PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072496

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072496

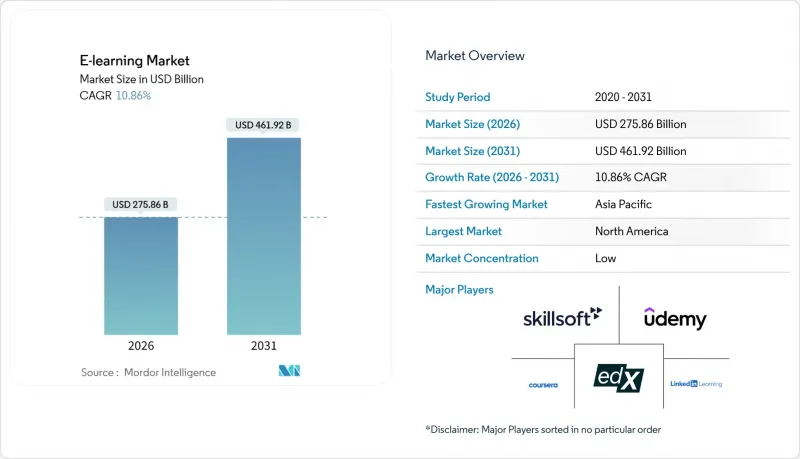

E-learning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the global e-learning market size is projected to grow from USD 275.86 billion in 2026 to USD 461.92 billion by 2031, reflecting a robust compound annual growth rate (CAGR) of 10.86% over the five years.

This report is Segmented by Delivery Mode (Self-Paced and Instructor-Led), Deployment (Cloud and On-Premise), Technology (Online E-Learning, Learning Management System (LMS), and More), End-User (Academic, Corporate, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global E-learning Market Trends and Insights

Growing Penetration of Smartphones and High-Speed Internet

Mobile access and better connectivity are reshaping how people engage with online learning and skills development. According to OECD PISA 2022 data, 98% of 15-year-olds across OECD countries own a smartphone, and 96% have access to a desktop, laptop, or tablet at home, lowering barriers to video lessons, tutoring, and coursework outside school hours. At the same time, 79 education systems worldwide, representing 40% of global systems, have implemented smartphone restrictions or bans in classrooms by the end of 2024 to protect attention and learning outcomes, per UNESCO monitoring, while permitting after-school use for homework and supplemental learning . The coexistence of classroom restrictions and strong out-of-school mobile use pushes providers to invest in features like offline modes, low-bandwidth formats, and content that fits short sessions. This environment helps the e-learning market extend reach among learners who have smartphones but inconsistent broadband, especially in rural districts and emerging markets where mobile-first strategies carry the most impact.

Corporate Up-Skilling Demand Amid Digital Transformation

Labor markets in 2026 prioritize speed-to-skill, making structured, outcomes-based programs central to enterprise learning roadmaps. A survey conducted by edX in 2025 found that most working-age adults considering training intended to act within months, pointing to concrete timelines that learning leaders must meet with scalable programs that align with job requirements. Public education systems are shifting to formalize AI literacy and practice through required professional learning days and resources that guide safe, effective classroom use. For instance, Ontario's Ministry of Education mandated AI as a topic for Professional Activity Days in 2025-26, requiring educators to discuss AI's role in teaching, explore approved tools for writing and critical thinking, and align with the Ontario Trustworthy AI Framework and cybersecurity policies. National strategies to address digital talent gaps in the public sector are driving evergreen training plans with explicit AI components, such as the UK Cabinet Office's One Big Thing 2025 initiative, which will train all civil servants on AI essentials, practical applications for streamlining work, and innovation in public services starting in autumn 2025. These efforts expand addressable demand for platforms that deliver role-aligned learning at government scale.

Other drivers and restraints analyzed in the detailed report include:

- Government Initiatives for Digital Education

- Cost Advantages Over Classroom Training

- Low Completion Rates and Learner-Engagement Challenges

- Digital Divide in Rural and Low-Income Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-paced learning accounts for 58.37% of the market in 2025, reflecting a strong preference for flexible, on-demand access that supports self-directed practice. Instructor-led formats are projected to grow at a 12.76% CAGR through 2031, driven by enterprises blending live coaching with asynchronous content to enhance confidence and completion rates. Managers increasingly request role-specific simulations, such as Udemy's October 2025 AI Role Play launch with over 10,000 simulations tied to certifications and feedback sessions, reducing performance risks. Platforms integrating AI assistance achieve 76% efficiency gains, as per Didask benchmarks, complementing instructor time and scaling live support across languages for large learner groups.

Corporate and public-sector buyers are formalizing AI up-skilling and digital literacy requirements, using live sessions to align teams with responsible practices and organizational frameworks. This shift strengthens hybrid designs, where instructor-led touchpoints introduce tools, assess readiness, and standardize workflows, while asynchronous content addresses knowledge gaps. Over the forecast period, the e-learning industry is expected to sustain both modes as complementary channels serving distinct objectives. Live formats will remain essential for onboarding, leadership, and soft skills, while self-paced modules will anchor knowledge acquisition and practice.

Cloud-based deployment, holding 54.37% of the base in 2025, is projected to grow at an 11.77% CAGR through 2031. Enterprises favor faster updates, elastic capacity, and multi-tenant architecture for simplified administration. The e-learning market supports this shift by focusing on security, regional hosting, and compliance integrations for regulated industries. Cloud platforms enable features like AI coaching and analytics without on-premises maintenance, ensuring continuous improvement and uptime for global users. Subscription models illustrate how enterprises scale across teams and geographies while reducing costs and consolidating vendors. As institutions standardize on fewer platforms, cloud-first strategies enhance speed and lower the total cost of ownership compared to on-premises solutions.

On-premises implementations will remain in defense and sensitive environments requiring network isolation. However, the e-learning market increasingly prioritizes cloud features. Product roadmaps emphasize privacy controls, consent management, and accessibility to meet institutional and student protection requirements, boosting confidence in hosted solutions. Cloud-native analytics link course activity to skill signals and credentials, proving outcomes and supporting career mobility. Procurement frameworks focusing on data protection and AI transparency favor cloud platforms with certifications and regional coverage. These factors position cloud deployment as the foundation of the e-learning industry through 2031.

Complete Report Scope:

- By Delivery Mode

- Self-Paced

- Instructor-Led

- By Deployment

- Cloud

- On-Premise

- By Technology

- Online e-learning

- Learning Management System (LMS)

- Mobile e-learning

- Rapid e-learning

- Virtual Classroom

- By End-User

- Academic

- Corporate

- Government & Public Sector

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Geography Analysis

North America held a 34.74% market share in 2025, supported by a strong ecosystem of platforms, content partners, and enterprise buyers sustaining digital learning post-pandemic. Institutional and government actions in 2026 are reinforcing digital literacy and responsible AI practices in schools and public services, driving long-term adoption. United States and Canadian initiatives to build AI-ready workforces are increasing demand for certifications, structured learning pathways, and compliance-ready vendors. Private-sector buyers are expanding subscriptions and role-based learning programs integrated with enterprise systems, committing to multi-year digital training. Rural connectivity gaps and potential telecom funding shifts create uncertainties for subsidized broadband, affecting community institutions. Growth in this mature market is tied to AI-native features, micro-credentials, and evidence.

Europe continues implementing the EU Digital Education Action Plan in 2026, advancing educator readiness, system resilience, and digital transformation goals in schools and higher education. Policies addressing digital skills and teacher support bridge readiness gaps and secure multi-year budgets for infrastructure, content, and platforms across member states. Procurement prioritizes privacy, safety, and accessibility, favoring platforms compliant with EU frameworks and national guidelines. Multilingual content and localization influence adoption across diverse language communities. As hybrid models and learning analytics become embedded, steady procurement cycles and cross-border partnerships align credentials with labor market needs. AI literacy and responsible use strengthen the case for AI-native platforms in higher education and enterprise contexts.

Asia-Pacific is projected to grow at an 8.87% CAGR through 2031, driven by internet access gains, mobile-first learning behavior, and policy pushes for digital skills in schools and workplaces. Governments and employers are investing in AI and data capability programs, expanding demand for role-aligned courses and professional certificates. Mobile access and offline capabilities shape product choices in rural and peri-urban areas. Privacy and safety mandates guide platform design, while partnerships with universities and large employers anchor market strategies.

- Coursera Inc.

- Udemy Inc.

- LinkedIn Learning

- edX (2U Inc.)

- Skillsoft

- Pluralsight

- Blackboard Inc.

- Instructure (Canvas)

- Cornerstone OnDemand

- Moodle

- Docebo S.p.A.

- Pearson plc

- SAP Litmos

- G-Cube

- Chegg Inc.

- Udacity

- D2L Corp. (Brightspace)

- Google LLC (Classroom)

- Aptara

- FutureLearn Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing penetration of smartphones & high-speed internet

- 4.2.2 Corporate up-skilling demand amid digital transformation

- 4.2.3 Government initiatives for digital education

- 4.2.4 Cost advantages over classroom training

- 4.2.5 Rise of micro-credential partnerships between universities & Big Tech

- 4.2.6 EdTech venture funding shift toward emerging markets

- 4.3 Market Restraints

- 4.3.1 Low completion rates & learner-engagement challenges

- 4.3.2 Digital divide in rural & low-income areas

- 4.3.3 Content-localization barriers for multilingual markets

- 4.3.4 Data-privacy regulatory complexity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Consumer Behavior Insights in the E-Learning Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, US$ bn)

- 5.1 By Delivery Mode

- 5.1.1 Self-Paced

- 5.1.2 Instructor-Led

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By Technology

- 5.3.1 Online e-learning

- 5.3.2 Learning Management System (LMS)

- 5.3.3 Mobile e-learning

- 5.3.4 Rapid e-learning

- 5.3.5 Virtual Classroom

- 5.4 By End-User

- 5.4.1 Academic

- 5.4.2 Corporate

- 5.4.3 Government & Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Coursera Inc.

- 6.4.2 Udemy Inc.

- 6.4.3 LinkedIn Learning

- 6.4.4 edX (2U Inc.)

- 6.4.5 Skillsoft

- 6.4.6 Pluralsight

- 6.4.7 Blackboard Inc.

- 6.4.8 Instructure (Canvas)

- 6.4.9 Cornerstone OnDemand

- 6.4.10 Moodle

- 6.4.11 Docebo S.p.A.

- 6.4.12 Pearson plc

- 6.4.13 SAP Litmos

- 6.4.14 G-Cube

- 6.4.15 Chegg Inc.

- 6.4.16 Udacity

- 6.4.17 D2L Corp. (Brightspace)

- 6.4.18 Google LLC (Classroom)

- 6.4.19 Aptara

- 6.4.20 FutureLearn Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment