PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072468

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072468

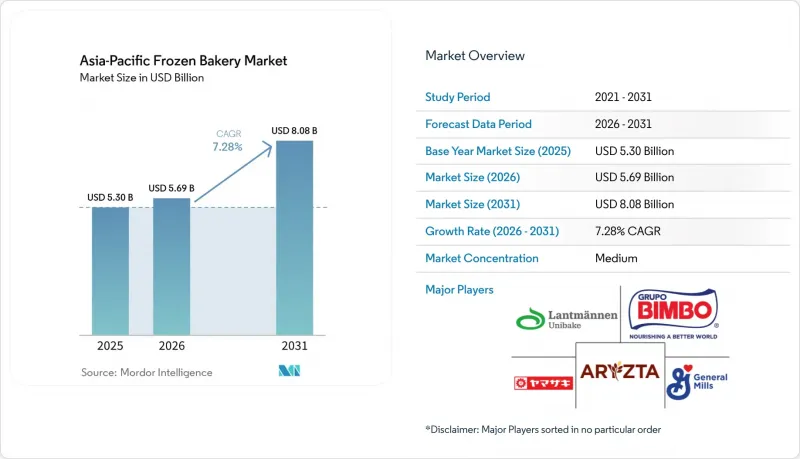

Asia-Pacific Frozen Bakery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the APAC frozen bakery market size is expected to grow from USD 5.3 billion in 2025 to USD 5.69 billion in 2026 and is forecast to reach USD 8.08 billion by 2031 at 7.28% CAGR over 2026-2031.

This report is Segmented by Product Type (Bread, Cakes and Pastries, Pizza, and More), Form (Ready To Cook, Ready To Bake, Ready To Proof, Ready To Eat), End Use (Foodservice, Retail/Household), and Geography (China, India, Japan, Australia, South Korea, Indonesia, Thailand, Malaysia, Vietnam, Philippines, Singapore, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Frozen Bakery Market Trends and Insights

Rising Demand for Convenient Breakfast and Snacking Options

Urban migration fuels single-person households and time-pressed routines, making portable, thaw-and-serve bakery items a staple of daily consumption. Convenience-store majors are scaling aggressively; Seven & i Holdings alone targets 100,000 stores worldwide by 2030, creating an extensive last-mile grid for frozen pastries. South Korean chains such as GS25 have validated premium frozen dessert collaborations, revealing shoppers' willingness to pay for indulgent formats. Indonesia's middle class, heading toward 135 million consumers by 2030, magnifies regional volume potential for Southeast Asia bakery products as expanding incomes meet better refrigeration coverage. Producers equipped with flexible cold-chain networks and portion-controlled SKUs gain a durable edge as breakfast behaviors evolve from fresh-baked daily purchases to stock-and-serve freezer staples.

Expansion of Cold-Chain Logistics and Bake-Off Equipment Penetration

Cold-chain infrastructure development represents a critical enabler for frozen bakery market expansion, particularly in emerging APAC economies where inadequate refrigeration historically constrained market penetration. Indonesia exemplifies this transformation, with government and private sector investments addressing cold-chain inefficiencies that previously caused up to 31% post-harvest losses for temperature-sensitive products. Lotte Global Logistics' USD 55 million investment in a cold-chain distribution center in Vietnam's Dong Nai Province, scheduled for full operation by May 2026, demonstrates the scale of infrastructure investments required to support frozen product distribution across Southeast Asia. The integration of advanced monitoring technologies, including real-time temperature sensors and blockchain-based traceability systems, addresses quality assurance concerns that previously limited consumer acceptance of frozen bakery products. Bake-off equipment penetration in retail environments enables the "fresh-baked" positioning that bridges the quality perception gap between frozen and fresh products, with retailers adopting ready-to-bake formats that require minimal skilled labor while maintaining artisanal appearance. The Philippines Cold Chain Project, supported by USDA funding from 2013-2018, provides a template for public-private partnerships that accelerate infrastructure development in markets where private investment alone proves insufficient.

Fresh-versus-Frozen Quality Perception Gap

Consumer perception challenges regarding frozen bakery quality relative to fresh alternatives constrain market penetration despite technological advances in freezing and preservation techniques. Traditional bakery cultures in markets like Japan and rural China maintain strong preferences for daily-fresh products, creating resistance to frozen alternatives even when nutritional and taste profiles prove comparable. The Real Bread Campaign's distinction between "real bread" and industrial bread made through processes like Chorleywood, which affects approximately 80% of UK breads, illustrates how processing methods influence consumer perception and acceptance. Gardenia Philippines' implementation of G-Lock color-coded packaging systems that indicate baking dates represents industry efforts to bridge freshness perception gaps through transparency and visual cues. The challenge extends beyond consumer education to encompass operational execution, as temperature fluctuations during distribution and inadequate in-store handling can compromise product quality and reinforce negative perceptions. Overcoming these barriers requires sustained investment in consumer education, supply chain optimization, and product innovation that demonstrably matches or exceeds fresh product attributes while maintaining the convenience advantages that justify frozen formats.

Other drivers and restraints analyzed in the detailed report include:

- Premiumisation & Health-Driven New Product Development

- Retail Adoption of In-Store Thaw-and-Serve Programmes

- Rising Energy & Refrigeration Costs in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bread maintained a 32.21% share in 2025, cementing its status as a staple across diverse dietary cultures. The APAC frozen bakery market size for bread reflects efficient large-scale production and broad retail reach. Yet morning goods such as muffins, pancakes, and sweet buns are forecast for a 9.52% CAGR, outpacing all other categories. Morning goods satisfy an experiential breakfast trend tied to cafe culture in metropolitan centers from Shanghai to Sydney. Lotus Bakeries' forthcoming Biscoff facility in Thailand demonstrates capital commitment to satisfy demand for premium coffee-paired treats. Partnerships between Lotus Bakeries and Mondelez in India envision co-branded chocolate applications that can migrate into frozen pastry shells, illustrating cross-category growth synergies.

Morning goods also carry functional upgrades, including high-protein waffles and reduced-sugar Danish pastries enabled by sweet protein technology. As portion-controlled indulgence gains traction among health-conscious millennials, the APAC frozen bakery market keeps bread as its volume bedrock yet leans on morning goods for value elasticity and brand storytelling. The blend of indulgence and health credentials positions this sub-segment as a profit driver through 2031.

Complete Report Scope:

- By Product Type

- Bread

- Cakes and Pastries

- Pizza Crust

- Morning Goods

- Viennoiserie and Danish

- Other Product Types

- By Form

- Ready to Cook

- Ready to Bake

- Ready to Proof

- Ready to Eat

- By End Use

- Foodservice (QSR, Bakeries, HoReCa, Catering)

- Retail/ Househod

- Supermarkets / Hypermarkets

- Convenience Stores

- Specialty Bakery Stores

- Online Retail / E-commerce

- Others

- By Geography

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Malaysia

- Vietnam

- Philippines

- Singapore

- New Zealand

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Lantmannen Unibake

- Grupo Bimbo

- General Mills

- McCain Foods

- Ajinomoto

- Conagra Brands

- Flower Foods

- Nestle SA

- Pasco Shikishima

- Aryzta AG

- Yamazaki Baking

- Vandemoortele

- Europastry

- Rich Products Corp.

- Dawn Food Products

- J&J Snack Foods

- Goodman Fielder

- BreadTalk Group

- TongTech Holdings

- CJ CheilJedang

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for convenient breakfast and snacking options

- 4.2.2 Expansion of cold-chain logistics and bake-off equipment penetration

- 4.2.3 Premiumisation & health-driven New Product Development (gluten-free, high-protein, clean-label)

- 4.2.4 Retail adoption of in-store thaw-and-serve programmes

- 4.2.5 Local-flavour hybrid products gaining acceptance across APAC

- 4.2.6 Enhanced customization options for product formats targeting specific consumption occasions.

- 4.3 Market Restraints

- 4.3.1 Fresh-versus-frozen quality perception gap

- 4.3.2 Rising energy & refrigeration costs in emerging markets

- 4.3.3 Tariff and regulatory risk on imported butter/dairy inputs

- 4.3.4 Carbon-footprint rules targeting high-energy frozen supply chains

- 4.4 Cinsumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Bread

- 5.1.2 Cakes and Pastries

- 5.1.3 Pizza Crust

- 5.1.4 Morning Goods

- 5.1.5 Viennoiserie and Danish

- 5.1.6 Other Product Types

- 5.2 By Form

- 5.2.1 Ready to Cook

- 5.2.2 Ready to Bake

- 5.2.3 Ready to Proof

- 5.2.4 Ready to Eat

- 5.3 By End Use

- 5.3.1 Foodservice (QSR, Bakeries, HoReCa, Catering)

- 5.3.2 Retail/ Househod

- 5.3.2.1 Supermarkets / Hypermarkets

- 5.3.2.2 Convenience Stores

- 5.3.2.3 Specialty Bakery Stores

- 5.3.2.4 Online Retail / E-commerce

- 5.3.2.5 Others

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 Indonesia

- 5.4.7 Thailand

- 5.4.8 Malaysia

- 5.4.9 Vietnam

- 5.4.10 Philippines

- 5.4.11 Singapore

- 5.4.12 New Zealand

- 5.4.13 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Lantmannen Unibake

- 6.4.2 Grupo Bimbo

- 6.4.3 General Mills

- 6.4.4 McCain Foods

- 6.4.5 Ajinomoto

- 6.4.6 Conagra Brands

- 6.4.7 Flower Foods

- 6.4.8 Nestle SA

- 6.4.9 Pasco Shikishima

- 6.4.10 Aryzta AG

- 6.4.11 Yamazaki Baking

- 6.4.12 Vandemoortele

- 6.4.13 Europastry

- 6.4.14 Rich Products Corp.

- 6.4.15 Dawn Food Products

- 6.4.16 J&J Snack Foods

- 6.4.17 Goodman Fielder

- 6.4.18 BreadTalk Group

- 6.4.19 TongTech Holdings

- 6.4.20 CJ CheilJedang

7 Market Opportunities and Future Outlook