PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072576

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072576

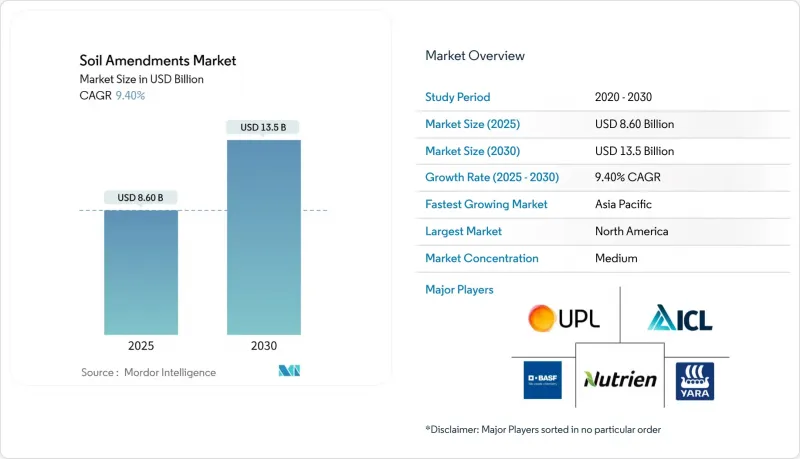

Soil Amendments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

According to Mordor Intelligence, the soil amendments market size is valued at USD 8.6 billion in 2025 and is forecast to reach USD 13.5 billion in 2030, advancing at a 9.4% CAGR.

This report is Segmented by Product Type (Organic Amendments, Inorganic Amendments, and More), by Form (Solid and Liquid), by Application (Agriculture, Horticulture and Turf, and More), by Crop Type (Cereals and Grains, Fruits and Vegetables, and More), by Soil Type (Sand, Clay, and More) and by Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Soil Amendments Market Trends and Insights

Accelerated transition to regenerative agriculture mandates

Government programs are reshaping purchasing behavior by tying subsidies to verifiable soil-health improvements. The USDA allocates USD 300 million to greenhouse-gas measurement and verification in 2023, while the EU funds 100 living labs that demonstrate best practices. Australia's National Soil Strategy adds AUD 21.599 million (USD 14.5 million) for monitoring networks that favor conditioners with proven carbon-sequestration benefits. Banks now require soil-health documentation for farm credit, rewarding early adopters with better loan terms. These actions compound to lift the soil amendments market by expanding the addressable user base and shortening payback periods for new products.

Rising carbon credit valuation incentivizing biochar

Voluntary carbon markets price removal credits at EUR 174 (USD 190) per metric ton, and verified biochar trades between EUR 300 and EUR 2,000 (USD 327-2,180) per metric ton in Europe. Soil amendment producers embrace dual-revenue models, selling biochar to farmers and monetizing certified removals. Pilot facilities in Washington State, backed by USD 20.49 million in USDA grants, illustrate the scale-up path. Corporate buyers, such as beverage and technology firms, pre-purchase credits to meet net-zero targets, anchoring demand and improving project bankability.

Patchy, ambiguous global regulations for amendments

Fragmented rules on product registration delay launches and inflate compliance costs. The European Union's shift from Regulation 2003/2003 to 2019/1009 forced re-certification of many conditioners. Canada's modernized fertilizer code extends renewal cycles yet introduces new data requirements. Companies must keep multiple formulations for different jurisdictions, limiting economies of scale and slowing global rollouts.

Other drivers and restraints analyzed in the detailed report include:

- Government bans on high-salinity synthetic fertilizers

- Soil microbiome seed coating synergies boosting demand

- Farmer Skepticism from Inconsistent Field Results

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Organic amendments held 57% share of the soil amendments market size in 2024, with compost, manure, and humic substances leading the category. Biochar-based products are projected to grow at a 12.4% CAGR, driven by carbon-credit opportunities and yield improvements. While inorganic products maintain their position in specialty crops, biological formulations show rapid growth through seed-coating applications. India's Minister Nitin Gadkari endorsed biochar workshops and subsidized pyrolyser technologies in May 2025, while Denmark implemented a pyrolysis-biochar strategy in October 2024, allocating EUR 13.5 million (USD 14.6 million) for R&D and EUR 1.34 billion (USD 14.5 million) in subsidies through 2027.

Organic amendments dominate the global soil amendments market due to their established usage, regulatory acceptance, and organic agriculture demand. The Department for Environment, Food and Rural Affairs reports that in 2023, Cattle FYM was the primary organic fertilizer in Great Britain, used by 47.1% of farmers, while Cattle Slurry ranked second at 16.7% adoption, offering essential nutrients while reducing chemical fertilizer requirements.

Granules and powders account for 68% of the soil amendments market share due to storage stability and bulk-fertilizer logistics compatibility. Liquid formulations are projected at 11.2% CAGR through 2030, driven by fertigation and drone-based foliar applications. Dry solids maintained the largest market share in 2023-2024, particularly in cereal and grain cultivation, due to sustained nutrient release, soil structure improvement, and water retention properties.

Biodegradable polymer encapsulation enables controlled-release solid granules that combine liquid-like precision with practical handling. Water-soluble packaging reduces operator exposure while meeting safety and sustainability requirements. Brazil's 2024 "Precision Ag Initiative" funds liquid humic-microbe applications in soybean and orange cultivation, while the European Biostimulant Industry Council introduced guidelines in early 2025 for liquid microbial inoculants in EU fertigation systems.

Complete Report Scope:

- By Product Type

- Organic Amendments

- Inorganic Amendments

- Biological/Microbial Amendments

- By Form

- Solid

- Liquid

- By Application

- Agriculture

- Horticulture and Turf

- Environmental Remediation

- By Crop Type

- Cereals and Grains

- Fruits and Vegetables

- Oilseeds and Pulses

- By Soil Type

- Sand

- Clay

- Loam and Silt

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- North America

Geography Analysis

North America holds 31% of 2024 revenue, underpinned by USD 120 million in federal biochar grants, robust carbon markets, and advanced precision-farming adoption. Canada's revamped fertilizer rules and extensive extension services foster trust in biologicals. Strong farm incomes allow growers to trial premium conditioners without compromising cash flow, and the region's research institutions shorten product-validation cycles.

Asia-Pacific records the fastest soil amendments market growth, at 12.7% CAGR to 2030. China enforces strict arable-land safeguards across 124.33 million hectares, integrating conditioners into rehabilitation mandates. India's Dhan-Dhaanya Krishi Yojana directs subsidies toward 100 low-productivity districts, catalyzing conditioner adoption among smallholders. The region benefits from large biomass streams for organic feedstocks, though distribution and agronomic-training gaps persist.

Europe shows steady expansion, driven by the EU Soil Deal's 100 living labs and a forthcoming Soil Monitoring Law addressing degraded land that costs EUR 50 billion (USD 54.5 billion) annually. Biochar fetches EUR 300-2,000 (USD 327-2,180) per metric ton, depending on certification status, rewarding innovators that deliver verified removals. Tight fertilizer-salinity limits and a 2050 carbon-neutral target embed conditioners into compliance pathways.

- Yara International ASA

- BASF SE

- Nutrien Ltd

- ICL Group

- UPL Ltd

- Syngenta AG

- Corteva Agriscience

- Scotts Miracle-Gro Company

- Novozymes A/S

- Humintech GmbH

- Biochar Supreme, LLC

- Lallemand Inc

- Omnia Nutriology

- Calix Ltd

- BioSafe Systems

- Bioceres S.A.

- Mosaic Company

- AgroLiquid

- FMC Corporation

- Genesis Industries Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated transition to regenerative agriculture mandates

- 4.2.2 Rising carbon credit valuation incentivizing biochar

- 4.2.3 Soil microbiome seed coating synergies boosting demand

- 4.2.4 Water scarcity driving uptake of super-absorbent polymers

- 4.2.5 Government bans on high-salinity synthetic fertilizers

- 4.2.6 Net-zero supply-chain commitments

- 4.3 Market Restraints

- 4.3.1 Patchy, ambiguous global regulations for amendments

- 4.3.2 Organic raw-material price volatility

- 4.3.3 Farmer skepticism from inconsistent field results

- 4.3.4 Weak distribution for live microbial products

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of Substitutes

- 4.6.4 Threat of New Entrants

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Organic Amendments

- 5.1.2 Inorganic Amendments

- 5.1.3 Biological/Microbial Amendments

- 5.2 By Form

- 5.2.1 Solid

- 5.2.2 Liquid

- 5.3 By Application

- 5.3.1 Agriculture

- 5.3.2 Horticulture and Turf

- 5.3.3 Environmental Remediation

- 5.4 By Crop Type

- 5.4.1 Cereals and Grains

- 5.4.2 Fruits and Vegetables

- 5.4.3 Oilseeds and Pulses

- 5.5 By Soil Type

- 5.5.1 Sand

- 5.5.2 Clay

- 5.5.3 Loam and Silt

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 Turkey

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Kenya

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 BASF SE

- 6.4.3 Nutrien Ltd

- 6.4.4 ICL Group

- 6.4.5 UPL Ltd

- 6.4.6 Syngenta AG

- 6.4.7 Corteva Agriscience

- 6.4.8 Scotts Miracle-Gro Company

- 6.4.9 Novozymes A/S

- 6.4.10 Humintech GmbH

- 6.4.11 Biochar Supreme, LLC

- 6.4.12 Lallemand Inc

- 6.4.13 Omnia Nutriology

- 6.4.14 Calix Ltd

- 6.4.15 BioSafe Systems

- 6.4.16 Bioceres S.A.

- 6.4.17 Mosaic Company

- 6.4.18 AgroLiquid

- 6.4.19 FMC Corporation

- 6.4.20 Genesis Industries Limited

7 Market Opportunities and Future Outlook