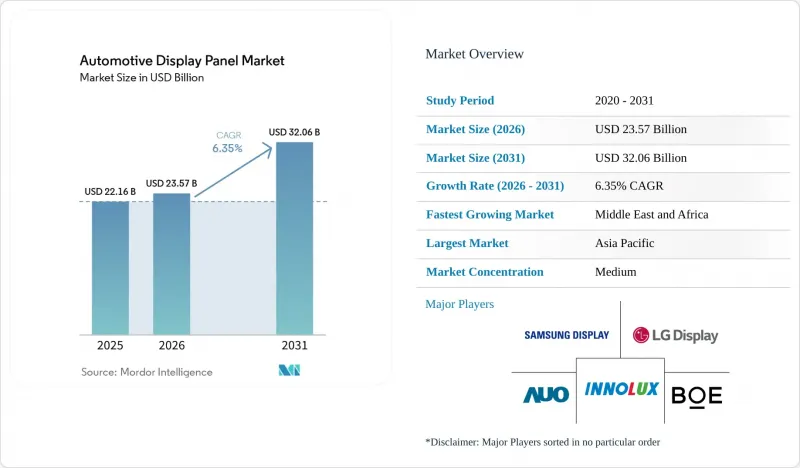

According to Mordor Intelligence, the automotive display panel market size is expected to grow from USD 22.16 billion in 2025 to USD 23.57 billion in 2026 and is forecast to reach USD 32.06 billion by 2031 at 6.35% CAGR over 2026-2031.

This report is Segmented by Display Technology (a-Si LCD, and More), Screen Size (Up To 5 Inch, and More), Vehicle Type (Passenger Cars, and More), Application (Instrument Cluster, and More), Integration Level (Stand-Alone Displays, and More), Touch/Control (Touchscreen, and More), Sales Channel (OEM-Fitted, and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Display Panel Market Trends and Insights

Automaker race to deliver pillar-to-pillar cockpit displays in China and US premium segments

Mass-production of LG Display's 40-inch unit since February 2025 signals a paradigm shift whereby displays act as brand signatures instead of functional upgrades. Switchable Privacy Mode permits front-seat streaming without distracting the driver, alleviating regulatory risk while enabling subscription revenue. Sony-Honda's AFEELA sedan will debut the module, and more than 100 Chinese EV launches in 2024 already prioritized similar configurations. This reinforces a display-centric cockpit model that supports over-the-air feature unlocks, making the automotive display panel market a software monetization anchor

Regulatory push for advanced driver assistance requiring larger digital instrument clusters in EU

Regulation (EU) 2019/2144 forces new type approvals from July 2024 to integrate driver-distraction warning functions that rely on gaze tracking. Meeting the technical files persuades OEMs to standardize larger, sensor-rich clusters across model lines rather than limit such panels to premium trims. The rule also propagates globally through UNECE channels, effectively lifting the baseline specification for forthcoming instrument clusters.

OLED burn-in reliability concerns limiting deployment in taxis/fleets

Continuous static images such as fare data create uneven pixel aging. Pixel-shift algorithms raise uniformity to 94.5%, yet operators demand multi-year proof before large rollouts. Replacement cycles of 5-7 years amplify the hesitancy, stalling OLED penetration into high-utilization fleets that otherwise would contribute sizable volumes to the automotive display panel market.

Other drivers and restraints analyzed in the detailed report include:

- Falling OLED panel ASPs triggering OEM adoption in mid-range passenger cars

- Mini-LED backlighting enhancing brightness for EVs in high-temperature Middle-East markets

- Scarcity of IGZO backplane capacity causing 2025 model-year delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MicroLED is set to grow at 10.85% CAGR as carmakers target unmatched brightness and efficiency for flagship models. AUO's transparent roof panels and morphing controls presented in 2025 validate design freedom that standard LCD cannot match. While a-Si LCD still commanded 50.74% revenue, its cost advantage wanes in upper trims where user-experience metrics trump unit price. Oxide LCD (IGZO) powers high-resolution instrument clusters that need minimal standby draw, and Mini-LED backlit LCD bridges the gap with quasi-OLED contrast. OLED breakthroughs in burn-in algorithms lengthen usable life, yet fleet buyers stay wary. These parallel tracks confirm that the automotive display panel market accommodates coexistence rather than outright substitution, enabling tiered feature packaging across vehicle lines.

Large automakers now hedge sourcing risk by approving both MicroLED and OLED for future cockpits; Samsung Display already samples 12-inch MicroLED clusters for 2028 production. Meanwhile, Tier-1 suppliers embed common graphics stacks so dashboards can interchange panel types with minor software changes, supporting software-defined vehicles goals. This flexibility sustains volume for incumbent LCD fabs even as next-gen formats expand, keeping the automotive display panel industry diversified.

Displays above 12 inches, though niche in 2024, unlock new cockpit architectures such as pillar-to-pillar dashboards and roof installations. LG Display's 40-inch module supports multi-zone dimming, allowing simultaneous cluster, infotainment, and passenger cinema in one surface. Mid-sized 5.1-8 inch panels remain primary for mainstream infotainment and secure 37.12% 2025 revenue, but growth momentum shifts upward. Conversely, up-to-5-inch screens gain traction in mirror replacements and HVAC touch bars, keeping unit volumes high. The bifurcation is clear: premium vehicles order expansive canvases; mass models opt for distributed clusters of small panels. As software layers decouple function from location, size selection hinges on aesthetics and bill-of-materials rather than fixed gauge placement, reinforcing flexible design in the automotive display panel market.

Market leaders deploy adaptive UI frameworks that reconfigure layout based on driving mode, from high-contrast ADAS overlays during motion to cinematic widescreen when parked. Such adaptability steers future strategy, where automotive display panel market size for large formats benefits from time-of-use monetization, for instance, streaming subscriptions activated in autonomous mode.

Passenger cars keep 83.58% of 2025 shipments, yet heavy commercial vehicles grow faster at 13.55% CAGR as safety mandates and telematics converge. Fleet operators justify high-resolution clusters that synthesize tire pressure, route analytics, and driver coaching on a single interface, cutting downtime. Light commercial vans follow, blending passenger-car UX expectations with cargo optimization tools. The automotive display panel market size for commercial classes is projected to cross 15.24% revenue share by 2031, underscoring a shift from optional extras to operational necessities.

Panel suppliers respond with shock-and-vibration-rated assemblies exceeding 70 Gs and anti-glare cover glass that withstands daily cleanings. Over-the-air upgrades permit freight companies to unlock advanced telematics on existing dashboards, converting hardware into recurrent service income. This business model cements displays as revenue generators rather than depreciating assets, amplifying value capture across the automotive display panel industry.

Geography Analysis

Asia-Pacific led with 48.12% revenue in 2025 owing to China's prolific EV pipelines and Japan's early legalization of camera mirrors. Regional automakers tout 32-inch passenger screens and AR HUDs as baseline features, forcing global competitors to match specs. Indigenous panel makers like BOE ship 9K oxide TFT prototypes, proving domestic ecosystem depth. Meanwhile, joint ventures in India localize LCD module assembly, fulfilling cost-sensitive markets and insulating supply from external shocks.

North America benefits from luxury SUV appetite and regulatory momentum toward mirrorless approvals. Pillar-to-pillar dashboards differentiate premium trims, while truck cabins embrace wide displays for towing visualization. Massive semiconductor investments, such as USD 60 billion in new US wafer fabs, strengthen upstream resilience, smoothing panel controller availability. These factors cement North America as the second-largest region by 2025 for the automotive display panel market.

Europe centers on safety-oriented adoption driven by Regulation 2019/2144. Automakers integrate gaze-tracking clusters and cross-domain displays that meet Euro NCAP roadmap targets. Panoramic Vision concepts slated for 2025 production reveal how German OEMs merge ADAS feeds with expansive glass surfaces. Supplier clusters in Germany and Czechia specialize in optical bonding and auto-grade coatings, anchoring European content despite cost pressures.

Middle East and Africa posts the highest 8.17% CAGR. Extreme heat calls for 45,000-nit Mini-LED panels that maintain chroma at 85 °C. Luxury imports equip rear entertainment suites as ride-hailing fleets upgrade passenger amenities. Government electrification targets in Gulf Cooperation Council nations further accelerate demand for efficient, high-brightness displays. South America lags in premium penetration but seeds growth through local glass finishing plants in Brazil and Vietnam-to-Mercosur supply chains, positioning the region for gradual uptake in the automotive display panel industry.

- LG Display

- Samsung Display

- BOE Technology Group

- AUO Corporation

- Innolux Corporation

- Sharp Corporation

- Japan Display Inc.

- Tianma Micro-electronics

- CSOT (TCL China Star)

- Visionox

- Truly Semiconductors

- HKC Corporation

- Continental AG

- Denso Corporation

- Robert Bosch GmbH

- Visteon Corporation

- Panasonic Automotive

- Nippon Seiki

- Magna International

- Marelli

- Yazaki Corporation

- Faurecia (Forvia)

- Desay SV

- Foryou General Electronics

- Hyundai Mobis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automaker Race to Deliver Pillar-to-Pillar Cockpit Displays in China and US Premium Segments

- 4.2.2 Regulatory Push for Advanced Driver Assistance Requiring Larger Digital Instrument Clusters in EU

- 4.2.3 Falling OLED Panel ASPs Triggering OEM Adoption in Mid-Range Passenger Cars

- 4.2.4 Semiconductor Mini-LED Backlighting Enhancing Brightness for EVs in High-Temperature Middle-East Markets

- 4.2.5 Consumer Shift Toward In-Vehicle Streaming and Gaming Driving Demand for Above 12-inch Rear Entertainment Screens

- 4.2.6 Integration of Digital Side Mirrors in Japan and South Korea Following Homologation Approvals

- 4.3 Market Restraints

- 4.3.1 OLED Burn-in Reliability Concerns Limiting Deployment in Taxis/Fleet Vehicles

- 4.3.2 Scarcity of IGZO Backplane capacity Causing 2025 Model Year Delays

- 4.3.3 High BOM Cost of Curved Free-Form Displays Hindering Mass-Market Adoption in India and Brazil

- 4.3.4 Cyber-security Compliance Costs Slowing Aftermarket Retrofits

- 4.4 Industry Ecosystem Analysis

- 4.5 Technology Snapshot

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Display Technology

- 5.1.1 a-Si LCD

- 5.1.2 Oxide LCD (IGZO)

- 5.1.3 LTPS LCD

- 5.1.4 OLED (AMOLED, PMOLED)

- 5.1.5 MicroLED

- 5.1.6 Others (E-paper, Mini-LED Backlit)

- 5.2 By Screen Size

- 5.2.1 Upto 5 inch

- 5.2.2 5.1-8 inch

- 5.2.3 8.1-12 inch

- 5.2.4 Above 12 inch

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.4 By Application

- 5.4.1 Instrument Cluster

- 5.4.2 Center Stack/Infotainment

- 5.4.3 Head-Up Display

- 5.4.4 Rear Seat Entertainment

- 5.4.5 Digital Side/Smart Mirror

- 5.4.6 Others (Roof, HVAC)

- 5.5 By Integration Level

- 5.5.1 Stand-alone Displays

- 5.5.2 Integrated Cockpit/Pillar-to-Pillar

- 5.6 By Touch/Control

- 5.6.1 Touchscreen (capacitive, Resistive)

- 5.6.2 Non-Touch (Display-only)

- 5.7 By Sales Channel

- 5.7.1 OEM-fitted

- 5.7.2 Aftermarket Retrofit

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Nordics

- 5.8.2.5 Rest of Europe

- 5.8.3 South America

- 5.8.3.1 Brazil

- 5.8.3.2 Rest of South America

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 India

- 5.8.4.4 South-East Asia

- 5.8.4.5 Rest of Asia-Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 Middle East

- 5.8.5.1.1 Gulf Cooperation Council Countries

- 5.8.5.1.2 Turkey

- 5.8.5.1.3 Rest of Middle East

- 5.8.5.2 Africa

- 5.8.5.2.1 South Africa

- 5.8.5.2.2 Rest of Africa

- 5.8.5.1 Middle East

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Ranking Analysis

- 6.4 Market Share Analysis

- 6.5 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.5.1 LG Display

- 6.5.2 Samsung Display

- 6.5.3 BOE Technology Group

- 6.5.4 AUO Corporation

- 6.5.5 Innolux Corporation

- 6.5.6 Sharp Corporation

- 6.5.7 Japan Display Inc.

- 6.5.8 Tianma Micro-electronics

- 6.5.9 CSOT (TCL China Star)

- 6.5.10 Visionox

- 6.5.11 Truly Semiconductors

- 6.5.12 HKC Corporation

- 6.5.13 Continental AG

- 6.5.14 Denso Corporation

- 6.5.15 Robert Bosch GmbH

- 6.5.16 Visteon Corporation

- 6.5.17 Panasonic Automotive

- 6.5.18 Nippon Seiki

- 6.5.19 Magna International

- 6.5.20 Marelli

- 6.5.21 Yazaki Corporation

- 6.5.22 Faurecia (Forvia)

- 6.5.23 Desay SV

- 6.5.24 Foryou General Electronics

- 6.5.25 Hyundai Mobis

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment