PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072526

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072526

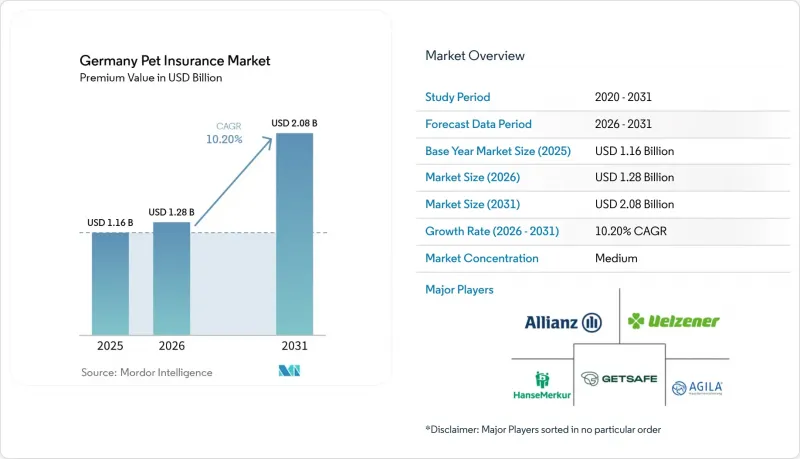

Germany Pet Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany pet insurance market size in terms of premium value is expected to grow from USD 1.16 billion in 2025 to USD 1.28 billion in 2026 and is forecast to reach USD 2.08 billion by 2031 at 10.20% CAGR over 2026-2031.

This report is Segmented by Policy Type (Pet Health and Pet Liability Insurance), Animal Type (Dogs and Cats), Sales Channel (Direct To Consumer, Broker/Agent, Bancassurance, and More), Coverage Level (Basic (<= €1, 000 Annual Cap), Standard (<= €5, 000 Annual Cap), and More), and Region (North, West, and More). The Market Forecasts are Provided in Value (USD).

Germany Pet Insurance Market Trends and Insights

Rising Pet Humanization & Willingness to Spend on Health

Nearly 73% of German owners identify pet parenting as central to their lifestyle, and spending priorities now emphasize welfare over cost. The result is a sustained preference for broad medical cover, preventive services, and even alternative therapies that mirror human care models. Emotional attachment reduces price sensitivity, encouraging insurers to launch premium tiers with unlimited caps, dental benefits, and travel extensions. In response, carriers have started loyalty programs that refund unused wellness budgets, reinforcing a perception of tangible value. Expanded public discussion around animal rights further normalizes the idea that quality veterinary care is a moral obligation, solidifying long-run demand in the Germany pet insurance market.

Increasing Pet Adoption Post-COVID

Remote work extended daily time spent at home, prompting many urban professionals to acquire pets for companionship. Household pet ownership reached 45% in 2024, totalling 34.3 million animals. New owners, unfamiliar with veterinary bills, view insurance as a straightforward budgeting instrument and respond well to educational content on accident-cost scenarios. Insurers now lead onboarding campaigns at breeder sites, shelters, and e-commerce checkout pages, converting first-time owners at the decision point. As flexible work patterns persist, continued inflow of puppies and kittens supports a longer-term policy pipeline, while social-media storytelling from satisfied claimants amplifies peer-to-peer influence.

High Premium Cost vs Perceived Need

Monthly charges ranging from USD 14.5 to USD 94.7 remain a hurdle for price-sensitive households, especially those that have never faced large veterinary bills. East German consumers retain cautious spending habits, slowing uptake despite improving purchasing power. Entry-level plans, installment billing, and clearer claim-probability calculators are helping narrow the perception gap, but many owners still weigh premiums against routine vaccination costs instead of worst-case scenarios. Rising inflation in household energy and food costs competes for disposable income, compounding reluctance. Insurers experimenting with micro-deductibles and mileage-style caps aim to offer just enough protection at a lower monthly price point.

Other drivers and restraints analyzed in the detailed report include:

- Rising Veterinary Costs Due to Advanced Treatments

- Expansion of Flexible, Customisable Policy Products

- Limited Cover for Senior Pets & Pre-Existing Conditions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pet health insurance generated 80.74% of 2025 premiums, underscoring how direct exposure to medical bills outweighs liability concerns for most owners. The Germany pet insurance market size for liability coverage is smaller but expands at 11.55% CAGR as more states mandate third-party protection for dogs. Liability premiums, starting at USD 3.49 monthly, serve as an entry product that familiarises price-sensitive owners with insurance. Cross-sell strategies convert liability clients into combined medical packages, elevating average revenue per policy and improving retention. Carriers are also exploring bundled discounts that attach liability cover automatically to mid and top-tier health plans, reducing friction for owners and simplifying compliance updates as regulations evolve.

Legislation mandating coverage is consistently driving up volumes, positioning liability as the primary growth engine for the industry. This trend highlights the increasing importance of liability insurance as a structural driver for sustained market expansion. Health insurance, bolstered by cutting-edge claims processing and an array of enticing add-ons, continues to serve as the industry's cornerstone. These advancements enhance customer satisfaction and streamline operational efficiency for insurers. Owners, already equipped with liability plans, are increasingly drawn to high-deductible health plans. This choice safeguards their budget and mitigates risks associated with major surgeries, offering a balanced approach to cost management and coverage. With dog ownership plateauing and cat adoption on the upswing, insurers foresee a further shift in the liability ratio. This anticipation is fueled by ongoing political discussions aiming to extend mandatory third-party coverage beyond just canines, potentially broadening the market and creating new growth opportunities for insurers.

Dogs contributed 63.92% of written premiums in 2025 because higher average treatment costs and liability obligations compel owners to seek protection. The Germany pet insurance market size for cats escalates faster at 13.19% CAGR as urbanization and smaller households favor feline companions. Cat policies generally price 20-30% below dog equivalents, broadening affordability without eroding margins thanks to lower average claim costs. Younger owners are also more willing to buy multi-pet packages, combining cat and dog cover under one discount, improving overall spending per household. Marketing content now includes breed-specific health tips that double as risk-mitigation tools, lowering claim frequency while increasing perceived insurer expertise.

Breed-linked orthopedic risks keep dog premiums elevated, while indoor lifestyle-related illnesses such as obesity and renal disease drive the cat claims mix. Insurers tailor underwriting formulas to each species, refining risk selection and sustaining profitability. Gene-testing add-ons, offered at a reduced price for policyholders, identify hereditary disorders early and build data insights. Growth in cat coverage also helps close the penetration gap among metropolitan renters, expanding overall policy counts in the Germany pet insurance market.

Complete Report Scope:

- By Policy Type

- Pet Health Insurance

- Pet Liability Insurance

- By Animal Type

- Dogs

- Cats

- By Sales Channel

- Direct to Consumer

- Broker / Agent

- Bancassurance

- Online Aggregators & Insurtech Platforms

- By Coverage Level

- Basic (<= €1 000 annual cap)

- Standard (<= €5 000 annual cap)

- Comprehensive (Unlimited / higher caps)

- By Region

- North

- West

- South

- East

List of Companies Covered in this Report:

- Allianz Versicherungs-AG

- AGILA Haustierversicherung AG

- Uelzener Allgemeine Versicherungs-Gesellschaft

- HanseMerkur Krankenversicherung AG

- Getsafe Digital GmbH

- DFV Deutsche Familienversicherung AG

- Figo Pet Insurance (Germany)

- Petplan Germany (Allianz Group)

- Zurich Gruppe Deutschland

- AXA Versicherung AG

- Barmenia Versicherungen

- Helvetia Versicherungen Deutschland

- Wurttembergische Versicherung AG

- R+V Versicherung AG

- Generali Deutschland Versicherung AG

- ERGO Versicherung AG

- Gothaer Versicherungsbank VVaG

- Luko Cover Clinic / Coya AG

- Feather Insurance GmbH

- HDI Versicherung AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising pet humanisation & willingness to spend on health

- 4.2.2 Increasing pet adoption post-COVID

- 4.2.3 Rising veterinary costs due to advanced treatments

- 4.2.4 Expansion of flexible, customisable policy products

- 4.2.5 Integration of IoT pet-wearables enabling risk-based pricing

- 4.2.6 State-level debate on mandatory pet health cover

- 4.3 Market Restraints

- 4.3.1 High premium cost vs perceived need

- 4.3.2 Limited cover for senior pets & pre-existing conditions

- 4.3.3 Fragmented data standards hamper benchmarking

- 4.3.4 Growth of vet "direct-payment" wellness plans

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers (Veterinary Clinics)

- 4.7.3 Bargaining Power of Buyers (Pet Owners)

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Policy Type

- 5.1.1 Pet Health Insurance

- 5.1.2 Pet Liability Insurance

- 5.2 By Animal Type

- 5.2.1 Dogs

- 5.2.2 Cats

- 5.3 By Sales Channel

- 5.3.1 Direct to Consumer

- 5.3.2 Broker / Agent

- 5.3.3 Bancassurance

- 5.3.4 Online Aggregators & Insurtech Platforms

- 5.4 By Coverage Level

- 5.4.1 Basic (<= €1 000 annual cap)

- 5.4.2 Standard (<= €5 000 annual cap)

- 5.4.3 Comprehensive (Unlimited / higher caps)

- 5.5 By Region

- 5.5.1 North

- 5.5.2 West

- 5.5.3 South

- 5.5.4 East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Allianz Versicherungs-AG

- 6.4.2 AGILA Haustierversicherung AG

- 6.4.3 Uelzener Allgemeine Versicherungs-Gesellschaft

- 6.4.4 HanseMerkur Krankenversicherung AG

- 6.4.5 Getsafe Digital GmbH

- 6.4.6 DFV Deutsche Familienversicherung AG

- 6.4.7 Figo Pet Insurance (Germany)

- 6.4.8 Petplan Germany (Allianz Group)

- 6.4.9 Zurich Gruppe Deutschland

- 6.4.10 AXA Versicherung AG

- 6.4.11 Barmenia Versicherungen

- 6.4.12 Helvetia Versicherungen Deutschland

- 6.4.13 Wurttembergische Versicherung AG

- 6.4.14 R+V Versicherung AG

- 6.4.15 Generali Deutschland Versicherung AG

- 6.4.16 ERGO Versicherung AG

- 6.4.17 Gothaer Versicherungsbank VVaG

- 6.4.18 Luko Cover Clinic / Coya AG

- 6.4.19 Feather Insurance GmbH

- 6.4.20 HDI Versicherung AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment