PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072474

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072474

Password Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

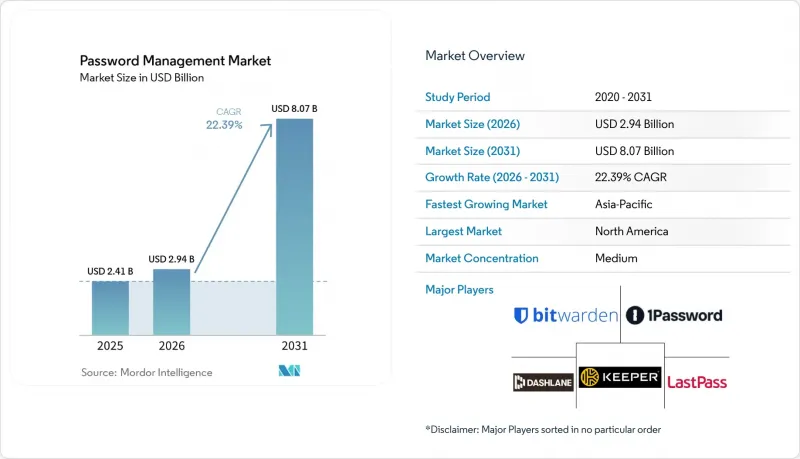

According to Mordor Intelligence, the password management market size is projected to expand from USD 2.41 billion in 2025 and USD 2.94 billion in 2026 to USD 8.07 billion by 2031, registering a CAGR of 22.39% between 2026 to 2031.

This report is Segmented by Solution Type (Self-Service, and Privileged User), Access / Technology Type (Desktop and Laptop, and More), Deployment Mode (Cloud-Hosted, On-Premises, and Hybrid), Enterprise Size (Large, and SMEs), End-User Vertical (BFSI, Healthcare, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Password Management Market Trends and Insights

Zero-Trust Programs Accelerating Privileged Password Vault Deployments in North American BFSI

Regulators linked credential misuse to unauthorized trading and loan-fraud incidents in 2024 and 2025, prompting United States and Canadian banks to embed privileged vaults into zero-trust architectures. The Office of the Comptroller of the Currency required institutions with assets above USD 10 billion to provide just-in-time access and session recording for every administrative account. CyberArk noted that 68% of its first-half 2025 bookings came from financial-services upgrades to dynamic privileged access management vaults that rotate passwords every 90 minutes. Mid-tier banks lacking appliance budgets turned to cloud-delivered privileged access, a capability rapidly expanded by Delinea in 2025. Similar mandates are emerging in Europe and the Asia Pacific, indicating global spillover.

EU GDPR and NIS-2 Mandates Triggering Enterprise-Wide Password Audits and Upgrades

The Network and Information Security Directive 2 entered full force in October 2024 and, together with GDPR, compelled European firms to inventory every credential across subsidiaries and supply-chain partners. Fines linked to weak password hygiene totaled EUR 1.2 billion (USD 1.3 billion) over 2024-2025 and elevated password vault roll-outs above other security projects. Germany, France and the Netherlands spearheaded hybrid architectures that keep privileged passwords on-premises while routing employee credentials to managed cloud vaults. Non-EU corporations serving European customers must also comply, broadening global demand.

High-Profile Breaches Undermining User Trust, Especially in DACH Region

The 2022 LastPass breach revealed encrypted vault data and unencrypted metadata, triggering a lingering trust deficit across Germany, Austria and Switzerland. Many organizations pivoted to on-premises or open-source options such as Bitwarden, citing transparency advantages over proprietary encryption. Germany's Federal Office for Information Security urged independent vendor assessments in 2024. Until vendors embrace standardized encryption and continuous third-party audits, caution in the DACH region will restrain cloud adoption.

Other drivers and restraints analyzed in the detailed report include:

- Surge in SaaS Identity Sprawl Creating Demand for Cross-Platform Vaults in Asia Pacific Mid-Market

- API-First Integration Needs for RPA and DevOps Pipelines Fueling Secrets-Management Adoption

- Rising Adoption of Passkeys and FIDO2 Reducing Future TAM in Consumer Segment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Privileged password tools represented the fastest-growing solution, advancing at a 23.8% CAGR through 2031, while self-service applications, although larger today, face growth deceleration. Banking, healthcare, and public-sector mandates now require credential rotation, access logging, and separation of duties, capabilities embedded only in privileged platforms. Cyber-insurance clauses reinforce the shift by denying favorable premiums to firms that rely on static spreadsheets.

Self-service tools held a 46.5% market share in 2025. Self-service vendors continue to enhance enterprise features, yet remain susceptible to the consumer shift toward passkeys. Hybrid work introduces new endpoints and expands the password management market, but the security premium associated with administrative accounts ensures that privileged vaults continue to drive growth.

Mobile solutions hold the strongest tailwind, forecast to rise at 24.1% to 2031, whereas desk-based clients maintain 38.1% of 2025 spending. The Nordic model has demonstrated that biometric-enabled vaults on smartphones can improve both user experience and compliance simultaneously. iCloud Keychain and Windows Hello now incorporate passkey storage, intensifying competitive pressure on independent vendors and making differentiated cross-platform support mandatory.

Growth in the password management market stems from remote work and 5G connectivity that allow real-time credential sync without latency. Desktops and laptops remain indispensable for developers and analysts, ensuring multipronged access strategies prevail.

Complete Report Scope:

- By Solution Type

- Self-Service Password Management

- Privileged User Password Management

- By Access/Technology Type

- Desktop and Laptop

- Mobile Devices

- Voice-Enabled Password Reset

- Browser Extensions and Web Vaults

- By Deployment Mode

- Cloud-Hosted

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Vertical

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- IT and Telecommunications

- Government and Public Sector

- Retail and E-Commerce

- Manufacturing

- Education

- Other End-User Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Geography Analysis

North America contributed 38.9% of 2025 revenue, propelled by zero-trust mandates, cyber-insurance terms, and a mature cloud landscape. United States banks responded swiftly to the new OCC guidance, while Canadian institutions followed a similar pattern of integration. Growth will gradually moderate as enterprise penetration peaks, and attention shifts to small and medium-sized organizations.

The Asia Pacific is projected to post the fastest regional CAGR of 24.13% through 2031. Cloud-first government projects, a vibrant startup ecosystem, and widespread mobile internet drive demand for cross-platform vaults. India and Southeast Asia exhibit the sharpest adoption curves, while Japan and South Korea focus on regulatory compliance and workforce mobility.

Europe demonstrates robust hybrid deployments under the pressures of GDPR and NIS-2. DACH markets remain cautious, favoring open-source or self-hosted solutions in the wake of the LastPass incident. Elsewhere, regulations on data localization in Russia and parts of the Middle East and Africa are fostering local vendor ecosystems, ensuring the password management market retains regional nuances.

- LastPass (GoTo)

- 1Password (AgileBits)

- Dashlane Inc.

- Keeper Security, Inc.

- Bitwarden, Inc.

- CyberArk Software Ltd.

- Delinea

- Microsoft Corporation

- IBM Corporation

- Apple Inc.

- Broadcom (CA Technologies)

- Okta Inc.

- SailPoint Technologies, Inc.

- Quest Software Inc.

- Hitachi ID Systems

- FastPassCorp A/S

- Avatier

- Trend Micro Incorporated

- Ivanti

- HashiCorp

- Thycotic

- BeyondTrust Corporation

- EmpowerID, Inc.

- Intuitive Security Systems Pty. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Zero-Trust Programs Accelerating Privileged Password Vault Deployments in North American BFSI

- 4.2.2 EU GDPR and NIS-2 Mandates Triggering Enterprise-wide Password Audits and Upgrades

- 4.2.3 Surge in SaaS Identity Sprawl Creating Demand for Cross-Platform Vaults in Asia Pacific Mid-Market

- 4.2.4 Workforce Mobility and BYOD Driving Mobile-First Password Managers in Nordics

- 4.2.5 Cyber-Insurance Underwriting Requiring Automated Credential Hygiene Proof in United States

- 4.2.6 API-First Integration Needs for RPA and DevOps Pipelines Fueling Secrets Management Adoption

- 4.3 Market Restraints

- 4.3.1 High-Profile Breaches (e.g., LastPass 2022) Undermining User Trust, Especially in DACH Region

- 4.3.2 Rising Adoption of Passkeys/FIDO2 Reducing Future TAM in Consumer Segment

- 4.3.3 Regulatory Data-Residency Rules Complicating Cloud Vault Roll-Outs in Middle East

- 4.3.4 Persistent Shadow-IT Password Stores Inflating Migration Costs for Large Enterprises

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory and Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 Self-Service Password Management

- 5.1.2 Privileged User Password Management

- 5.2 By Access/Technology Type

- 5.2.1 Desktop and Laptop

- 5.2.2 Mobile Devices

- 5.2.3 Voice-Enabled Password Reset

- 5.2.4 Browser Extensions and Web Vaults

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Hosted

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By End-User Vertical

- 5.5.1 Banking, Financial Services and Insurance (BFSI)

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 IT and Telecommunications

- 5.5.4 Government and Public Sector

- 5.5.5 Retail and E-Commerce

- 5.5.6 Manufacturing

- 5.5.7 Education

- 5.5.8 Other End-User Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 LastPass (GoTo)

- 6.4.2 1Password (AgileBits)

- 6.4.3 Dashlane Inc.

- 6.4.4 Keeper Security, Inc.

- 6.4.5 Bitwarden, Inc.

- 6.4.6 CyberArk Software Ltd.

- 6.4.7 Delinea

- 6.4.8 Microsoft Corporation

- 6.4.9 IBM Corporation

- 6.4.10 Apple Inc.

- 6.4.11 Broadcom (CA Technologies)

- 6.4.12 Okta Inc.

- 6.4.13 SailPoint Technologies, Inc.

- 6.4.14 Quest Software Inc.

- 6.4.15 Hitachi ID Systems

- 6.4.16 FastPassCorp A/S

- 6.4.17 Avatier

- 6.4.18 Trend Micro Incorporated

- 6.4.19 Ivanti

- 6.4.20 HashiCorp

- 6.4.21 Thycotic

- 6.4.22 BeyondTrust Corporation

- 6.4.23 EmpowerID, Inc.

- 6.4.24 Intuitive Security Systems Pty. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment