PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072516

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072516

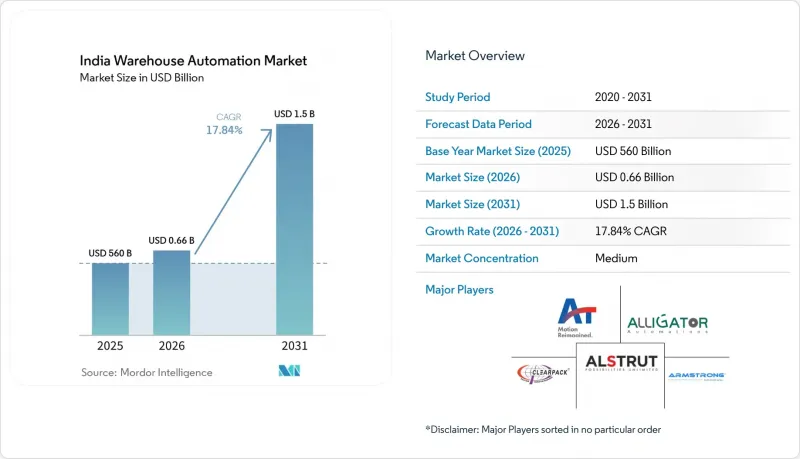

India Warehouse Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india warehouse automation market size is expected to grow from USD 560 million in 2025 to USD 659.96 million in 2026 and is forecast to reach USD 1.5 billion by 2031 at 17.84% CAGR over 2026-2031.

This report is Segmented by Component (Hardware, Software, and Services), Automation Level (Basic Mechanization, Semi-Automated Systems, and Fully Automated Robotics/AS-RS), Function (Picking and Sorting, Palletizing and Depalletizing, Storage and Retrieval, and More), and End-User Industry (E-Commerce and 3PL, FMCG and Retail, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Warehouse Automation Market Trends and Insights

Explosive Growth of Indian E-commerce

India's online retail sector is on track to reach USD 300 billion by 2030, propelled by a surge in grocery orders and a 41.5% sales contribution from Tier-2 and Tier-3 cities in 2022. Traditional block-stack warehouses can no longer support same-day or 10-minute expectations, prompting 4,000+ dark stores to install automated picking pods and robotic sorters. Logistics costs, which consumed 7.8-8.9% of GDP in 2024, are forecast to fall as automated hubs cut mis-picks and shrink delivery kilometers. Forward-looking operators are layering AI-based inventory engines over AS/RS grids to orchestrate multi-channel stock pools in real time.

Fast-track GST-Led Consolidation of Warehouses

GST removed state-border inventory buffers, allowing national distribution networks to flourish. Average facility size jumped from 50,000 sq ft in 2023 to over 200,000 sq ft by 2025, cementing the economic case for high-bay AS/RS and shuttle systems. Pallet counts per site often top 10,000, encouraging multilevel clad-rack designs that maximize vertical space while trimming civil costs. FMCG and pharmaceuticals benefit most because consolidated nodes simplify batch traceability and cold-chain compliance. Rental rates climbed 5% in Pune and NCR during 2024 as developers raced to deliver Grade-A boxes with flat floors and 11-12 m clear heights, prerequisites for fast-moving cranes.

Abundant Low-cost Manual Labor Pool

With 500 million workers in the informal sector, entry-level wages of Rs 15,000-20,000 per month extend the payback window for mechanization. In Tier-3 centers, costs are 30-40% lower, tempting SMEs to delay automation. Yet wage inflation topped 15-20% in Mumbai and Delhi during 2024 as warehouses competed for skilled handlers. Simultaneously, younger workers are pivoting to higher-skill jobs, eroding labor quality and fueling interest in semi-automated aids such as voice picking and goods-to-person carts.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Goods and Services Tax E-invoicing APIs

- Government PLI Schemes Boosting SKU Proliferation

- High Upfront CAPEX of AS/RS and Robotics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware commanded 60.55% of 2025 revenue, underscoring India warehouse automation market reliance on conveyors, shuttle racks, and robotic arms. Large brownfield campuses in Bhiwandi and Sriperumbudur tapped high-bay AS/RS to quadruple pallet density within existing footprints, reinforcing hardware's role as the operational backbone. Yet as installed bases mature, decision-makers are shifting budget toward cloud WMS, digital twins, and AI engines that unlock latent capacity and lift utilization above 85%.

Software's 27.40% CAGR through 2031 mirrors this pivot. SaaS platforms such as Addverb's Mobinity orchestrate multi-vendor fleets and inject machine learning into slotting, labor assignment, and energy management. Retro-fits dominate 2026-2028 spending cycles as operators realize that data-rich control layers deliver step-change returns on earlier hardware layouts. Services follow suit because integrators are needed to weave siloed machines into unified, API-compliant ecosystems.

Semi-automated solutions held 48.60% of India warehouse automation market share in 2025, reflecting a pragmatic appetite for incremental change. Put-to-light stations, carousel modules, and lift trucks fitted with real-time location sensors typically raise productivity 40-60% but cost 30-50% less than full robotics. Enterprises pair these tools with flexible financing, testing workflows before upgrading to goods-to-person bots.

Fully automated robotics, advancing at 27.10% CAGR, are surfacing in pharmaceutical and cold-chain facilities where compliance fines dwarf equipment costs. Vendors bundle environmental monitoring, traceability logs, and AI vision into turnkey cells that slash error rates to under 0.1%. Price parity is also improving as domestic component lines scale under the Component Manufacturing Scheme. By 2031, industry consensus expects a 60-40 split favoring fully automated formats in greenfield builds.

Complete Report Scope:

- By Component

- Hardware

- Software

- Services

- By Automation Level

- Basic Mechanization

- Semi-Automated Systems

- Fully Automated (Robotics/AS-RS)

- By Function

- Picking and Sorting

- Palletizing and Depalletizing

- Storage and Retrieval

- Packaging and Labelling

- Vision Inspection and QC

- Transportation and AGV/AMR

- By End-user Industry

- E-commerce and 3PL

- FMCG and Retail

- Pharmaceuticals and Healthcare

- Automotive

- Electronics

- Other End-user Industries

List of Companies Covered in this Report:

- Addverb Technologies Private Limited

- Alligator Automations Private Limited

- Alstrut India Private Limited

- Armstrong Machine Builders Private Limited

- Clearpack India Private Limited

- Delta Electronics, Inc.

- Falcon Autotech Private Limited

- Signode India Limited

- Titan Engineering and Automation Limited

- Win Automation (Wipro Limited)

- Worldpack Automation Systems Private Limited

- SICK AG

- Keyence Corporation

- OMRON Corporation

- GreyOrange Private Limited

- Godrej Consoveyo Logistics Automation Limited

- SSI SCHAEFER Systems International Private Limited

- Daifuku Co., Ltd.

- Swisslog Holding AG

- Honeywell Intelligrated (Honeywell International Inc.)

- Toyota Material Handling India Private Limited

- Vanderlande Industries B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth of Indian e-commerce

- 4.2.2 Fast-track GST-led consolidation of warehouses

- 4.2.3 Adoption of Goods and Services Tax e-invoicing APIs

- 4.2.4 Government PLI schemes boosting SKU proliferation

- 4.2.5 Demand for 10-minute "quick-commerce" fulfilment

- 4.2.6 Labor-shortage spikes in Tier-1 logistics hubs

- 4.3 Market Restraints

- 4.3.1 Abundant low-cost manual labor pool

- 4.3.2 High upfront capex of AS/RS and robotics

- 4.3.3 Fragmented SME-owned warehouse footprint

- 4.3.4 Inconsistent power-quality and floor-flatness norms

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Automation Level

- 5.2.1 Basic Mechanization

- 5.2.2 Semi-Automated Systems

- 5.2.3 Fully Automated (Robotics/AS-RS)

- 5.3 By Function

- 5.3.1 Picking and Sorting

- 5.3.2 Palletizing and Depalletizing

- 5.3.3 Storage and Retrieval

- 5.3.4 Packaging and Labelling

- 5.3.5 Vision Inspection and QC

- 5.3.6 Transportation and AGV/AMR

- 5.4 By End-user Industry

- 5.4.1 E-commerce and 3PL

- 5.4.2 FMCG and Retail

- 5.4.3 Pharmaceuticals and Healthcare

- 5.4.4 Automotive

- 5.4.5 Electronics

- 5.4.6 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Addverb Technologies Private Limited

- 6.4.2 Alligator Automations Private Limited

- 6.4.3 Alstrut India Private Limited

- 6.4.4 Armstrong Machine Builders Private Limited

- 6.4.5 Clearpack India Private Limited

- 6.4.6 Delta Electronics, Inc.

- 6.4.7 Falcon Autotech Private Limited

- 6.4.8 Signode India Limited

- 6.4.9 Titan Engineering and Automation Limited

- 6.4.10 Win Automation (Wipro Limited)

- 6.4.11 Worldpack Automation Systems Private Limited

- 6.4.12 SICK AG

- 6.4.13 Keyence Corporation

- 6.4.14 OMRON Corporation

- 6.4.15 GreyOrange Private Limited

- 6.4.16 Godrej Consoveyo Logistics Automation Limited

- 6.4.17 SSI SCHAEFER Systems International Private Limited

- 6.4.18 Daifuku Co., Ltd.

- 6.4.19 Swisslog Holding AG

- 6.4.20 Honeywell Intelligrated (Honeywell International Inc.)

- 6.4.21 Toyota Material Handling India Private Limited

- 6.4.22 Vanderlande Industries B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment