PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072575

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072575

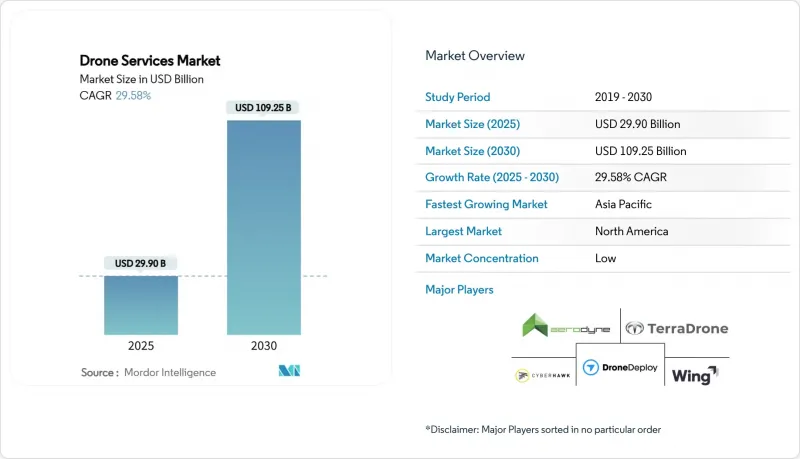

Drone Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

According to Mordor Intelligence, the drone services market size reached USD 29.9 billion in 2025 and is projected to climb to USD 109.246 billion by 2030, reflecting a 29.58% CAGR over the forecast horizon.

This report is Segmented by Service Type (Piloting and Operations, and Data Analytics), End User Industry (Construction and Infrastructure, and More), Drone Type (Rotary-Wing, Fixed-Wing, and Hybrid VTOL), Operating Range (Visual Line-Of-Sight and Beyond Visual Line-Of-Sight), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Drone Services Market Trends and Insights

Growing Demand for High-Frequency Asset Inspection in Energy and Utilities

Power-line, pipeline, and renewable-asset operators re-engineered maintenance around automated aerial scans. Dominion Energy's multi-role program inspects solar farms, storm-hit grids, and nuclear power plants around the clock. At the same time, Georgia Power's fleet flagged 5,174 anomalies across 7,000 structures, triple the count achieved by ground crews, and carved 60% from annual O&M budgets. Methane-sniffing payloads extend coverage to leak-prone pipelines, meeting tightening environmental rules and protecting shareholder value. The outcome is a shift from reactive fixes to predictive lifecycle management, which lengthens asset service life and reduces outage penalties.

Rapidly Declining Cost per Flight Hour for BVLOS Operations

Transport Canada removed special-flight certificates for Level 1 complex BVLOS sorties in November 2025, collapsing lead times and compliance spending. The FAA's forthcoming Part 108 framework mirrors that flexibility. At the same time, Iridium's L-band link underpinned the first waiver for remote pipeline patrols in the United States, cementing reliable command-and-control pathways. Combined with 24/7 drone-in-a-box launchers, end-to-end mission costs land well below crewed helicopter benchmarks, opening previously marginal business cases across sparsely populated corridors and offshore rigs.

Fragmented Regulatory Standards Across Countries

Operators juggling FAA, EASA, and emerging-market rule books must secure multiple pilot certifications, hardware labels, and insurance endorsements, inhibiting cross-border scale. Canada's 2025 overhaul diverges from EU class-marking schemes, forcing fleets to carry redundant documentation and inflating compliance overhead. The asynchronous rollout delays enterprise RFPs for continental delivery corridors and keeps smaller fleets domestic.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI-Powered Analytics Unlocking End-to-End Solutions

- Regulatory Fast-Tracking of Urban Air Mobility Corridor

- Limited Battery Endurance for Heavy-Lift Drones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Piloting and operations captured 52.35% of the drone services market share in 2024, underscoring the labor-intensive oversight still required under most aviation rules. Data Analytics is projected to advance at a 31.34% CAGR through 2030, the quickest pace among all service categories, signaling a shift toward monetizing insight rather than flight hours. The accelerating uptake of autonomous docking stations from suppliers such as Percepto and Skydio is expected to reduce pilot demand and compress the cost base of traditional operations. Programs like Elk Grove, California's Drone as First Responder 2.0 already allow one operator to supervise several autonomous aircraft simultaneously, demonstrating how centralized Real-Time Information Centers can scale coverage without proportional labor growth. As regulations evolve toward corporate-oversight models, the drone services market size for piloting and operations is expected to grow more slowly than analytics-centric offerings, even as it remains vital for safety management.

Edge computing and 5G links now enable drones to process LiDAR, thermal, and multispectral feeds during flight, converting raw pixels into actionable work orders before landing. Airborne Ultralight Spectrometer technology exemplifies this evolution by detecting methane and CO2 in real-time, enabling firms such as TotalEnergies to align with ambitious emissions goals. Computer-vision models routinely deliver 78% higher fault-detection accuracy than manual reviews while trimming electrical downtime by 35%. These gains reduce data-handling costs and speed decision cycles, strengthening the competitive position of providers offering end-to-end analytics platforms. Enterprises consequently view insight delivery as the core value driver, relegating flight execution to an enabling function rather than the primary revenue source.

Energy and utilities delivered 32.18% of 2024 turnover, underlining the segment's central role in grid-modernisation and methane-leak compliance mandates. The drone services market share for this vertical benefits from steady inspection cycles that convert CAPEX into predictable OPEX budgets. Drones equipped with optical zoom and thermal sensors review conductors, insulators, and right-of-way vegetation, trimming helicopter charter fees, and reducing crew hazard exposure.

Infrastructure and construction commands the fastest growth at 30.14% CAGR. BIM-friendly photogrammetry and LiDAR models compared against as-planned drawings identify millimetre discrepancies early, preventing costly rework. Megaprojects in APAC and the Middle East now embed weekly aerial scans as contractual deliverables, embedding drones into digital-twin workflows that cut schedule drift.

Complete Report Scope:

- By Service Type

- Piloting and Operations

- Data Analytics

- By End User Industry

- Construction and Infrastructure

- Agriculture and Forestry

- Energy and Utilities

- Law Enforcement and Public Safety

- Medical and Parcel Delivery

- Others (Mining, Real-estate, Media)

- By Drone Type

- Rotary-wing

- Fixed-wing

- Hybrid VTOL

- By Operating Range

- Visual Line-of-Sight (VLOS)

- Beyond Visual Line-of-Sight (BVLOS)

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America retained 41.97% of 2024 revenue thanks to coherent federal guidance, insurance acceptance, and a deep base of enterprise early adopters. The FAA logged 300 Drone-as-First-Responder (DFR) program submissions by mid-2025, illustrating municipal appetite for autonomous incident assessment. Utilities such as Georgia Power and Dominion Energy provide textbook ROI cases, while Oklahoma forecasts a USD 5.6 billion boost from advanced-air-mobility corridors.

The Asia-Pacific region is projected to grow at a 30.25% CAGR through 2030. Manufacturing scale keeps hardware prices low, and governments in China, Japan, South Korea, and India fund pilot corridors covering logistics, healthcare, and agriculture. Land-survey bookings and precision-spray packages anchor sizable order books, with survey operators expecting the regional drone services market size to exceed USD 2.5 billion by 2033.

Europe combines EASA's harmonized rules with a strong sustainability mandate. More than 1.6 million operators are registered under the common framework, and 83% of surveyed citizens view air taxis positively. Carbon-pricing mechanisms and dense urban topography give drones a clear advantage for short-haul deliveries. Pioneering offshore projects in the North Sea and Baltic expand the use cases for heavy-lift beyond inspection to include spare-parts logistics.

- Aerodyne Group Limited

- Terra Drone Corporation

- Cyberhawk Innovations Limited

- DroneDeploy, Inc.

- Sky-Futures (ICR Integrity)

- Zipline International Inc.

- Wing Aviation LLC

- DroneUp, LLC

- DroneBase, Inc.

- Flyability SA

- Percepto Robotics Ltd.

- AgEagle Aerial Systems Inc.

- Skycatch, Inc.

- Draganfly Innovations Inc.

- Ondas Holdings Inc.

- Amazon Prime Air (Amazon.com, Inc.)

- Skyports Drone Services

- Volatus Aerospace Corp.

- Flytrex Inc.

- Skydio, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for high-frequency asset inspection in energy and utilities

- 4.2.2 Rapidly declining cost per flight hour for BVLOS operations

- 4.2.3 Integration of AI-powered analytics unlocking end-to-end solutions

- 4.2.4 Regulatory fast-tracking of urban air mobility corridors

- 4.2.5 Satellite-to-drone communication enabling offshore coverage

- 4.2.6 Carbon-offset programs favouring drone logistics over ground miles

- 4.3 Market Restraints

- 4.3.1 Fragmented regulatory standards across countries

- 4.3.2 Limited battery endurance for heavy-lift drones

- 4.3.3 Public privacy and data-protection concerns

- 4.3.4 Persistent GPS jamming in conflict zones

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competetive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Piloting and Operations

- 5.1.2 Data Analytics

- 5.2 By End User Industry

- 5.2.1 Construction and Infrastructure

- 5.2.2 Agriculture and Forestry

- 5.2.3 Energy and Utilities

- 5.2.4 Law Enforcement and Public Safety

- 5.2.5 Medical and Parcel Delivery

- 5.2.6 Others (Mining, Real-estate, Media)

- 5.3 By Drone Type

- 5.3.1 Rotary-wing

- 5.3.2 Fixed-wing

- 5.3.3 Hybrid VTOL

- 5.4 By Operating Range

- 5.4.1 Visual Line-of-Sight (VLOS)

- 5.4.2 Beyond Visual Line-of-Sight (BVLOS)

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aerodyne Group Limited

- 6.4.2 Terra Drone Corporation

- 6.4.3 Cyberhawk Innovations Limited

- 6.4.4 DroneDeploy, Inc.

- 6.4.5 Sky-Futures (ICR Integrity)

- 6.4.6 Zipline International Inc.

- 6.4.7 Wing Aviation LLC

- 6.4.8 DroneUp, LLC

- 6.4.9 DroneBase, Inc.

- 6.4.10 Flyability SA

- 6.4.11 Percepto Robotics Ltd.

- 6.4.12 AgEagle Aerial Systems Inc.

- 6.4.13 Skycatch, Inc.

- 6.4.14 Draganfly Innovations Inc.

- 6.4.15 Ondas Holdings Inc.

- 6.4.16 Amazon Prime Air (Amazon.com, Inc.)

- 6.4.17 Skyports Drone Services

- 6.4.18 Volatus Aerospace Corp.

- 6.4.19 Flytrex Inc.

- 6.4.20 Skydio, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment