PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072502

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072502

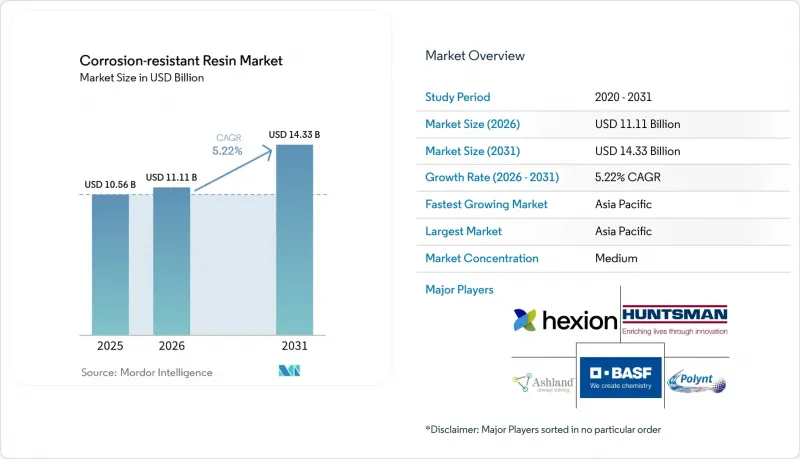

Corrosion-resistant Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the corrosion-resistant resin market size in 2026 is estimated at USD 11.11 Billion, growing from 2025 value of USD 10.56 Billion with 2031 projections showing USD 14.33 Billion, growing at 5.22% CAGR over 2026-2031.

This report is Segmented by Resin Type (Epoxy, Vinyl Ester, Polyester, Polyurethane, and Others), Application (Composites, Coatings, and Others), End-User Industry (Automotive and Transportation, Infrastructure, Marine, Oil and Gas, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Corrosion-resistant Resin Market Trends and Insights

Increasing Demand for Epoxy Resins

Epoxy resins continue to redefine corrosion management because nano-silica-filled matrices are delivering higher barrier performance and longer service intervals. Fluorescence-enabled coatings allow visual detection of microcracks, supporting proactive maintenance on offshore platforms where inspection windows are limited . Regulators' focus on sustainability is catalyzing commercial roll-out of vegetable-oil-derived epoxies that match incumbent mechanical properties while lowering carbon footprints. Self-healing chemistries that trigger inhibitor release in response to temperature spikes are further positioning epoxies as the workhorse for next-generation protective systems. Collectively, these advances boost asset uptime and compress total cost of ownership for heavy-industry end-users.

Rising Corrosion-related CAPEX (Capital Expenditures) and OPEX (Operational Expenditures) in Oil & Gas Pipelines

Pipeline operators confront corrosion costs of roughly USD 1.372 Billion annually, prompting adoption of nonmetallic pipe networks and advanced resin-rich liners. Aramco has already installed over 10,000 km of reinforced thermoplastic pipe to mitigate sweet-gas corrosion in desert and offshore environments. New resin systems qualified for 198.33 MPa and 352.25°C downhole conditions are unlocking deep-reservoir completions while reducing downtime linked to tubing failures. Response-surface corrosion modelling lets engineers tailor resin selection to local chloride and CO2 levels, lowering lifecycle spend and enhancing safety metrics. These economics underpin sustained purchasing of high-performance corrosion-resistant resin market solutions by energy majors.

REACH and TSCA Re-classification of Bisphenol-a

Europe's sharp reduction of Bisphenol-A (BPA) tolerable daily intake and the United States' antidumping levies on Asian epoxy imports are forcing formulators to pivot toward Bisphenol A (BPA)-free chemistries. Sherwin-Williams and PPG Industries, Inc. now market non-Bisphenol A (BPA) container linings, while Roquette's isosorbide-based hardeners preserve chemical resistance without endocrine-disruption concerns . Supply uncertainty during the transition period elevates production costs and may slow qualification cycles for new aerospace and food-contact applications.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting Trend in Wind-blade Composites

- Mainstream Shift to Water-borne Vinyl-ester Systems in Marine

- Volatile MDI Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The epoxy segment commanded 42.38% of the Corrosion-resistant Resin market share in 2025, anchored by its bonding strength, chemical inertness, and adaptability across marine, oil and gas, and infrastructure projects. Epoxy-based formulations infused with bis-silane modifiers now achieve self-healing rates above 90% after salt-spray exposure, extending maintenance intervals for offshore installations. Polyurethane's 5.74% CAGR reflects its rapid curing, which cuts blade cycle times and lowers capital tied up in molds, propelling its use in 100-m class wind blades. Vinyl esters retain a foothold in chemical-tank fabrication because their ester linkage tolerates acids and solvents that attack conventional polyesters.

Emerging smart-resin platforms integrate fluorescent tracers for early-stage crack visibility and temperature-responsive inhibitor release, supporting predictive maintenance programs that slash unplanned downtime by up to 25% for refinery operators. These advances reinforce epoxy's premium positioning even as alternative chemistries race to close performance gaps.

Complete Report Scope:

- By Resin Type

- Epoxy

- Vinyl Ester

- Polyester

- Polyurethane

- Others

- By Application

- Composites

- Coatings

- Others (Adhesives & Linings)

- By End-User Industry

- Automotive and Transportation

- Food and Beverage

- Industrial

- Infrastructure

- Marine

- Oil and Gas

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Geography Analysis

Asia Pacific accounted for 38.21% of the Corrosion-resistant Resin market revenue in 2025 and is projected to expand at a 6.35% CAGR to 2031, cementing its leadership position. China's annual installation of over 30 GW of new wind capacity drives bulk consumption of glass-fiber-epoxy resins for blades and nacelles. India's contract manufacturing, highlighted by Kineco Exel's qualification for Vestas carbon-fiber planks, signals rising local value-addition in advanced composites. Taiwan's Swancor supplies more than 50% of material input for regional offshore wind projects, reflecting supply-chain maturation.

North America captures demand through technological innovation and trade policy. United States antidumping duties on certain Asian epoxy imports shield domestic players and encourage capacity expansions, ensuring a secure supply for defense and infrastructure applications. ExxonMobil's collaboration with McClarin Composites on polyolefin-based thermosets underscores the region's push for lower-carbon alternatives that maintain tensile performance. BASF already operates coating plants on 100% renewable electricity, reducing scope-2 emissions while holding throughput steady.

Europe prioritizes sustainability and regulatory leadership, prompting rapid commercialisation of BPA-free epoxies and bio-attributed intermediates under stringent Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) frameworks. Middle East and Africa accelerate through localization plans such as Sadara's PlasChem Park, geared toward anticorrosion products, while Strata-Solvay's prepreg facility positions the United Arab Emirates as an aerospace material supplier. South America's industrialization and port upgrades sustain moderate resin demand, yet the region trails in composite expertise and remains import-reliant for key intermediates.

- Aditya Birla Chemicals

- AOC Resins

- Ashland Inc.

- BASF SE

- DIC Corporation

- Guangdong Yinyang Environment-Friendly New Materials Co., Ltd.

- Hexion Inc.

- Huntsman Corporation

- Olin Corporation

- Polynt-Reichhold Group

- Resonac

- Scott Bader Co. Ltd.

- Sino Polymer Co. Ltd.

- Sir Industriale

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Epoxy Resins

- 4.2.2 Rising Corrosion-related CAPEX (Capital Expenditures) and OPEX (Operational Expenditures) in Oil & Gas Pipelines

- 4.2.3 Light-weighting Trend in Wind-blade Composites

- 4.2.4 Mainstream Shift to Water-borne Vinyl-ester Systems in Marine

- 4.2.5 Localized Resin Blenders Emerging Around Middle-east Tank-farm Clusters

- 4.3 Market Restraints

- 4.3.1 REACH and TSCA Re-classification of Bisphenol-a

- 4.3.2 Volatile MDI Prices

- 4.3.3 Lack of Skilled Composite Fabricators in the Middle East and Africa

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Vinyl Ester

- 5.1.3 Polyester

- 5.1.4 Polyurethane

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Composites

- 5.2.2 Coatings

- 5.2.3 Others (Adhesives & Linings)

- 5.3 By End-User Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Food and Beverage

- 5.3.3 Industrial

- 5.3.4 Infrastructure

- 5.3.5 Marine

- 5.3.6 Oil and Gas

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Aditya Birla Chemicals

- 6.4.2 AOC Resins

- 6.4.3 Ashland Inc.

- 6.4.4 BASF SE

- 6.4.5 DIC Corporation

- 6.4.6 Guangdong Yinyang Environment-Friendly New Materials Co., Ltd.

- 6.4.7 Hexion Inc.

- 6.4.8 Huntsman Corporation

- 6.4.9 Olin Corporation

- 6.4.10 Polynt-Reichhold Group

- 6.4.11 Resonac

- 6.4.12 Scott Bader Co. Ltd.

- 6.4.13 Sino Polymer Co. Ltd.

- 6.4.14 Sir Industriale

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Integration of Nanotechnology into Resin Formulations