PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066771

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066771

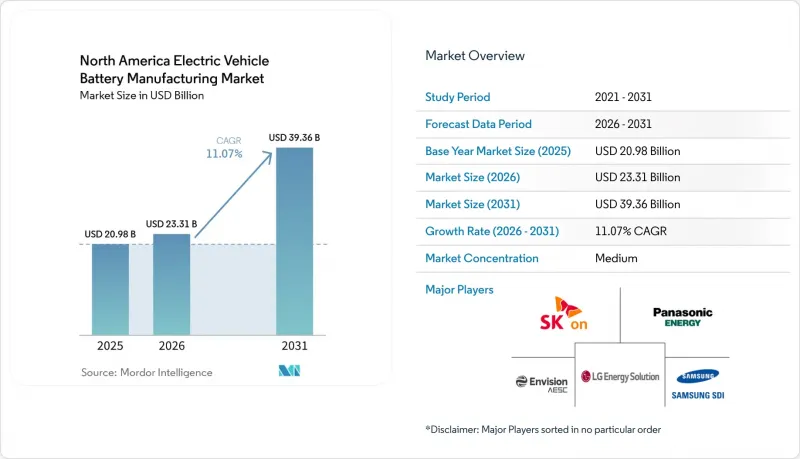

North America Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america electric vehicle battery manufacturing market size is expected to grow from USD 20.98 billion in 2025 to USD 23.31 billion in 2026 and is forecast to reach USD 39.36 billion by 2031 at 11.07% CAGR over 2026-2031.

This report is Segmented by Battery Chemistry (Lithium-Ion, Emerging, Lead-Acid, and Nickel-Metal-Hydride), Cell Format (Cylindrical, Prismatic, and Pouch), Propulsion (Battery Electric Vehicle, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium and Heavy Trucks, Buses and Coaches, and More), and Geography (United States, Canada, and Mexico).

North America Electric Vehicle Battery Manufacturing Market Trends and Insights

IRA-Fuelled Giga-Factory Build-Out

Federal production credits have pushed North America's electric vehicle battery manufacturing market participants to shift from import-led supply toward domestic lines, with 13 new U.S. plants securing Department of Energy loan offers in 2024. Developers are racing to commission facilities before subsidies taper after 2032, locking in advantageous unit economics. Automakers that continue to rely on Asian imports risk forfeiting consumer tax incentives, effectively pricing their vehicles USD 7,500 above models with North American batteries. The resulting localization sprint has converted Midwest and Southeast industrial parks into giga-factory corridors and supplied a visible near-term lift to regional construction and tooling suppliers.

OEM Vertical-Integration Race

Ultium Cells, BlueOval SK, and other captive ventures illustrate how legacy OEMs are rewriting procurement doctrine. General Motors and LG Energy Solution already run three joint plants totaling 140 GWh of capacity, embedding cell cost at book value instead of market value and moderating exposure to volatile lithium and nickel benchmarks. Tesla's dry-electrode patents show an ambition to internalize both assembly and core IP. Vertical integration is viewed as insurance that protects gross margins when spot raw-material contracts swing widely; it also provides bargaining leverage in negotiations with cathode suppliers.

Raw-Material Price Whiplash

Lithium carbonate plunged from USD 85,000 per tonne in 2022 to USD 13,000 per tonne in 2023, then doubled inside six months in 2024. Nickel saw a 35% swing after Indonesian export curbs and Russian sanctions tightened supply. Quarterly renegotiations have replaced long-term offtake contracts, shrinking the gross-margin buffer for cell producers that once hovered near 20%. IRA domestic-content rules restrict sourcing flexibility and lock manufacturers into higher-cost regional feedstock even when global spot benchmarks are cheaper.

Other drivers and restraints analyzed in the detailed report include:

- Regionalisation of Cathode & Anode Supply

- Solid-State Pilot-Line Breakthroughs

- Grid-Capacity & Permitting Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion retained 90.85% of the 2025 North America electric vehicle battery manufacturing market share thanks to mature yields exceeding 95% and energy densities between 250 and 300 Wh/kg. Solid-state, lithium-sulfur, and sodium-ion lines will grow at a 34.08% CAGR through 2031 as OEM pilots graduate to low-volume series production. NMC remains the preferred chemistry for premium ranges above 300 miles, but cobalt cost volatility is accelerating the pivot toward high-nickel NMC 811 blends with just 10% cobalt content. LFP packs are rebounding in North America because their cobalt-free design reduces bill-of-materials risk despite lower energy density.

The North America electric vehicle battery manufacturing market size expansion for emerging chemistries rests on two assumptions: solid-state yields close the gap with conventional lines by 2028, and capex per GWh falls by half through automation. Sodium-ion's lower density constrains it to stationary storage and urban commuter models, yet its abundant raw material offers a hedge against lithium scarcity. Lithium-sulfur research pushes cycle life beyond 150, though deployment remains speculative. Collectively, new chemistries diversify supply risk and extend the regional technology curve without displacing lithium-ion before 2030.

Cylindrical cells held 51.90% of 2025 demand, reflecting Tesla's early laptop-derived designs and mature high-speed winding lines. Prismatic alternatives will move ahead with a 25.32% CAGR through 2031 as automakers favor 20% better volumetric efficiency and simplified pack assembly. Pouch formats keep a mid-teens niche, but recalls tied to swelling episodes highlight quality-control hurdles at scale.

Prismatic growth boosts the North America electric vehicle battery manufacturing market size, where new lines integrate cells directly into the pack, cutting module housings and saving USD 5-8 per kilowatt-hour. Tesla's 4680 cylindrical strategy still aims for a 50% cost cut through tab-less electrodes, though yields under 80% in Austin show the difficulty of scaling the process. BYD and CATL have set a benchmark with blade-style prismatic packs that reach 160 Wh/kg at the pack level and demonstrate crash safety during nail-penetration tests. Automakers are balancing volumetric gains with the risk of shifting to less familiar production tooling.

List of Companies Covered in this Report:

- LG Energy Solution

- Panasonic Energy (w/ Tesla)

- SK On

- Samsung SDI

- AESC Envision

- Ultium Cells (GM + LG)

- CATL USA

- FREYR Battery

- BYD Motors NA

- Contemporary Amperex Technology Ltd.

- American Battery Solutions

- EnerSys

- GS Yuasa Corp

- Exide Industries NA

- Sionic Energy

- Clarios LLC

- Redwood Materials

- Li-Cycle Holdings

- QuantumScape

- Solid Power

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IRA-fuelled giga-factory build-out

- 4.2.2 OEM vertical-integration race

- 4.2.3 Regionalisation of cathode & anode supply

- 4.2.4 Solid-state pilot-line breakthroughs

- 4.2.5 Second-life & recycling credit markets

- 4.2.6 North-American critical-minerals pacts

- 4.3 Market Restraints

- 4.3.1 Raw-material price whiplash

- 4.3.2 Grid-capacity & permitting bottlenecks

- 4.3.3 Skilled-labour shortfall for giga-scale

- 4.3.4 Persisting EV-demand cyclicality

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-ion (NMC, LFP, NCA)

- 5.1.2 Emerging (Solid-state, Li-S, Na-ion)

- 5.1.3 Lead-acid

- 5.1.4 Nickel-metal-hydride

- 5.2 By Cell Format

- 5.2.1 Cylindrical

- 5.2.2 Prismatic

- 5.2.3 Pouch

- 5.3 By Propulsion

- 5.3.1 Battery Electric Vehicle (BEV)

- 5.3.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.3.3 Hybrid Electric Vehicle (HEV)

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Trucks

- 5.4.4 Buses and Coaches

- 5.4.5 Two and Three-wheelers

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 LG Energy Solution

- 6.4.2 Panasonic Energy (w/ Tesla)

- 6.4.3 SK On

- 6.4.4 Samsung SDI

- 6.4.5 AESC Envision

- 6.4.6 Ultium Cells (GM + LG)

- 6.4.7 CATL USA

- 6.4.8 FREYR Battery

- 6.4.9 BYD Motors NA

- 6.4.10 Contemporary Amperex Technology Ltd.

- 6.4.11 American Battery Solutions

- 6.4.12 EnerSys

- 6.4.13 GS Yuasa Corp

- 6.4.14 Exide Industries NA

- 6.4.15 Sionic Energy

- 6.4.16 Clarios LLC

- 6.4.17 Redwood Materials

- 6.4.18 Li-Cycle Holdings

- 6.4.19 QuantumScape

- 6.4.20 Solid Power

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment