PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066773

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066773

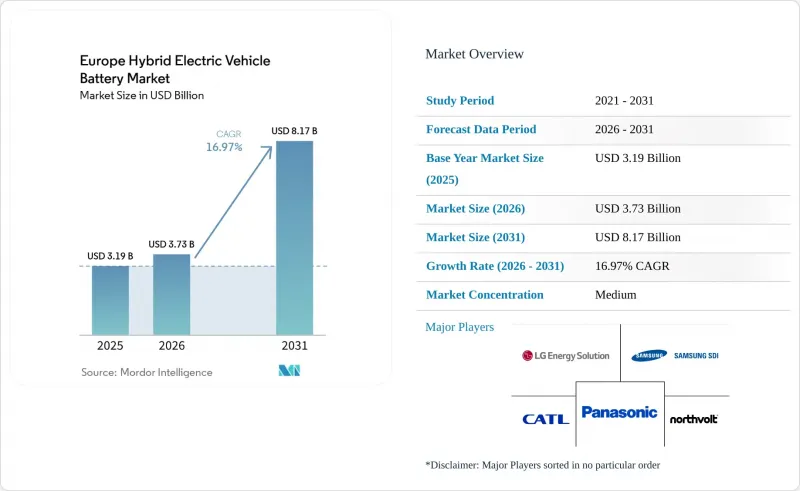

Europe Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe hybrid electric vehicle battery market size is expected to grow from USD 3.19 billion in 2025 to USD 3.73 billion in 2026 and is forecast to reach USD 8.17 billion by 2031 at 16.97% CAGR over 2026-2031.

[1] European Commission, "Proposal for CO2 Emission Performance Standards," ec.europa.eu Mild-hybrid penetration is climbing ahead of full and plug-in variants because the technology delivers 10-15% fuel-economy gains at roughly one-third the system cost of a full hybrid, preserving margin while avoiding expensive charging infrastructure build-outs. [2] Stellantis, "2024 Electrification Strategy," stellantis.com Li-ion chemistries dominated in 2025 with 78.2% volume, as cell makers chase lower material cost and supply-chain resilience. This report is Segmented by Battery Chemistry (Lithium-Ion, Nickel-Metal Hydride, Lead-Acid, and More), Degree of Hybridization (Mild Hybrid, Full Hybrid, and More), Voltage Class (Up To 60V, 60 To 200V, 200 To 400V, and Above 400V), Vehicle Class (Passenger Cars, Commercial Vehicles, Two-/Three-Wheelers, and More), and Geography (Germany, United Kingdom, Spain, Netherlands, and More).

Europe Hybrid Electric Vehicle Battery Market Trends and Insights

Rising HEV Production Volumes Aligned With EU CO2 Fleet Targets

Automakers must meet the 2025 fleet-average ceiling of 93.6 g/km, reduced from 115.1 g/km in 2021, or pay EUR 95 for every excess gram per vehicle sold, pushing brands to standardize hybrid powertrains across high-volume B- and C-segment models. Stellantis, Renault, and Volkswagen expanded 48-volt offerings in 2024, each leveraging belt-starter-generator systems that shave roughly 12 g/km from type-approval emissions for less than a EUR 1,000 cost premium. Because super-credits for zero and low-emission vehicles can still be applied through 2025, building hybrids today generates compliance headroom while BEV infrastructure scales. This rule architecture therefore locks in baseline demand for lithium-ion cells through at least 2027, after which the stricter 2030 targets will intensify electrification pressure.

Gigafactory Investments in CEE Region Localizing Supply Chains

Over EUR 15 billion was committed to new cell plants in Hungary, Poland, and Slovakia during 2024, led by CATL's 100 GWh Debrecen facility and LG Energy Solution's Wroclaw expansion to 70 GWh. The labor arbitrage of 15-20% versus Western Europe, plus just-in-time proximity to German assembly hubs, trims pack lead times to under 24 hours. European Battery Alliance co-financing is accelerating upstream cathode precursor and separator projects that substitute Asia-origin inputs, simultaneously lowering embedded CO2 per kWh. As carbon-footprint declarations become mandatory, local supply chains gain a strategic advantage.

Critical Mineral Cost Volatility

Lithium carbonate prices collapsed from USD 80,000/t in late 2022 to near USD 10,000/t by December 2024, while nickel sulfate swung USD 7,000/t inside a single year. Such turbulence compresses margins on fixed-price supply deals, particularly for smaller European entrants lacking vertical integration. Investors now demand price-adjustment clauses or equity stakes in upstream mines before funding capacity expansions, delaying several gigafactory timelines.

Other drivers and restraints analyzed in the detailed report include:

- Surge in 48-V Mild-Hybrid Architectures

- EU Sustainable-Battery Regulation Incentives

- OEM Cap-ex Shift Toward Full-BEV Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion held 77.60% of 2025 demand, with high-nickel NMC variants powering plug-in hybrids that require 250-280 Wh/kg energy density. LFP gained share in mild-hybrids owing to 3,000-cycle durability and cobalt-free supply chains, a feat demonstrated by BYD's Blade pack that cut system cost 30% for Stellantis models. Emerging sodium-ion and solid-state formats should grow 30.90% annually yet remain sub-scale until after 2026, when Northvolt's pilot line in Sweden starts series output for entry-level hybrids. Nickel-metal-hydride slipped to 7.60% share as Toyota transitioned to new European releases to lithium-ion. The European hybrid electric vehicle battery market sees chemistry bifurcation: cost-sensitive mild hybrids gravitate to LFP and sodium-ion, performance-oriented PHEVs keep high-nickel NMC, and ultra-premium variants pilot solid-state cells.

Advanced chemistries introduce recycling complexity. Solid-state packs using sulfide electrolytes demand novel dismantling and recovery steps that few European recyclers are ready to scale. Simultaneously, cobalt-free formats lighten obligations under Regulation 2023/1542, saving OEMs the EUR 50-80/kWh compliance premium attached to high cobalt content cells. These shifts require gigafactories to design flexible lines capable of chemistry switching without extended downtime, a capability that entrenched Asian incumbents already demonstrate, and new European players must replicate quickly.

The European hybrid electric vehicle battery market recorded 46.70% revenue from mild hybrids in 2025, and this cohort will compound 18.64% annually to 2031. System costs as low as EUR 800 make 48-volt the dominant compliance lever for models such as the Volkswagen Golf and Renault Clio. Full hybrids, typified by Toyota's e-CVT system, held a 28.40% share yet face a slower 10.60% CAGR as European brands redirect engineering budgets. Plug-in hybrids claimed 22.00% revenue but are vulnerable after Germany and the UK scrapped purchase incentives, eroding total-cost-of-ownership parity with BEVs.

Real-world usage data compounds the pressure. A 2024 Transport & Environment study found fleet PHEVs drive less than half their kilometers in electric mode, prompting policymakers to consider tougher utility-factor testing. Absent tax breaks, buyers gravitate either to lower-cost mild hybrids or to BEVs as charging networks improve. Range-extender designs remain below 2.90% share due to packaging complexity and are unlikely to scale before 2031.

List of Companies Covered in this Report:

- BYD Company Ltd

- LG Energy Solution

- Panasonic Holdings Corporation

- Samsung SDI Co., Ltd.

- SK On Co., Ltd.

- EnerSys

- Clarios

- Gotion High-Tech Co Ltd

- Northvolt AB

- Automotive Cells Company (ACC)

- VARTA AG

- CATL Europe

- AESC Envision

- InoBat Auto

- Verkor

- FREYR Battery

- SVOLT Energy Technology

- Saft Groupe S.A.

- Leclanche SA

- E4V

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising HEV production volumes aligned with EU CO? fleet targets

- 4.2.2 Gigafactory investments in CEE region localizing supply chains

- 4.2.3 Declining lithium-ion pack prices in Europe

- 4.2.4 EU sustainable-battery regulation incentives

- 4.2.5 Surge in 48-V mild-hybrid architectures

- 4.2.6 Emergence of sodium-ion batteries for low-cost hybrids

- 4.3 Market Restraints

- 4.3.1 Critical mineral cost volatility

- 4.3.2 OEM cap-ex shift toward full-BEV platforms

- 4.3.3 Cross-border battery-transport regulatory complexity

- 4.3.4 Rise of hydrogen ICE hybrids diverting investment

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 Market Size & Growth Forecasts

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-ion (NMC, NCA, LFP, LTO)

- 5.1.2 Nickel-Metal Hydride (NiMH)

- 5.1.3 Lead-acid

- 5.1.4 Emerging Solid-State/Sodium-ion

- 5.2 By Degree of Hybridization

- 5.2.1 Mild Hybrid (48 V MHEV)

- 5.2.2 Full Hybrid (HEV)

- 5.2.3 Plug-in Hybrid (PHEV)

- 5.2.4 Range-Extender Hybrid

- 5.3 By Voltage Class

- 5.3.1 Up to 60 V

- 5.3.2 60 to 200 V

- 5.3.3 200 to 400 V

- 5.3.4 Above 400 V

- 5.4 By Vehicle Class

- 5.4.1 Passenger Cars

- 5.4.2 Commercial Vehicles

- 5.4.3 Two-/Three-Wheelers

- 5.4.4 Off-Highway and Specialty

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Norway

- 5.5.8 Russia

- 5.5.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 BYD Company Ltd

- 6.4.2 LG Energy Solution

- 6.4.3 Panasonic Holdings Corporation

- 6.4.4 Samsung SDI Co., Ltd.

- 6.4.5 SK On Co., Ltd.

- 6.4.6 EnerSys

- 6.4.7 Clarios

- 6.4.8 Gotion High-Tech Co Ltd

- 6.4.9 Northvolt AB

- 6.4.10 Automotive Cells Company (ACC)

- 6.4.11 VARTA AG

- 6.4.12 CATL Europe

- 6.4.13 AESC Envision

- 6.4.14 InoBat Auto

- 6.4.15 Verkor

- 6.4.16 FREYR Battery

- 6.4.17 SVOLT Energy Technology

- 6.4.18 Saft Groupe S.A.

- 6.4.19 Leclanche SA

- 6.4.20 E4V

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment