PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072534

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072534

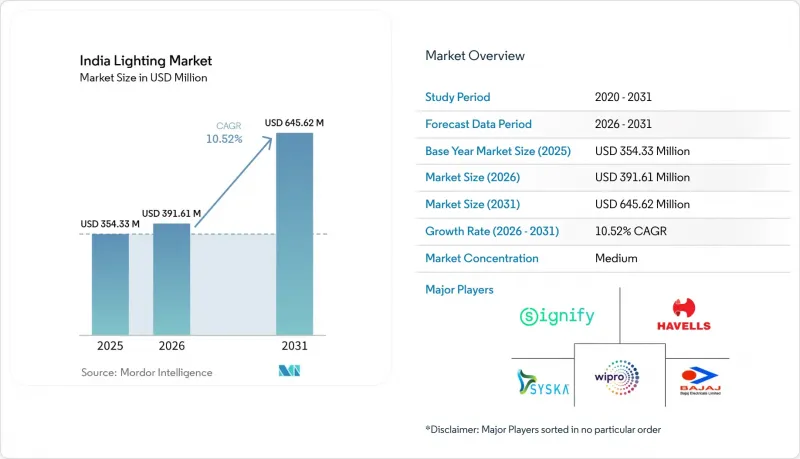

India Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india lighting market size is expected to grow from USD 354.33 million in 2025 to USD 391.61 million in 2026 and is forecast to reach USD 645.62 million by 2031 at 10.52% CAGR over 2026-2031.

This report is Segmented by Product Type (Luminaires / Fixtures, and Lamps), Light Source (LED, and Conventional), Distribution Channel (Direct Sales / Developers / Contract, Wholesalers / Electricians, Lighting Specialists, and Others), Application (Commercial, Industrial, Outdoor, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

India Lighting Market Trends and Insights

LED price erosion and energy-efficiency mandates

Mandatory ECBC compliance for new commercial buildings plus BEE star-label requirements have pushed developers toward high-efficacy fixtures that deliver 35%-50% energy savings relative to baseline codes. UJALA's competitive tenders cut retail LED bulb prices by 90% from 2014 figures and distributed 36.87 crore units, making LEDs the universal default even beyond public-sector programs. As electricity tariffs climb and corporate net-zero pledges gain momentum, enterprises now treat lighting retrofits as first-wave decarbonization measures. The result is sustained double-digit volume demand for premium-efficiency chips, optics, and drivers across commercial, industrial, and high-end residential builds. Vendors that certify products under the latest Super ECBC thresholds are defending margins despite broader price competition.

Rapid urban infrastructure build-out (Smart Cities Mission)

The Smart Cities Mission has approved USD 24.7 billion in projects and completed 5,909 work orders by July 2024; each integrated command center specifies connected street, area, and facade lighting that can be monitored in real time. Municipalities increasingly bundle lighting into traffic, safety, and environmental dashboards, turning luminaires into edge nodes for broader city-data platforms. Vendors able to supply interoperable controls, adaptive-dimming algorithms, and cyber-secure firmware are winning multiyear framework contracts. Because second-tier cities replicate flagship designs from metros such as Pune and Varanasi, contract pipelines extend well into the medium term. The clustering of projects also shortens payback cycles for specialized installers and keeps warehouse throughput high for component suppliers.

High upfront retrofit cost for SMEs and households

Small factories and neighborhood retailers often face payback periods of 3-5 years on full-facility LED conversions, making many defer projects despite 40%-60% potential energy savings. Limited awareness of lifecycle economics keeps decision-makers focused on sticker price rather than total cost of ownership. Although micro-finance and utility-on-bill schemes exist, uptake remains low in non-metro clusters because of cumbersome documentation and perceived technology risk. This capex hurdle slows penetration of connected fixtures and sensors that carry higher dollar-per-lumen pricing compared with basic retrofit bulbs.

Other drivers and restraints analyzed in the detailed report include:

- Government procurement (UJALA and SLNP)

- Growth of Tier-II/III city facade-lighting projects

- Fragmented distribution and counterfeit products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The luminaires and fixtures segment commanded a 58.72% revenue slice of the India lighting market in 2025 and is projected to grow at a 11.78% CAGR through 2031, underlining its dual role as both volume and value driver of the India lighting market. This category's rise stems from Smart Cities Mission tenders that specify integrated, sensor-ready fixtures and from private developers bundling lighting with building-automation contracts to cut commissioning time. Luminaires frequently anchor facade-lighting packages, earning higher margins than commodity lamps because they embed optics, drivers, and on-board diagnostics that meet Bureau of Energy Efficiency specifications. Contractors targeting metro rail, airport-terminal, and data-center projects also prefer turnkey luminaires to minimize field wiring errors and accelerate sign-off, extending the segment's edge in the India lighting market.

Second-order momentum comes from programmable RGB architectural jobs in Tier-II/III cities, where local authorities seek tourism branding without paying metro-grade premiums. Mid-range manufacturers that certify to BIS safety rules are winning here by pairing aluminum extrusion heat sinks with DMX controls that survive high-humidity coastal climates. Lamps, by contrast, continue to cede ground as price erosion compresses margins and government procurement resets bulk tender benchmarks. Even so, retrofit CFL-to-LED bulb swaps persist in the residential channel, cushioning lamps' volume decline but not reversing the structural tilt toward higher-value luminaires.

India LED lighting solutions held an 81.35% India lighting market share in 2025 and are projected to post the fastest 12.05% CAGR to 2031. The India lighting market size is tied to LEDs for commercial ceilings, roadway poles, and industrial high-bays, reflecting deeper penetration into price-sensitive rural installations. UJALA and Street Lighting National Program tenders normalized LED economics, while ECBC "Super" ratings funnel premium demand toward >=150-lm/W luminaires that still command price premiums. Conventional fluorescent and HID technologies now survive mainly in legacy high-temperature factories where drivers face derating risks, but even those niches are shrinking as ruggedized LED engine platforms pass accelerated lifecycle tests.

LED adoption also benefits from emerging Li-Fi pilots that turn luminaires into data nodes, allowing facilities to overlay broadband capacity without radio-frequency congestion. Wipro Lighting's alliance with pureLiFi exemplifies how vendors link illumination with connectivity to protect margins in a rapidly commoditizing diode market. At the same time, the Production-Linked Incentive Scheme for white goods subsidizes chip-on-board back-end lines, further localizing the LED bill of materials and improving cost resilience against import shocks, an upside for the India lighting industry as a whole.

Complete Report Scope:

- By Product Type

- Luminaires / Fixtures

- Lamps

- By Light Source

- LED

- Conventional

- By Distribution Channel

- Direct Sales / Developers / Contract

- Wholesalers / Electricians

- Lighting Specialists

- Others

- By Application

- Commercial

- Offices

- Retail and Hospitality

- Healthcare Facilities

- Others

- Industrial

- Process Industries

- Discrete Industries

- Warehouses and Other Industrial Set-ups

- Outdoor

- Residential

- Commercial

List of Companies Covered in this Report:

- Signify N.V.

- Havells India Limited

- Wipro Lighting (Wipro Ltd.)

- Bajaj Electricals Ltd.

- Syska LED Lights Pvt Ltd.

- Crompton Greaves Consumer Electricals Ltd.

- Surya Roshini Ltd.

- Halonix Technologies Pvt Ltd.

- MIC Electronics Ltd.

- Orient Electric Ltd.

- Panasonic Life Solutions India Pvt Ltd.

- Osram GmbH

- Zumtobel Group AG

- Acuity Brands Inc.

- Eaton Corporation plc (Cooper Lighting)

- Hubbell Inc.

- Fagerhult AB

- Dialight plc

- Nichia Corporation

- Eveready Industries India Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LED price erosion and energy-efficiency mandates

- 4.2.2 Rapid urban infrastructure build-out (Smart Cities Mission)

- 4.2.3 Government procurement (UJALA and SLNP)

- 4.2.4 Growth of Tier-II/III city facade-lighting projects

- 4.2.5 Emerging DC-micro-grid and off-grid solar lighting demand

- 4.2.6 Integration of Li-Fi pilots in enterprise campuses

- 4.3 Market Restraints

- 4.3.1 High upfront retrofit cost for SMEs and households

- 4.3.2 Fragmented distribution and counterfeit products

- 4.3.3 Import-linked volatility in LED driver IC pricing

- 4.3.4 Slow pay-out cycles in government EPC contracts

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Luminaires / Fixtures

- 5.1.2 Lamps

- 5.2 By Light Source

- 5.2.1 LED

- 5.2.2 Conventional

- 5.3 By Distribution Channel

- 5.3.1 Direct Sales / Developers / Contract

- 5.3.2 Wholesalers / Electricians

- 5.3.3 Lighting Specialists

- 5.3.4 Others

- 5.4 By Application

- 5.4.1 Commercial

- 5.4.1.1 Offices

- 5.4.1.2 Retail and Hospitality

- 5.4.1.3 Healthcare Facilities

- 5.4.1.4 Others

- 5.4.2 Industrial

- 5.4.2.1 Process Industries

- 5.4.2.2 Discrete Industries

- 5.4.2.3 Warehouses and Other Industrial Set-ups

- 5.4.3 Outdoor

- 5.4.4 Residential

- 5.4.1 Commercial

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Havells India Limited

- 6.4.3 Wipro Lighting (Wipro Ltd.)

- 6.4.4 Bajaj Electricals Ltd.

- 6.4.5 Syska LED Lights Pvt Ltd.

- 6.4.6 Crompton Greaves Consumer Electricals Ltd.

- 6.4.7 Surya Roshini Ltd.

- 6.4.8 Halonix Technologies Pvt Ltd.

- 6.4.9 MIC Electronics Ltd.

- 6.4.10 Orient Electric Ltd.

- 6.4.11 Panasonic Life Solutions India Pvt Ltd.

- 6.4.12 Osram GmbH

- 6.4.13 Zumtobel Group AG

- 6.4.14 Acuity Brands Inc.

- 6.4.15 Eaton Corporation plc (Cooper Lighting)

- 6.4.16 Hubbell Inc.

- 6.4.17 Fagerhult AB

- 6.4.18 Dialight plc

- 6.4.19 Nichia Corporation

- 6.4.20 Eveready Industries India Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment